|

市場調查報告書

商品編碼

1871284

滾子軸承市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Roller Bearings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

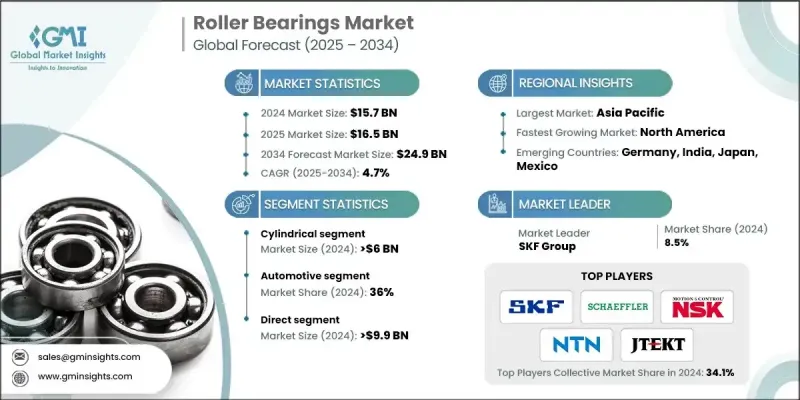

2024 年全球滾子軸承市場價值為 157 億美元,預計到 2034 年將以 4.7% 的複合年成長率成長至 249 億美元。

滾子軸承是建築、採礦和製造等行業不可或缺的關鍵零件,可靠性和耐用性是高效運作的關鍵。工業領域自動化和先進機械的日益普及,推動了對能夠承受重載、高壓和極端溫度變化的高性能軸承的需求。各國政府大力推廣工業自動化和節能系統,進一步促進了市場成長。隨著研發投入的不斷增加,滾子軸承也在不斷發展,以在嚴苛的工業環境中提供更高的性能、精度和使用壽命。支持再生能源和智慧製造的全球性舉措也持續影響著市場的發展,鼓勵著能夠提高效率和運作穩定性的創新。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 157億美元 |

| 預測值 | 249億美元 |

| 複合年成長率 | 4.7% |

2024年,圓柱滾子軸承市場規模預計將達到60億美元,這主要得益於市場對能夠承受重徑向負荷並在高速下高效運行的軸承的需求。這些軸承廣泛應用於工業電機、製造業和汽車系統。僅工業電機一項就佔製造業總能耗的一半以上,而圓柱滾子軸承在提高其運行效率方面發揮著至關重要的作用,因此,各行各業對這類軸承的需求強勁,因為它們都致力於節能減排,降低維護成本。

2024年,直銷通路市場規模達到99億美元,憑藉其與原始設備製造商(OEM)建立直接合作關係的有效性,在滾輪軸承市場佔據主導地位。直銷模式使製造商能夠提供客製化解決方案,同時確保順暢的溝通和技術協作。這種模式在汽車、航太和重型設備製造等高價值產業尤其有利,因為在這些產業中,精準度、品質保證和性能可靠性是OEM的關鍵決策因素。

2024年,美國滾子軸承市佔率達77.1%。美國先進的製造業生態系統、強大的汽車產業基礎以及不斷發展的航太和重型機械產業是推動這一成長的主要因素。持續的技術發展和主要行業參與者的存在鞏固了美國在該地區的主導地位,從而支撐了國內外對工業級滾子軸承的需求。

全球滾子軸承市場的主要參與者包括NBI Bearings Europe、HKT Bearings、C&U Group、美蓓亞、NTN、NSK、SKF、舍弗勒集團、鐵姆肯公司、RBC Bearings、Brammer、大同金屬、哈爾濱軸承製造、捷太格特和Rexnord。滾子軸承市場的企業致力於技術創新、產品多元化和策略合作,以鞏固其全球地位。對研發的大量投入使他們能夠開發出先進、高耐久性的軸承,即使在極端條件下也能高效運作。許多企業正在採用自動化和智慧製造流程來提高精度並降低生產成本。與工業、汽車和航太領域的原始設備製造商 (OEM) 的合作確保了長期合約和產品客製化機會。擴大區域製造基地和供應鏈有助於加快交貨速度並提高成本效益。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 工業擴張和自動化

- 汽車產業成長

- 技術進步與產品創新

- 產業陷阱與挑戰

- 高昂的生產成本

- 替代技術的出現

- 機會

- 節能智慧型滾子軸承系統

- 工業自動化和智慧製造的成長

- 成長促進因素

- 成長潛力分析

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監管環境

- 標準和合規要求

- 區域監理框架

- 認證標準

- 貿易統計(HS編碼-8482)

- 主要進口國

- 主要出口國

- 差距分析

- 風險評估與緩解

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依類型分類,2021-2034年

- 主要趨勢

- 圓柱形

- 錐

- 球形

- 其他

- 針

- 推力

- 分裂

第6章:市場估算與預測:依材料分類,2021-2034年

- 主要趨勢

- 鋼

- 陶瓷製品

- 聚合物

- 混合

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 變速箱

- 電動機

- 泵浦和壓縮機

- 風力渦輪機

- 傳送帶

- 工具機

第8章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 汽車

- 農業

- 電力

- 採礦與建築

- 鐵路與航太

- 汽車售後市場

- 其他

第9章:市場估算與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 直接的

- 間接

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Brammer

- C&U Group

- Daido Metal

- Harbin Bearing Manufacturing

- HKT Bearings

- JTEKT

- Minebea

- NBI軸承歐洲

- NSK

- NTN

- RBC Bearings

- Rexnord

- Schaeffler Group

- SKF

- The Timken Company

The Global Roller Bearings Market was valued at USD 15.7 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 24.9 billion by 2034.

Roller bearings serve as essential components across industries such as construction, mining, and manufacturing, where reliability and durability are key to efficient operations. The growing adoption of automation and advanced machinery across industrial sectors has driven the need for high-performance bearings capable of handling heavy loads, high pressure, and extreme temperature variations. Governments promoting industrial automation and energy-efficient systems are further fueling market growth. With increased focus on research and development, roller bearings are evolving to deliver improved performance, precision, and longevity in demanding industrial environments. Global initiatives supporting renewable energy and smart manufacturing also continue to influence the market's evolution, encouraging innovations that enhance efficiency and operational stability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.7 Billion |

| Forecast Value | $24.9 Billion |

| CAGR | 4.7% |

The cylindrical roller bearing segment reached USD 6 billion in 2024, driven by demand for bearings that support heavy radial loads and perform efficiently at high speeds. These bearings are widely adopted in industrial motors, manufacturing, and automotive systems. Industrial motors alone account for more than half of total energy consumption in manufacturing, and cylindrical bearings play a crucial role in improving their operational efficiency, thereby driving strong demand across industries seeking energy savings and reduced maintenance costs.

The direct sales segment reached USD 9.9 billion in 2024, dominating the roller bearings market due to its effectiveness in maintaining direct partnerships with OEMs. Direct distribution enables manufacturers to deliver customized solutions while ensuring seamless communication and technical collaboration. This approach is particularly beneficial in high-value sectors such as automotive, aerospace, and heavy equipment manufacturing, where precision, quality assurance, and performance reliability are key decision factors for OEMs.

U.S. Roller Bearings Market held 77.1% share in 2024. The country's advanced manufacturing ecosystem, strong automotive base, and expanding aerospace and heavy machinery sectors are major contributors to this growth. Continuous technological development and the presence of key industry players have reinforced the U.S. as a dominant force in the region, supporting both domestic and global demand for industrial-grade roller bearings.

Major players in the Global Roller Bearings Market include NBI Bearings Europe, HKT Bearings, C&U Group, Minebea, NTN, NSK, SKF, Schaeffler Group, The Timken Company, RBC Bearings, Brammer, Daido Metal, Harbin Bearing Manufacturing, JTEKT, and Rexnord. Companies in the Roller Bearings Market are focused on technological innovation, product diversification, and strategic partnerships to strengthen their global presence. Heavy investment in R&D enables them to develop advanced, high-durability bearings that perform efficiently under extreme conditions. Many players are adopting automation and smart manufacturing processes to improve precision and reduce production costs. Collaborations with OEMs across industrial, automotive, and aerospace sectors ensure long-term contracts and product customization opportunities. Expanding regional manufacturing bases and supply chains allows for faster delivery and cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Application

- 2.2.5 End use Industry

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial expansion and automation

- 3.2.1.2 Automotive industry growth

- 3.2.1.3 Technological advancements and product innovation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Emergence of alternative technologies

- 3.2.3 Opportunities

- 3.2.3.1 Energy-efficient and smart roller bearing systems

- 3.2.3.2 Growth in industrial automation and smart manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code-8482)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Cylindrical

- 5.3 Tapered

- 5.4 Spherical

- 5.5 Others

- 5.5.1 Needle

- 5.5.2 Thrust

- 5.5.3 Split

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Ceramic

- 6.4 Polymer

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Gearboxes

- 7.3 Electric Motors

- 7.4 Pumps & Compressors

- 7.5 Wind Turbines

- 7.6 Conveyors

- 7.7 Machine Tools

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Agriculture

- 8.4 Electrical

- 8.5 Mining & Construction

- 8.6 Railway & Aerospace

- 8.7 Automotive aftermarket

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Brammer

- 11.2 C&U Group

- 11.3 Daido Metal

- 11.4 Harbin Bearing Manufacturing

- 11.5 HKT Bearings

- 11.6 JTEKT

- 11.7 Minebea

- 11.8 NBI Bearings Europe

- 11.9 NSK

- 11.10 NTN

- 11.11 RBC Bearings

- 11.12 Rexnord

- 11.13 Schaeffler Group

- 11.14 SKF

- 11.15 The Timken Company

全球滾輪軸承環市場(按產品類型、材料、尺寸範圍、應用、最終用途產業和分銷管道分類)預測(2026-2032年)全球十字錐形滾柱軸承市場(按產品類型、分銷管道、材料、尺寸、最終用途產業和應用分類)預測(2026-2032年)

全球滾輪軸承環市場(按產品類型、材料、尺寸範圍、應用、最終用途產業和分銷管道分類)預測(2026-2032年)全球十字錐形滾柱軸承市場(按產品類型、分銷管道、材料、尺寸、最終用途產業和應用分類)預測(2026-2032年) 2026年全球滾輪軸承市場報告2026年全球滾針滾輪軸承市場報告2026年全球滾錐軸承市場報告2026年全球球面滾子軸承市場報告全球滾針推力軸承市場按類型、配置、材料、潤滑方式、承載能力和應用進行分類-2026-2032年預測精密滾針滾輪軸承市場按產品類型、保持架設計、潤滑類型和產業垂直領域分類-全球預測,2026-2032年

2026年全球滾輪軸承市場報告2026年全球滾針滾輪軸承市場報告2026年全球滾錐軸承市場報告2026年全球球面滾子軸承市場報告全球滾針推力軸承市場按類型、配置、材料、潤滑方式、承載能力和應用進行分類-2026-2032年預測精密滾針滾輪軸承市場按產品類型、保持架設計、潤滑類型和產業垂直領域分類-全球預測,2026-2032年 全球混合陶瓷球軸承市場洞察及預測(至2031年)

全球混合陶瓷球軸承市場洞察及預測(至2031年) 氮化矽軸承球:全球市佔率及排名、總收入及需求預測(2025-2031)

氮化矽軸承球:全球市佔率及排名、總收入及需求預測(2025-2031)