|

市場調查報告書

商品編碼

1871205

航空航太絕緣用氣凝膠複合材料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Aerogel Composites for Aerospace Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

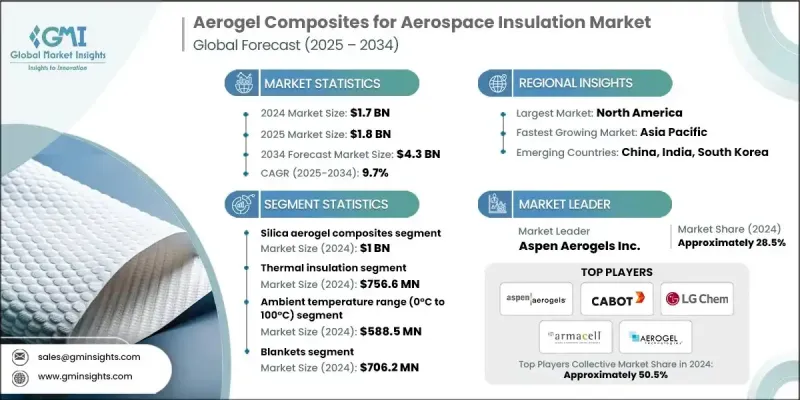

2024 年全球航空航太絕緣用航太複合材料市場價值為 17 億美元,預計到 2034 年將以 9.7% 的複合年成長率成長至 43 億美元。

航太業對輕量化、高性能隔熱系統的日益重視推動了市場成長,該系統廣泛應用於商用和國防飛機。氣凝膠複合材料具有卓越的隔熱性能,同時最大限度地減輕重量,有助於飛機在不影響結構完整性的前提下達到燃油效率目標。其優異的導熱性能,以及能夠承受從低溫到1200°C以上極端溫度的能力,使其成為下一代飛機和太空船應用的理想選擇。二氧化矽和聚合物基氣凝膠複合材料的進步提高了機械耐久性和加工效率,使其在航太熱管理領域中得到更廣泛的應用。纖維增強氣凝膠和聚醯亞胺氣凝膠的創新使其機械強度比傳統氣凝膠增加了數百倍,同時保持了良好的隔熱性能。對永續航空、電動飛機和電池熱管理的日益重視進一步推動了氣凝膠複合材料的應用,製造商正在尋找兼具輕量化和高性能隔熱性能的材料。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 17億美元 |

| 預測值 | 43億美元 |

| 複合年成長率 | 9.7% |

2024年,二氧化矽氣凝膠複合材料市場規模達10億美元,預計2025年至2034年將以9.9%的複合年成長率成長,佔60.2%的市場。二氧化矽基複合材料憑藉其超低導熱係數、結構穩定性和優異的耐火性能,在該領域佔據領先地位,使其適用於飛機引擎室、太空船熱系統和低溫燃料儲存。其在極端溫度條件下的卓越性能以及符合嚴格的航太防火標準,使其成為商業、軍事和航太領域關鍵隔熱應用的首選材料。

2024年,隔熱材料市場規模為7.566億美元,預計到2034年將以10%的複合年成長率成長,佔據45%的市場。該市場佔據主導地位的原因在於溫度控制在飛機引擎、太空船系統和低溫燃料密封等領域的關鍵作用。氣凝膠複合材料在極端環境下(從-200°C到500°C以上)都能維持優異的隔熱性能。航太應用領域對氣凝膠複合材料的需求尤其旺盛,因為在航太領域,隔熱系統必須能夠承受外太空嚴酷的溫度波動,同時保護設備和乘員艙的安全。

2024年,北美航空航太航太氣凝膠複合材料市佔率達42%。該地區的領先地位源於其擁有眾多大型航太製造商、先進的研究機構以及政府對國防和航太項目的巨額投資。美國擁有強大的航太生態系統,許多公司正積極將氣凝膠複合材料應用於飛機和太空船設計。政府資助的太空探索計畫和國防計畫也正在加速北美地區氣凝膠隔熱解決方案的技術發展和應用。

全球航太航太隔熱用氣凝膠複合材料市場的主要參與者包括FLEXcon、LG Chem、Armacell International、Blueshift Materials、Aspen Aerogels, Inc.、Active Aerogels、Aerogel Technologies LLC、EAS Fiberglass Co., Ltd.、Jucos Refractory、WH Thermalgel Technology、Green Earth Earth Technologies、Svenska, Ltd.、Jucos Refractory、WH Thermalgel Technology、Green Earth Earth Technologies、Svenska, Ltd。這些企業正採取多種策略方法來鞏固其市場地位。他們大力投資研發,以提高氣凝膠複合材料的強度、熱效率和可製造性。與航太航太原始設備製造商 (OEM) 和國防承包商建立戰略合作夥伴關係,有助於確保長期契約,並擴大其在商業、軍事和航太領域的應用。此外,各公司也致力於透過開發聚合物和纖維增強複合材料來豐富其產品組合,以滿足不斷變化的性能要求。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 供應鏈的複雜性

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 二氧化矽氣凝膠複合材料

- 碳氣凝膠複合材料

- 混合氣凝膠複合材料

- 聚合物氣凝膠複合材料

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 隔熱

- 隔音

- 消防

- 振動阻尼

第7章:市場估計與預測:依溫度範圍分類,2021-2034年

- 主要趨勢

- 低溫(-200°C 至 -100°C)

- 低溫(-100°C 至 0°C)

- 環境溫度(0°C 至 100°C)

- 高溫(100°C 至 500°C)

- 極端溫度(>500°C)

第8章:市場估算與預測:依形式分類,2021-2034年

- 主要趨勢

- 毯子

- 面板

- 塗層

- 自訂形狀

第9章:市場估算與預測:依製造流程分類,2021-2034年

- 主要趨勢

- 超臨界乾燥

- 常壓乾燥

- 冷凍乾燥

- 溶膠-凝膠加工

第10章:市場估計與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 商用飛機

- 軍用機

- 太空船

- 電動飛機

第11章:市場估計與預測:按地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第12章:公司簡介

- Aspen Aerogels, Inc.

- Cabot Corporation

- LG Chem

- Armacell International

- Aerogel Technologies LLC

- Blueshift Materials

- Svenska Aerogel Holding AB

- Active Aerogels

- Green Earth Aerogel Technologies

- FLEXcon

- EAS Fiberglass Co., Ltd.

- Guangdong Alison Technology

- Jucos Refractory

- WH Thermal Energy Technology

- Wedge India

The Global Aerogel Composites for Aerospace Insulation Market was valued at USD 1.7 Billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 4.3 Billion by 2034.

Market growth is driven by the aerospace industry's growing focus on lightweight, high-performance thermal protection systems for both commercial and defense aircraft. Aerogel composites offer exceptional thermal insulation while minimizing weight, helping aircraft meet fuel efficiency targets without compromising structural integrity. Their superior thermal conductivity, combined with the ability to endure extreme temperatures ranging from cryogenic conditions to above 1,200°C, makes them ideal for next-generation aircraft and spacecraft applications. Advances in silica and polymer-based aerogel composites have enhanced mechanical durability and processing efficiency, enabling broader implementation in aerospace thermal management. Innovations in fiber-reinforced and polyimide aerogels are improving mechanical strength by hundreds of times over conventional aerogels while retaining thermal performance. Increasing emphasis on sustainable aviation, electric aircraft, and battery thermal management is further propelling adoption, as manufacturers seek materials that combine lightweight properties with high-performance insulation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 billion |

| Forecast Value | $4.3 billion |

| CAGR | 9.7% |

The silica aerogel composites segment generated USD 1 Billion in 2024 and is projected to grow at a CAGR of 9.9% from 2025 to 2034, accounting for 60.2% of the market. Silica-based composites lead the segment due to their ultra-low thermal conductivity, structural stability, and excellent fire resistance, making them suitable for aircraft engine compartments, spacecraft thermal systems, and cryogenic fuel storage. Their proven performance in extreme temperature conditions and compliance with stringent aerospace fire standards have positioned them as the material of choice for critical thermal insulation applications across commercial, military, and space sectors.

The thermal insulation segment was valued at USD 756.6 million in 2024 and is expected to grow at a CAGR of 10% through 2034, capturing a 45% market share. This segment dominates due to the essential role of temperature control in aircraft engines, spacecraft systems, and cryogenic fuel containment. Aerogel composites excel in maintaining thermal performance across extreme environments, from -200°C to over 500°C. The demand is particularly high for space applications, where thermal protection systems must withstand the harsh temperature fluctuations of outer space while safeguarding equipment and crew compartments.

North America Aerogel Composites for Aerospace Insulation Market accounted for a 42% share in 2024. The region's leadership stems from the presence of major aerospace manufacturers, advanced research institutions, and substantial government investment in defense and aerospace programs. The U.S. benefits from a strong aerospace ecosystem, with companies actively integrating aerogel composites into aircraft and spacecraft designs. Government-funded space exploration initiatives and defense programs are also accelerating technological development and the application of aerogel-based thermal solutions in North America.

Leading players in the Global Aerogel Composites for Aerospace Insulation Market include FLEXcon, LG Chem, Armacell International, Blueshift Materials, Aspen Aerogels, Inc., Active Aerogels, Aerogel Technologies LLC, EAS Fiberglass Co., Ltd., Jucos Refractory, WH Thermal Energy Technology, Green Earth Aerogel Technologies, Svenska Aerogel Holding AB, Guangdong Alison Technology, and Wedge India. Companies in the Aerogel Composites for Aerospace Insulation Market are employing several strategic approaches to strengthen their presence and market position. They are investing heavily in R&D to enhance the material strength, thermal efficiency, and manufacturability of aerogel composites. Strategic partnerships with aerospace OEMs and defense contractors help secure long-term contracts and expand adoption in commercial, military, and space applications. Firms are also focusing on diversifying their product portfolio with polymer- and fiber-reinforced composites to meet evolving performance requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Application

- 2.2.3 Temperature range

- 2.2.4 Form

- 2.2.5 Manufacturing process

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Silica aerogel composites

- 5.3 Carbon aerogel composites

- 5.4 Hybrid aerogel composites

- 5.5 Polymer aerogel composites

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Thermal insulation

- 6.3 Acoustic insulation

- 6.4 Fire protection

- 6.5 Vibration damping

Chapter 7 Market Estimates and Forecast, By Temperature Range, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Cryogenic (-200°C to -100°C)

- 7.3 Low temperature (-100°C to 0°C)

- 7.4 Ambient (0°C to 100°C)

- 7.5 High temperature (100°C to 500°C)

- 7.6 Extreme temperature (>500°C)

Chapter 8 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Blankets

- 8.3 Panels

- 8.4 Coatings

- 8.5 Custom shapes

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Supercritical drying

- 9.3 Ambient pressure drying

- 9.4 Freeze drying

- 9.5 Sol-gel processing

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 Commercial aircraft

- 10.3 Military aircraft

- 10.4 Spacecraft

- 10.5 Electric aircraft

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East & Africa

Chapter 12 Company Profiles

- 12.1 Aspen Aerogels, Inc.

- 12.2 Cabot Corporation

- 12.3 LG Chem

- 12.4 Armacell International

- 12.5 Aerogel Technologies LLC

- 12.6 Blueshift Materials

- 12.7 Svenska Aerogel Holding AB

- 12.8 Active Aerogels

- 12.9 Green Earth Aerogel Technologies

- 12.10 FLEXcon

- 12.11 EAS Fiberglass Co., Ltd.

- 12.12 Guangdong Alison Technology

- 12.13 Jucos Refractory

- 12.14 WH Thermal Energy Technology

- 12.15 Wedge India

全球航太隔熱材料市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年)

全球航太隔熱材料市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年) 2026年全球航太隔熱材料市場報告

2026年全球航太隔熱材料市場報告 航太隔熱材料市場規模、佔有率和成長分析(按材料類型、隔熱形式、飛機、最終用戶和地區分類)—2026-2033年產業預測

航太隔熱材料市場規模、佔有率和成長分析(按材料類型、隔熱形式、飛機、最終用戶和地區分類)—2026-2033年產業預測 航太用隔熱材料的市場:市場規模,佔有率,趨勢,產業分析(各材料,各產品,各用途,各地區)與未來預測(2025年~2034年)

航太用隔熱材料的市場:市場規模,佔有率,趨勢,產業分析(各材料,各產品,各用途,各地區)與未來預測(2025年~2034年) 航太隔熱材料市場規模、佔有率、趨勢分析報告:按材料、產品、最終用途、地區和細分市場預測,2025 年至 2033 年按產品類型、材料、地區、範圍和預測劃分的全球航空航天絕緣市場規模

航太隔熱材料市場規模、佔有率、趨勢分析報告:按材料、產品、最終用途、地區和細分市場預測,2025 年至 2033 年按產品類型、材料、地區、範圍和預測劃分的全球航空航天絕緣市場規模