|

市場調查報告書

商品編碼

1871278

人工智慧在診斷領域的市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Artificial Intelligence In Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

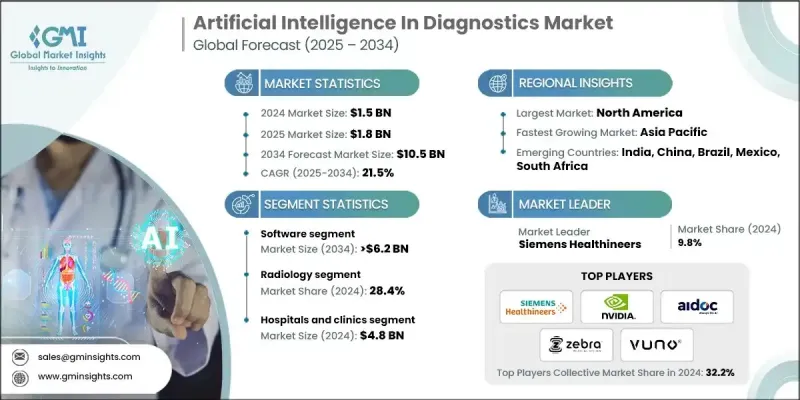

2024 年全球人工智慧診斷市場價值為 15 億美元,預計到 2034 年將以 21.5% 的複合年成長率成長至 105 億美元。

市場成長的驅動力來自對疾病早期檢測、人工智慧在醫學影像中的應用、精準診斷以及合規性提升等方面的日益成長的需求。人工智慧解決方案正幫助醫療服務提供者、支付方、生命科學機構和醫療技術公司改善患者預後、最佳化營運並滿足合規標準。關鍵解決方案包括基於人工智慧的影像和診斷軟體、數位病理平台以及預測分析工具,這些工具能夠自動識別疾病、輔助制定精準的治療方案並提升醫療品質。雲端人工智慧應用、數位病理和預測建模技術的進步正在拓展人工智慧在放射學、心臟病學、腫瘤學和病理學等領域的應用。監管機構的批准和相關框架鼓勵將人工智慧融入臨床工作流程,進一步推動了市場普及。醫療機構、技術供應商和生命科學公司之間不斷增加的研究投入和策略合作正在推動創新,並加速人工智慧在全球的應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15億美元 |

| 預測值 | 105億美元 |

| 複合年成長率 | 21.5% |

2024年,診斷實驗室領域的市場規模達到3.561億美元,預計到2034年將以22.3%的複合年成長率成長。由於實驗室在各種臨床應用中發揮著至關重要的作用,例如篩檢、分析和報告醫療結果,因此它們是人工智慧技術的主要使用者。日益複雜的工作流程、不斷成長的樣本量以及對高通量檢測的需求,都在推動對人工智慧驅動的自動化和決策支援系統的需求。

2024年,放射學領域佔據了28.4%的市場佔有率,預計到2034年將達到30億美元。由於迫切需要快速、精準的影像分析以早期發現疾病,放射學在診斷市場中引領人工智慧的發展。慢性病和急性病患病率的不斷上升,也推高了對醫學影像檢查的需求。基於人工智慧的放射學解決方案能夠自動解讀影像,最大限度地減少人為錯誤,並更快提供結果,從而支援及時制定治療方案。

2024年,北美人工智慧診斷市場佔40.7%的佔有率。該地區的領先地位歸功於其先進的醫療基礎設施、數位技術的廣泛應用以及大量的研發投入。人工智慧驅動的醫學影像、預測分析和數位病理平台已在醫院、診所和實驗室廣泛普及。此外,包括心血管疾病、癌症和神經系統疾病在內的慢性病盛行率不斷上升,也推動了該地區對早期精準診斷的需求。

全球全球診斷市場的主要參與者包括Aidoc、AliveCor、Digital Diagnostics、Enlitic、HeartFlow、Imagen、NVIDIA、PathAI、Qure.ai、Riverain Technologies、西門子醫療、Sophia Genetics、Tempus、Ultromics、Viz.ai、Vuno和Zebra Vision。為了鞏固自身地位,人工智慧診斷市場的企業正在實施多種策略。這些策略包括:擴大研發能力以創新人工智慧演算法並提高預測準確性;與醫療服務提供者、實驗室和科技公司建立策略合作夥伴關係;以及收購小型公司以增強技術組合。許多企業正致力於遵守監管規定並獲得批准,以加速市場准入。此外,企業還優先考慮基於雲端和軟體即服務(SaaS)的解決方案,以拓展市場並提供可擴展、方便用戶使用的平台。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 慢性病盛行率上升

- 對人工智慧工具的需求不斷成長

- 技術進步

- 政府的利多措施和資金

- 產業陷阱與挑戰

- 高昂的採購和維護成本

- 資料隱私和安全問題

- 市場機遇

- 新興經濟體的擴張

- 與遠距醫療和遠距診斷的整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 技術格局

- 當前技術趨勢

- 人工智慧驅動的放射學和病理學成像軟體

- 用於快速異常檢測的機器學習演算法

- 與醫院工作流程整合的數位病理平台

- 新興技術

- 人工智慧驅動的多模態成像技術用於綜合診斷

- 用於早期癌症和慢性病檢測的深度學習演算法

- 面向可擴展診斷解決方案的雲端人工智慧平台

- 當前技術趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

- 人工智慧診斷在新興市場的擴展

- 與遠距醫療和遠距患者監測相結合

- 利用人工智慧洞察力實現精準醫療和個人化醫療的普及

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新服務類型推出

- 擴張計劃

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 軟體

- 服務

- 硬體

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 放射科

- 腫瘤學

- 心臟病學

- 神經病學

- 病理

- 傳染病

- 其他應用

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和診所

- 診斷實驗室

- 影像中心

- 其他最終用途

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Aidoc

- AliveCor

- Digital Diagnostics

- Enlitic

- HeartFlow

- Imagen

- NVIDIA

- PathAI

- Qure.ai

- Riverain Technologies

- Siemens Healthineers

- Sophia Genetics

- Tempus

- Ultromics

- Viz.ai

- Vuno

- Zebra Medical Vision

The Global Artificial Intelligence In Diagnostics Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 10.5 billion by 2034.

The market is being propelled by increasing demand for early disease detection, AI integration in medical imaging, precision diagnostics, and regulatory compliance facilitation. AI-powered solutions are enabling healthcare providers, payers, life sciences organizations, and health technology companies to improve patient outcomes, optimize operations, and meet compliance standards. Key solutions include AI-based imaging and diagnostic software, digital pathology platforms, and predictive analytics tools that automate disease identification, assist in accurate treatment planning, and enhance care quality. Advancements in cloud-based AI applications, digital pathology, and predictive modeling are broadening the use of AI across radiology, cardiology, oncology, and pathology. Market adoption is further supported by regulatory approvals and frameworks that encourage the integration of AI into clinical workflows. Increasing research investments and strategic partnerships among healthcare institutions, technology providers, and life sciences firms are driving innovation and accelerating adoption worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 21.5% |

The diagnostic laboratories segment generated USD 356.1 million in 2024 and is expected to grow at a CAGR of 22.3% through 2034. Laboratories are major users of AI technologies due to their critical role in screening, analyzing, and reporting medical results across a variety of clinical applications. Rising workflow complexity, growing sample volumes, and the need for high-throughput testing are driving the demand for AI-driven automation and decision support systems.

The radiology segment held a 28.4% share in 2024 and is projected to reach USD 3 billion by 2034. Radiology leads the Artificial Intelligence in the diagnostics market because of the urgent need for rapid and precise imaging analysis to detect diseases at early stages. The increasing prevalence of chronic and acute conditions has raised the demand for medical imaging tests. AI-based radiology solutions automate image interpretation, minimize human error, and deliver faster results, enabling timely treatment decisions.

North America Artificial Intelligence In Diagnostics Market held a 40.7% share in 2024. The region's leadership is attributed to advanced healthcare infrastructure, widespread adoption of digital technologies, and significant research and development investments. AI-driven medical imaging, predictive analytics, and digital pathology platforms are widely available across hospitals, clinics, and laboratories. Additionally, the growing prevalence of chronic conditions, including cardiovascular diseases, cancer, and neurological disorders, is driving demand for early and precise diagnostics in the region.

Key players operating in the Global Artificial Intelligence In Diagnostics Market include Aidoc, AliveCor, Digital Diagnostics, Enlitic, HeartFlow, Imagen, NVIDIA, PathAI, Qure.ai, Riverain Technologies, Siemens Healthineers, Sophia Genetics, Tempus, Ultromics, Viz.ai, Vuno, and Zebra Medical Vision. To strengthen their position, companies in the Artificial Intelligence In Diagnostics Market are implementing a variety of strategies. These include expanding research and development capabilities to innovate new AI algorithms and improve predictive accuracy, forming strategic partnerships with healthcare providers, laboratories, and technology firms, and acquiring smaller companies to enhance technological portfolios. Many organizations are focusing on regulatory compliance and obtaining approvals to accelerate market entry. Companies are also prioritizing cloud-based and software-as-a-service solutions to reach broader markets while offering scalable, user-friendly platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Increasing demand for AI tools

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favourable government initiatives and funding

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procurement and maintenance costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging economies

- 3.2.3.2 Integration with telemedicine and remote diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 AI-powered radiology and pathology imaging software

- 3.5.1.2 Machine learning algorithms for rapid anomaly detection

- 3.5.1.3 Digital pathology platforms integrated with hospital workflows

- 3.5.2 Emerging technologies

- 3.5.2.1 AI-driven multi-modal imaging for integrated diagnostics

- 3.5.2.2 Deep learning algorithms for early cancer and chronic disease detection

- 3.5.2.3 Cloud-based AI platforms for scalable diagnostics solutions

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Expansion of AI diagnostics in emerging markets

- 3.9.2 Integration with telemedicine and remote patient monitoring

- 3.9.3 Adoption of precision and personalized medicine using AI insights

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.4 Hardware

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Radiology

- 6.3 Oncology

- 6.4 Cardiology

- 6.5 Neurology

- 6.6 Pathology

- 6.7 Infectious diseases

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Diagnostic laboratories

- 7.4 Imaging centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aidoc

- 9.2 AliveCor

- 9.3 Digital Diagnostics

- 9.4 Enlitic

- 9.5 HeartFlow

- 9.6 Imagen

- 9.7 NVIDIA

- 9.8 PathAI

- 9.9 Qure.ai

- 9.10 Riverain Technologies

- 9.11 Siemens Healthineers

- 9.12 Sophia Genetics

- 9.13 Tempus

- 9.14 Ultromics

- 9.15 Viz.ai

- 9.16 Vuno

- 9.17 Zebra Medical Vision

2026年全球人工智慧醫療記錄軟體市場報告2026年全球人工智慧(AI)磁振造影(MRI)病灶檢測市場報告2026年全球人工智慧(AI)視網膜篩檢設備市場報告2026年超音波影像成像人工智慧(AI)全球市場報告

2026年全球人工智慧醫療記錄軟體市場報告2026年全球人工智慧(AI)磁振造影(MRI)病灶檢測市場報告2026年全球人工智慧(AI)視網膜篩檢設備市場報告2026年超音波影像成像人工智慧(AI)全球市場報告 2026-2030年全球人工智慧輻射分流系統市場2026年全球人工智慧醫療診斷市場報告

2026-2030年全球人工智慧輻射分流系統市場2026年全球人工智慧醫療診斷市場報告 人工智慧醫療診斷應用市場(至2040年):依部署類型、應用、最終用戶和主要地區劃分 - 行業趨勢和全球預測2026年人工智慧(AI)增強型手術影像分析全球市場報告2026年人工智慧(AI)耳鏡影像分流平台全球市場報告2026年全球人工智慧顯微鏡市場報告

人工智慧醫療診斷應用市場(至2040年):依部署類型、應用、最終用戶和主要地區劃分 - 行業趨勢和全球預測2026年人工智慧(AI)增強型手術影像分析全球市場報告2026年人工智慧(AI)耳鏡影像分流平台全球市場報告2026年全球人工智慧顯微鏡市場報告