|

市場調查報告書

商品編碼

1871213

智慧交通號誌通訊模組市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Smart Traffic Signal Communication Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

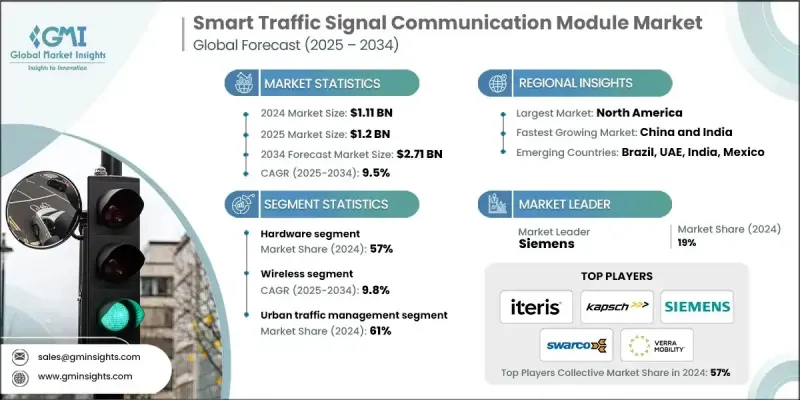

2024 年全球智慧交通號誌通訊模組市場價值為 11.1 億美元,預計到 2034 年將以 9.5% 的複合年成長率成長至 27.1 億美元。

由於智慧交通系統和智慧城市計畫的廣泛應用,市場正經歷強勁擴張。世界各國政府都在優先發展互聯基礎設施,以最大限度地減少交通堵塞、提高道路安全並即時最佳化交通號誌配時。這些進步正在將傳統的交通系統轉變為高度響應、數據驅動的網路。快速的城市化進程和對高效出行解決方案的需求也推動了對通訊模組的投資,這些模組將訊號燈、感測器和控制系統連接起來,覆蓋整個道路網路。人工智慧、機器學習和邊緣運算與交通管理系統的日益融合,使得預測控制和對交通狀況的自適應響應成為可能,從而顯著提高了營運效率。同時,物聯網賦能的智慧出行生態系統和基於雲端的交通控制解決方案的興起,正在加速向集中式、以數據為中心的交通網路轉型,以應對日益複雜的城市出行需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 11.1億美元 |

| 預測值 | 27.1億美元 |

| 複合年成長率 | 9.5% |

智慧交通號誌通訊模組產業正迅速從固定時序系統向自適應、人工智慧驅動的架構轉型,後者利用即時資料分析。這些智慧型系統能夠根據即時交通狀況自動調整號誌模式,進而緩解交通堵塞,提高交叉口通行效率。邊緣運算的部署實現了本地資料處理,可進行即時調整,增強響應速度,同時最大限度地減少對雲端基礎架構的依賴。此外,物聯網平台和雲端管理工具的整合支援對大型城市網路進行統一控制,幫助城市規劃者更有效率地監控、分析和最佳化訊號運作。

2024年,硬體部分佔據了57%的市場。感測器、處理器、路側單元和收發器等硬體組件構成了通訊模組的核心,這些模組負責即時傳輸和處理交通資料。全球範圍內的大型基礎設施現代化項目為該領域的成長提供了強勁動力,這些項目包括為沿著城市走廊和主要交通幹線安裝實體模組提供大量資金。全球持續推動道路網路現代化和智慧交叉路口建設,不斷催生了對可靠且可擴展的硬體解決方案的巨大需求。

預計2024年,城市交通管理領域將佔據61%的市場佔有率,成為主導應用領域。快速的城市化進程以及大都市地區日益嚴重的交通堵塞,正在推動自適應交通控制和交叉路口協調系統的應用。這些解決方案是現代智慧城市計畫的核心,有助於協調交通流量並提升安全性。隨著車聯網(V2X)通訊技術的日益普及,預計這一趨勢將進一步加速,因為連網車輛基礎設施正成為下一代交通生態系統不可或缺的一部分。

2024年,美國智慧交通號誌通訊模組市場規模達3.971億美元。在巨額公共資金和基礎設施更新計畫的支持下,美國仍然是互聯交通系統最成熟的市場之一。聯邦政府對智慧交通和互聯走廊項目的投資正在推動先進交通管理模組的大規模部署,使美國成為智慧交通創新和基礎設施現代化領域的全球領導者。

智慧交通號誌通訊模組市場的主要參與者包括泰雷茲(Thales)、Bosch)、Cubic、Econolite、Q-Free、西門子(Siemens)、Iteris、SWARCO、Verra Mobility 和 Kapsch TrafficCom。為了鞏固其在智慧交通號誌通訊模組市場的地位,該產業的企業正採取一系列策略舉措,重點在於創新、合作和全球擴張。許多企業正大力投資研發,以提高通訊可靠性、降低延遲並增強基於人工智慧的交通管理功能。與市政當局和技術提供者建立策略聯盟和合作夥伴關係,有助於加速互聯基礎設施的部署。製造商也在擴大生產能力並豐富產品組合,以滿足不同地區的市場需求。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預報

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 連網車輛和V2X基礎設施的日益部署

- 政府日益重視智慧城市和智慧交通系統的部署

- 日益嚴重的城市擁擠和安全措施

- 5G、人工智慧和邊緣運算技術的融合

- 產業陷阱與挑戰

- 高昂的安裝和整合成本

- 通訊協定缺乏互通性和標準化

- 市場機遇

- 擴大合作型智慧交通系統和互聯走廊項目

- 與雲端和邊緣分析平台整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利分析

- 永續性和環境方面

- 碳足跡評估

- 循環經濟一體化

- 電子垃圾管理要求

- 綠色製造計劃

- 用例和應用

- 最佳情況

- 資金和激勵分析

- 政府撥款和補貼

- 私部門投資趨勢

- 影響市場的公私合作項目

- 市場韌性與風險因素

- 硬體模組的供應鏈彈性

- 監理和合規風險評估

- 通訊網路中的網路安全風險

- 基準化分析和性能指標

- 提高交叉路口通行效率

- 減少行程時間和排放影響

- 自適應交通模組部署的投資報酬率

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 路側單元 (RSU)

- 感應器

- GPS單元

- 收發器

- 天線

- 軟體

- ATMS(進階交通管理系統)

- 基於雲端的分析

- 訊號控制最佳化平台

- 互通性/通訊協定軟體

- 服務

- 專業服務

- 託管服務

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 無線的

- DSRC / ITS-G5 (5.9 GHz)

- 蜂窩網路(5G/LTE)

- Wi-Fi(IEEE 802.11)

- 擴頻無線電

- 有線

- 光纖

- 雙絞線

- 同軸電纜

- V2X專用通訊系統

- 車對車(V2V)

- 車路協同(V2I)

- 基礎設施對基礎設施(I2I)

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 城市交通管理

- 城際/公路管理

- 互聯車輛與安全

- 其他

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 全球參與者

- Advantech

- Alstom

- Bosch

- Cisco Systems

- Cubic

- Denso

- Hitachi

- Huawei Technologies

- IBM

- Indra Sistemas

- Kapsch TrafficCom

9.1.12. L3 Harris Technologies

- 蒙迪斯

- 美國國家電氣公司

- 巴基斯坦電視台

- Q-Free

- 西門子

- 新科工程

- 泰萊達因FLIR系統

- 泰瑞茲

- 區域玩家

- 艾瑞恩

- 伊康諾萊特

- 埃夫肯

- GeoToll

- 伊特里斯

- SWARCO

- TransCore

- Verra Mobility

- 新興參與者/顛覆者

- 連接訊號

- Mobileye

The Global Smart Traffic Signal Communication Module Market was valued at USD 1.11 Billion in 2024 and is estimated to grow at a CAGR of 9.5% to reach USD 2.71 Billion by 2034.

The market is witnessing strong expansion due to the widespread adoption of intelligent transportation systems and smart city initiatives. Governments worldwide are prioritizing the development of connected infrastructure to minimize traffic congestion, enhance road safety, and optimize traffic signal timing in real time. These advancements are transforming traditional traffic systems into highly responsive, data-driven networks. Rapid urbanization and the need for efficient mobility solutions are also driving investments in communication modules that connect signals, sensors, and control systems across road networks. The increasing integration of artificial intelligence, machine learning, and edge computing into traffic management systems enables predictive control and adaptive responses to traffic conditions, significantly improving operational efficiency. Meanwhile, the rise of IoT-enabled smart mobility ecosystems and cloud-based traffic control solutions is accelerating the shift toward centralized, data-centric transportation networks capable of supporting the growing complexity of urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.11 Billion |

| Forecast Value | $2.71 Billion |

| CAGR | 9.5% |

The smart traffic signal communication module industry is rapidly transitioning from fixed-timing systems to adaptive, AI-powered architectures that utilize real-time data analytics. These intelligent systems can automatically adjust signal patterns based on live traffic conditions, reducing congestion and improving intersection efficiency. The deployment of edge computing allows local data processing for instant adjustments, enhancing responsiveness while minimizing dependence on cloud infrastructure. Furthermore, integrating IoT platforms and cloud-based management tools supports unified control across large urban networks, helping city planners monitor, analyze, and optimize signal operations more efficiently.

The hardware segment held 57% share in 2024. Hardware components such as sensors, processors, roadside units, and transceivers form the backbone of communication modules that transmit and process traffic data in real time. The segment's growth is strongly supported by major infrastructure modernization programs worldwide, which include significant funding for the installation of physical modules along urban corridors and key transportation routes. The ongoing global push to modernize road networks and establish smart intersections continues to create substantial demand for reliable and scalable hardware solutions.

The urban traffic management segment held a 61% share in 2024, making it the dominant application segment. Rapid urbanization, coupled with increasing congestion in metropolitan areas, is fueling the adoption of adaptive traffic control and intersection coordination systems. These solutions are central to modern smart city projects, helping to synchronize traffic flow and enhance safety. The growing implementation of vehicle-to-everything (V2X) communication technologies is expected to accelerate this trend further, as connected-vehicle infrastructure becomes an integral part of next-generation transportation ecosystems.

United States Smart Traffic Signal Communication Module Market generated USD 397.1 million in 2024. The country remains one of the most mature markets for connected traffic systems, supported by large-scale public funding and infrastructure renewal programs. Federal investments in intelligent transportation and connected corridor projects are driving large-scale deployment of advanced traffic management modules, establishing the U.S. as a global leader in smart mobility innovation and infrastructure modernization.

Prominent companies active in the Smart Traffic Signal Communication Module Market include Thales, Bosch, Cubic, Econolite, Q-Free, Siemens, Iteris, SWARCO, Verra Mobility, and Kapsch TrafficCom. To strengthen their Smart Traffic Signal Communication Module Market, companies in the smart traffic signal communication module industry are adopting a blend of strategic initiatives focused on innovation, collaboration, and global expansion. Many are investing heavily in R&D to enhance communication reliability, latency reduction, and AI-based traffic management features. Strategic alliances and partnerships with municipal governments and technology providers are helping accelerate the deployment of connected infrastructure. Manufacturers are also expanding their production capabilities and diversifying product portfolios to support varying regional requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising deployment of connected vehicle and V2X infrastructure

- 3.2.1.2 Increasing government focus on smart city and ITS deployments

- 3.2.1.3 Growing urban congestion and safety initiatives

- 3.2.1.4 Integration of 5G, AI, and edge computing technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and integration costs

- 3.2.2.2 Lack of interoperability and standardization in communication protocols

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of cooperative ITS and connected corridor projects

- 3.2.3.2 Integration with cloud and edge analytics platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability & environmental aspects

- 3.9.1 Carbon Footprint Assessment

- 3.9.2 Circular Economy Integration

- 3.9.3 E-Waste Management Requirements

- 3.9.4 Green Manufacturing Initiatives

- 3.10 Use cases and applications

- 3.11 Best-case scenario

- 3.12 Funding and incentive analysis

- 3.12.1 Government grants and subsidies

- 3.12.2 Private sector investment trends

- 3.12.3 Public-private partnership initiatives impacting the market

- 3.13 Market resilience and risk factors

- 3.13.1 Supply chain resilience for hardware modules

- 3.13.2 Regulatory and compliance risk assessment

- 3.13.3 Cybersecurity risks in communication networks

- 3.14 Benchmarking and performance metrics

- 3.14.1 Intersection efficiency improvements

- 3.14.2 Travel time reduction and emission impact

- 3.14.3 ROI from adaptive traffic module deployments

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 RSUs (Roadside Units)

- 5.2.2 Sensors

- 5.2.3 GPS units

- 5.2.4 Transceivers

- 5.2.5 Antennas

- 5.3 Software

- 5.3.1 ATMS (Advanced Traffic Management Systems)

- 5.3.2 Cloud-based analytics

- 5.3.3 Signal control optimization platforms

- 5.3.4 Interoperability/communication protocol software

- 5.4 Services

- 5.4.1 Professional Services

- 5.4.2 Managed Services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Wireless

- 6.2.1 DSRC / ITS-G5 (5.9 GHz)

- 6.2.2 Cellular (5G / LTE)

- 6.2.3 Wi-Fi (IEEE 802.11)

- 6.2.4 Spread spectrum radio

- 6.3 Wired

- 6.3.1 Fiber optics

- 6.3.2 Twisted-pair

- 6.3.3 Coaxial cables

- 6.4 V2X-Specific communication systems

- 6.4.1 Vehicle-to-Vehicle (V2V)

- 6.4.2 Vehicle-to-Infrastructure (V2I)

- 6.4.3 Infrastructure-to-Infrastructure (I2I)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Urban Traffic Management

- 7.3 Interurban / Highway Management

- 7.4 Connected Vehicles & Safety

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Advantech

- 9.1.2 Alstom

- 9.1.3 Bosch

- 9.1.4 Cisco Systems

- 9.1.5 Cubic

- 9.1.6 Denso

- 9.1.7 Hitachi

- 9.1.8 Huawei Technologies

- 9.1.9 IBM

- 9.1.10 Indra Sistemas

- 9.1.11 Kapsch TrafficCom

9.1.12. L3 Harris Technologies

- 9.1.13 Mundys

- 9.1.14 NEC

- 9.1.15 PTV

- 9.1.16 Q-Free

- 9.1.17 Siemens

- 9.1.18 ST Engineering

- 9.1.19 Teledyne FLIR Systems

- 9.1.20 Thales

- 9.2 Regional Players

- 9.2.1 Aireon

- 9.2.2 Econolite

- 9.2.3 EFKON

- 9.2.4 GeoToll

- 9.2.5 Iteris

- 9.2.6 SWARCO

- 9.2.7 TransCore

- 9.2.8 Verra Mobility

- 9.3 Emerging Players / Disruptors

- 9.3.1 Connected Signals

- 9.3.2 Mobileye

城市交通分析市場預測至2034年-全球分析(按組件、資料來源、分析類型、部署模式、應用、最終用戶和區域分類)

城市交通分析市場預測至2034年-全球分析(按組件、資料來源、分析類型、部署模式、應用、最終用戶和區域分類) 智慧型運輸管理系統(ITS)市場規模、佔有率和成長分析:按組件、部署類型、應用、最終用戶和地區分類-2026-2033年產業預測

智慧型運輸管理系統(ITS)市場規模、佔有率和成長分析:按組件、部署類型、應用、最終用戶和地區分類-2026-2033年產業預測 智慧交通分析市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、最終用戶、地區和競爭格局分類,2020-2030年預測

智慧交通分析市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、最終用戶、地區和競爭格局分類,2020-2030年預測 全球智慧交通分析市場

全球智慧交通分析市場 全球智慧城市 ATM 市場-按類型、應用、地區和預測的市場規模

全球智慧城市 ATM 市場-按類型、應用、地區和預測的市場規模 先進交通管理系統市場,按組件、按應用、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

先進交通管理系統市場,按組件、按應用、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 先進交通管理系統 (ATMS) 市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

先進交通管理系統 (ATMS) 市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測