|

市場調查報告書

商品編碼

1871295

實驗室自建檢測市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Laboratory Developed Tests Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

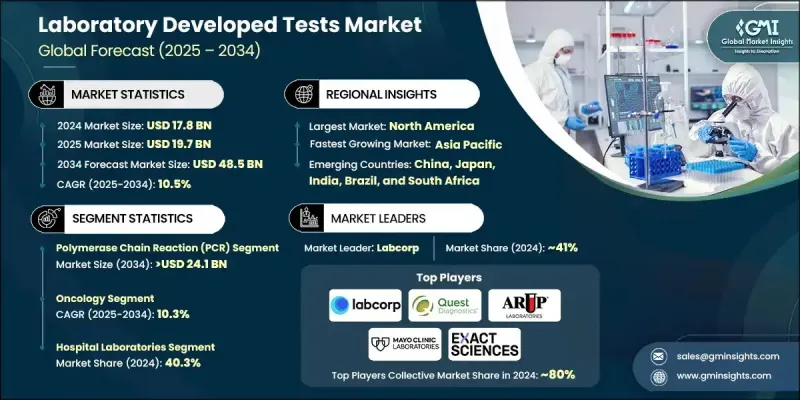

2024 年全球實驗室自建測試市場價值為 178 億美元,預計到 2034 年將以 10.5% 的複合年成長率成長至 485 億美元。

實驗室自建檢測(LDT)的快速成長主要得益於人們對疾病早期檢測意識的提高、傳染病和慢性病患病率的上升,以及癌症和遺傳性疾病病例的不斷增加。 LDT是指在同一實驗室內完成創建、生產和使用的診斷測試,它徹底改變了個人化醫療,改善了疾病管理並輔助臨床決策。 LDT能夠快速創新並根據特定患者的需求量身定做測試,這正在改變醫療保健行業,尤其是在需要精準個體化診斷的複雜疾病領域。各公司提供種類繁多的測試,從先進的下一代定序(NGS)檢測到複雜的分子診斷和生物標記檢測。這些測試利用了最先進的技術,包括高通量基因組學、人工智慧驅動的演算法、生物資訊學平台和雲端資料整合。隨著癌症發生率的持續攀升,對早期、準確和個人化診斷的需求也日益成長。 LDT發揮著至關重要的作用,能夠快速檢測基因突變、生物標記和疾病亞型,這對於制定標靶治療方案和改善患者預後至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 178億美元 |

| 預測值 | 485億美元 |

| 複合年成長率 | 10.5% |

由於全球癌症負擔日益加重,預計到2034年,免疫組織化學(IHC)領域將以9.9%的複合年成長率成長。 IHC對於識別腫瘤標記、輔助治療方案選擇以及支持個人化醫療策略至關重要,鞏固了其在腫瘤診斷領域的地位。

受全球病毒和細菌感染發生率上升的推動,預計到2034年,傳染病領域將以11%的複合年成長率成長。實驗室自建檢測(LDT)的靈活性和快速週轉能力使其成為疫情防治和日常傳染病診斷不可或缺的工具。

2024年,美國實驗室自建檢測(LDT)市場規模預計將達到68億美元,這得益於其強大的醫院和參考實驗室網路,這些機構能夠開發和驗證複雜的檢測方法,尤其是在腫瘤學、傳染病和遺傳疾病領域。北美,特別是美國的監管環境歷來鼓勵LDT領域的創新,使實驗室能夠應對不斷出現的健康挑戰。人工智慧、自動化和新一代定序技術的整合持續推動著市場成長,使該地區成為先進診斷技術開發的領導者。

全球實驗室自建檢測(LDT)市場的主要企業包括IgX、Freenome、GUARDANT、HealthBio、veracyte、BioReference、MicroGenDX、prognomiQ、梅奧診所實驗室(MAYO CLINIC LABORATORIES)、SONIC HEALTHCARE USA和GeneDx。這些企業致力於持續創新,整合人工智慧、機器學習和新一代定序等尖端技術,以提高偵測準確性和縮短週轉時間。與醫院、研究機構和生技公司建立策略合作關係,有助於拓展檢測產品組合,加速市場進入。對生物資訊學和雲端運算的投資,促進了高級資料分析和患者資訊的無縫整合,從而提高診斷精度。此外,各企業也優先考慮合規性,並靈活適應不斷變化的醫療環境,以保持競爭優勢。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 癌症和遺傳性疾病發生率不斷上升

- 傳染病和慢性病盛行率不斷上升

- 人們越來越重視疾病早期檢測

- 技術進步

- 產業陷阱與挑戰

- 替代檢測方法的可用性

- 市場機遇

- 自動化與數位病理的融合

- 成長促進因素

- 成長潛力分析

- 報銷方案

- LDT定價模型及策略

- 臨床實驗室收費標準(CLFS)影響分析

- 聯邦醫療保險B部分承保範圍及報銷率

- 監管環境

- 技術格局

- 目前技術

- 新興技術

- 未來市場趨勢

- 價值鏈分析

- 消費者行為分析

- 投資環境

- 2024年定價分析

- 波特的分析

- PESTEL 分析

- 差距分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 聚合酶鍊式反應(PCR)

- 下一代定序(NGS)

- 免疫組織化學(IHC)

- 其他技術

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 腫瘤學

- 傳染病

- 遺傳及罕見疾病

- 心臟病學

- 自體免疫疾病與發炎性疾病

- 其他應用

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院實驗室

- 私人參考實驗室

- 專業診斷實驗室

- 其他最終用途

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ARUP Laboratories

- BioReference

- EXACT SCIENCES

- Freenome

- GeneDx

- GUARDANT

- HealthBio

- IgX

- Labcorp

- MAYO CLINIC LABORATORIES

- MicroGenDX

- prognomiQ

- Quest Diagnostics

- SONIC HEALTHCARE USA

- Veracyte

The Global Laboratory Developed Tests Market was valued at USD 17.8 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 48.5 billion by 2034.

The rapid growth is largely driven by increasing awareness around early disease detection, the rising prevalence of infectious and chronic illnesses, and a growing number of cancer and genetic disorder cases. LDTs, which are diagnostic tests created, manufactured, and used within a single laboratory, revolutionize personalized medicine, improving disease management and aiding clinical decision-making. Their ability to rapidly innovate and tailor tests to specific patient needs is transforming healthcare, especially in the context of complex conditions that require precise and individualized diagnostics. Companies offer an extensive range of tests, from advanced next-generation sequencing (NGS) panels to sophisticated molecular diagnostics and biomarker assays. These tests utilize state-of-the-art technologies, including high-throughput genomics, AI-driven algorithms, bioinformatics platforms, and cloud-enabled data integration. As cancer rates continue to climb, the demand for early, accurate, and personalized diagnostics intensifies. LDTs play a crucial role by enabling the swift detection of genetic mutations, biomarkers, and disease subtypes, which are vital for tailoring targeted treatments and enhancing patient outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.8 Billion |

| Forecast Value | $48.5 Billion |

| CAGR | 10.5% |

The immunohistochemistry (IHC) segment is anticipated to grow at a CAGR of 9.9% through 2034, due to the increasing global burden of cancer. IHC is essential for identifying tumor markers, assisting treatment choices, and supporting personalized medicine strategies, solidifying its place in oncology diagnostics.

The infectious diseases segment is expected to grow at a 11% CAGR through 2034, driven by the rising global incidence of viral and bacterial infections. The flexibility and rapid turnaround offered by LDTs make them indispensable for managing outbreaks and everyday infectious disease diagnosis.

U.S. Laboratory Developed Tests Market generated USD 6.8 billion in 2024, benefiting from a robust network of hospitals and reference labs capable of developing and validating complex tests, particularly in oncology, infectious diseases, and genetic conditions. The regulatory environment in North America, especially the U.S., has traditionally encouraged innovation in LDTs, allowing labs to respond to emerging health challenges. The integration of AI, automation, and next-generation sequencing technologies continues to fuel growth, establishing the region as a leader in advanced diagnostic development.

Leading companies in the Global Laboratory Developed Tests Market include IgX, Freenome, GUARDANT, HealthBio, veracyte, BioReference, MicroGenDX, prognomiQ, MAYO CLINIC LABORATORIES, SONIC HEALTHCARE USA, and GeneDx. Companies in the Laboratory Developed Tests Market focus on continuous innovation by integrating cutting-edge technologies such as AI, machine learning, and next-generation sequencing to enhance test accuracy and turnaround time. Strategic collaborations and partnerships with hospitals, research institutes, and biotech firms enable expanded test portfolios and faster market entry. Investments in bioinformatics and cloud computing facilitate advanced data analytics and seamless integration of patient information, improving diagnostic precision. Additionally, companies prioritize regulatory compliance and agile adaptation to changing health landscapes to maintain a competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of cancer and genetic disorders

- 3.2.1.2 Rising prevalence of infectious and chronic diseases

- 3.2.1.3 Growing awareness and focus on early disease detection

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Availability of alternative testing methods

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of automation & digital pathology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.4.1 LDT pricing models & strategies

- 3.4.2 Clinical laboratory fee schedule (CLFS) impact analysis

- 3.4.3 Medicare Part B coverage & reimbursement rates

- 3.5 Regulatory landscape

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Consumer behavior analysis

- 3.10 Investment landscape

- 3.11 Pricing analysis, 2024

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Polymerase chain reaction (PCR)

- 5.3 Next-generation sequencing (NGS)

- 5.4 Immunohistochemistry (IHC)

- 5.5 Other technologies

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Infectious diseases

- 6.4 Genetic & rare disorders

- 6.5 Cardiology

- 6.6 Autoimmune & inflammatory conditions

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital laboratories

- 7.3 Private reference labs

- 7.4 Specialty diagnostic labs

- 7.5 Other End use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ARUP Laboratories

- 9.2 BioReference

- 9.3 EXACT SCIENCES

- 9.4 Freenome

- 9.5 GeneDx

- 9.6 GUARDANT

- 9.7 HealthBio

- 9.8 IgX

- 9.9 Labcorp

- 9.10 MAYO CLINIC LABORATORIES

- 9.11 MicroGenDX

- 9.12 prognomiQ

- 9.13 Quest Diagnostics

- 9.14 SONIC HEALTHCARE USA

- 9.15 Veracyte

分析化驗服務市場:依分析方法、樣品類型、服務類型和最終用戶產業分類-2026-2032年全球市場預測臨床實驗室市場:按技術、檢測類型、產品類型、應用和最終用戶分類-2026-2032年全球市場預測

分析化驗服務市場:依分析方法、樣品類型、服務類型和最終用戶產業分類-2026-2032年全球市場預測臨床實驗室市場:按技術、檢測類型、產品類型、應用和最終用戶分類-2026-2032年全球市場預測 人類生物檢體市場規模、佔有率和成長分析:檢體類型、應用、最終用途、儲存類型、採購類型、地區和產業預測,2026-2033年

人類生物檢體市場規模、佔有率和成長分析:檢體類型、應用、最終用途、儲存類型、採購類型、地區和產業預測,2026-2033年 2026年全球臨床試驗生物樣本庫和存檔解決方案市場報告

2026年全球臨床試驗生物樣本庫和存檔解決方案市場報告 亞太地區人類生物檢體市場:分析與預測(2025-2035)

亞太地區人類生物檢體市場:分析與預測(2025-2035) 歐洲人類生物檢體市場:分析與預測(2025-2035)

歐洲人類生物檢體市場:分析與預測(2025-2035) 全球檢查室開發測試市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球檢查室開發測試市場規模、佔有率、趨勢和成長分析報告(2026-2034) 日本診斷檢測市場規模、佔有率、趨勢及預測(按提供者類型、檢測類型、產業、最終用戶和地區分類),2026-2034年

日本診斷檢測市場規模、佔有率、趨勢及預測(按提供者類型、檢測類型、產業、最終用戶和地區分類),2026-2034年 臨床試驗生物樣本庫及存檔解決方案市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、產品、地區和競爭對手分類,2021-2031年勞動市場:按就業類型、產業、技能水準、教育程度和年齡層別分類的全球預測 - 2026-2032 年

臨床試驗生物樣本庫及存檔解決方案市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、產品、地區和競爭對手分類,2021-2031年勞動市場:按就業類型、產業、技能水準、教育程度和年齡層別分類的全球預測 - 2026-2032 年