|

市場調查報告書

商品編碼

1871202

托盤搬運車市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Pallet Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球托盤搬運車市場價值為 338 億美元,預計到 2034 年將以 5.8% 的複合年成長率成長至 591 億美元。

倉儲自動化程度的提高、勞動力短缺的加劇以及物料搬運技術的不斷進步,正推動市場發生重大變革。托盤搬運車,包括手排、電動和自動導引車 (AGV),正成為全球物流運作中不可或缺的工具。 76% 的供應鏈企業表示面臨勞動力短缺,因此自動化已成為一項策略性需求。先進鋰離子電池的普及加速了這項變革,與傳統能源系統相比,鋰離子電池具有更高的效率、更長的使用壽命和更快的充電速度。製造商正在實現生產區域多元化,以增強供應鏈的韌性,同時,自動化、電池系統以及與倉儲管理技術的整合方面的創新也加劇了市場競爭。歐洲企業將能源效率和環保合規性作為關鍵的差異化優勢,而全球機器人和自動化領域的領導者則日益影響托盤搬運車的性能標準。這些因素共同塑造了一個高度動態且技術驅動的全球物料搬運生態系統。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 338億美元 |

| 預測值 | 591億美元 |

| 複合年成長率 | 5.8% |

2024年,手動托盤搬運車市場規模達到174億美元,預計2025年至2034年間將以5.1%的複合年成長率成長。手動托盤搬運車憑藉其價格實惠、操作簡單、維護成本低等優勢,持續佔據市場主導地位。中小企業和預算有限的企業尤其青睞手動托盤搬運車。其簡單的設計和易用性無需對操作人員進行大量培訓,從而降低了整體營運成本。在勞動成本較低的地區,手動托盤搬運車為物料搬運提供了一個高效經濟的解決方案,也促成了其在全球各行業持續旺盛的需求。

2024年,載重能力不超過2,000公斤的低載重托盤搬運車市場以139億美元的市場規模和41.1%的市佔率領跑。此細分市場的顯著成長主要歸功於其在零售場所、小型倉庫和輕工業設施的廣泛應用。這些搬運車經濟高效、結構緊湊,非常適合短距離運輸輕型貨物,因此對於空間有限或搬運需求較低的中小型企業來說尤其實用。其價格實惠且操作簡便,使其成為注重靈活性和成本效益的物流和製造環境中的理想之選。

2024年,美國托盤搬運車市場規模達79億美元,預計2025年至2034年將以5.9%的複合年成長率成長。倉儲、物流和電商配送網路的快速擴張推動了美國市場對托盤搬運車的需求。配送中心和倉儲樞紐對高效物料搬運解決方案的需求日益成長,也促進了托盤搬運車的普及。托盤搬運車正成為最佳化工作流程、提升工人安全和提高高產量作業效率的關鍵工具,使美國成為先進托盤搬運解決方案的領先市場之一。

全球托盤搬運車市場的主要企業包括HU-LIFT、豐田產業株式會社、永恆力股份公司、雷蒙德公司、杭叉、CUBLIFT、凱傲集團、諾寶力、皇冠設備公司、維斯蒂爾製造公司、豪華搬運、克拉克、南通奧曼實業、安徽合力以及海斯特-耶魯。托盤搬運車市場的領先製造商正採取多元化的策略來鞏固其全球競爭力。許多企業正大力投資研發,以提高自動化程度、電池效率和產品耐用性。各公司正致力於拓展其電動和半電動托盤搬運車產品組合,以滿足市場對永續和低排放設備日益成長的需求。與物流供應商和電商公司建立策略聯盟有助於擴大市場覆蓋範圍。此外,各公司也正在建立區域生產中心,以最大限度地降低供應鏈風險並最佳化交付週期。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 2024年定價分析

- 按地區和產品類型

- 原料成本

- 未來市場趨勢

- 風險評估與緩解

- 監理合規風險

- 產能限制影響分析

- 技術轉型風險

- 價格波動和成本上漲風險

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 手動托盤搬運車

- 步行式托盤搬運車

- 騎乘式托盤搬運車

- 高位托盤搬運車

- 剪叉式升降托盤車

- 其他(跨式托盤搬運車等)

第6章:市場估算與預測:依營運模式分類,2021-2034年

- 主要趨勢

- 手動托盤搬運車

- 半電動托盤搬運車

- 電動托盤搬運車

第7章:市場估計與預測:依產能分類,2021-2034年

- 主要趨勢

- 低容量(<2,000 公斤)

- 中等容量(2,000-4,000 公斤)

- 高容量(4,000-6,000 公斤)

- 超重型承重能力(>6,000 公斤)

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 倉儲和配送中心

- 製造設施

- 零售和電子商務經營

- 運輸與物流

- 其他(建築業、農業等)

第9章:市場估算與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 直銷

- 間接銷售

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- Anhui Heli

- CLARK

- Crown Equipment Corporation

- CUBLIFT

- Hangcha

- Howard Handling

- HU-LIFT

- Hyster-Yale

- Jungheinrich AG

- KION Group

- Nantong Allman Industry

- Noblelift

- The Raymond Corporation

- Toyota Industries Corporation

- Vestil Manufacturing Corp.

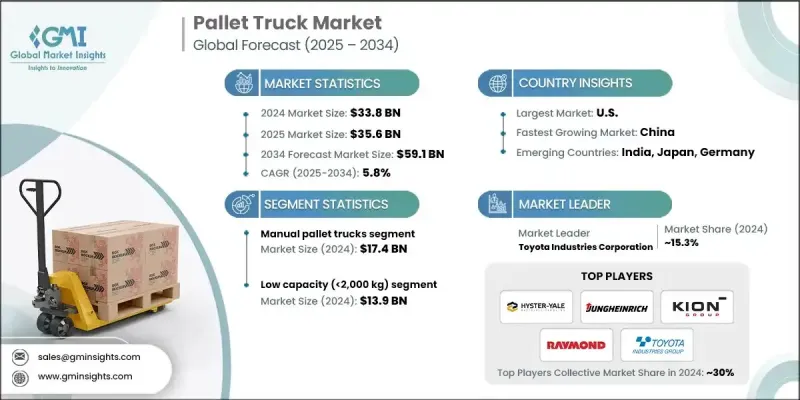

The Global Pallet Truck Market was valued at USD 33.8 Billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 59.1 Billion by 2034.

The market is undergoing a major evolution fueled by the rise of warehouse automation, growing labor shortages, and continuous advancements in material handling technologies. Pallet trucks, including manual, electric, and automated guided vehicles (AGVs), are becoming indispensable in logistics operations worldwide. With 76% of supply chain organizations reporting workforce shortages, automation has become a strategic necessity. The shift toward advanced lithium-ion batteries has accelerated this transformation, offering higher efficiency, longer operational life, and faster charging compared to traditional energy systems. Manufacturers are diversifying production across regions to strengthen supply chain resilience, while competition continues to intensify through innovations in automation, battery systems, and integration with warehouse management technologies. European companies are emphasizing energy efficiency and environmental compliance as key differentiators, while global robotics and automation leaders are increasingly influencing pallet truck performance standards. These combined factors are shaping a highly dynamic and technology-driven global material handling ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $33.8 Billion |

| Forecast Value | $59.1 Billion |

| CAGR | 5.8% |

The manual pallet truck segment generated USD 17.4 Billion in 2024 and is projected to grow at a CAGR of 5.1% between 2025 and 2034. Manual models continue to dominate the market based on their affordability, operational simplicity, and low maintenance costs. They are especially preferred by small and medium-sized enterprises (SMEs) and businesses operating with constrained budgets. Their uncomplicated design and ease of use eliminate the need for extensive operator training, reducing overall operational expenses. In regions with lower labor costs, manual pallet trucks provide an efficient and economical solution for material handling, which contributes to their sustained global demand across industries.

The low-capacity pallet truck segment, handling up to 2,000 kg, led the market in 2024 with USD 13.9 Billion and captured a 41.1% share. This segment's prominence is attributed to its strong adoption across retail spaces, small warehouses, and light industrial facilities. These trucks are cost-efficient, compact, and ideal for short-distance transport of lighter loads, making them especially practical for SMEs and enterprises with limited space or lower handling requirements. Their affordability and ease of operation make them a versatile choice in logistics and manufacturing environments that prioritize flexibility and cost-effectiveness.

U.S. Pallet Truck Market reached USD 7.9 Billion in 2024 and is projected to grow at a CAGR of 5.9% from 2025 to 2034. Demand in the country is accelerating due to the rapid expansion of warehousing, logistics, and e-commerce distribution networks. The increased need for efficient material movement solutions in fulfillment centers and storage hubs is driving adoption. Pallet trucks are becoming essential tools in optimizing workflows, enhancing worker safety, and improving productivity in high-volume operations, positioning the U.S. as one of the leading markets for advanced pallet handling solutions.

Key companies operating in the Global Pallet Truck Market include HU-LIFT, Toyota Industries Corporation, Jungheinrich AG, The Raymond Corporation, Hangcha, CUBLIFT, KION Group, Noblelift, Crown Equipment Corporation, Vestil Manufacturing Corp., Howard Handling, CLARK, Nantong Allman Industry, Anhui Heli, and Hyster-Yale. Leading manufacturers in the Pallet Truck Market are adopting diverse strategies to strengthen their competitive position globally. Many are investing heavily in research and development to enhance automation, battery efficiency, and product durability. Companies are focusing on expanding their electric and semi-electric pallet truck portfolios to meet growing demand for sustainable and low-emission equipment. Strategic alliances with logistics providers and e-commerce companies are helping to expand market reach. Firms are also establishing regional production hubs to minimize supply chain risks and optimize delivery timelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Mode of Operation trends

- 2.2.3 Capacity trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

- 2.5 Strategic recommendations

- 2.5.1 Supply chain diversification strategy

- 2.5.2 Product portfolio enhancement

- 2.5.3 Partnership and alliance opportunities

- 2.5.4 Cost management and pricing strategy

- 2.6 Decision framework

- 2.6.1 Investment priority matrix

- 2.6.2 Risk-adjusted ROI analysis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.4.1 By region and product type

- 3.4.2 Raw material cost

- 3.5 Future market trends

- 3.6 Risk assessment and mitigation

- 3.6.1 Regulatory compliance risks

- 3.6.2 Capacity constraint impact analysis

- 3.6.3 Technology transition risks

- 3.6.4 Pricing volatility and cost escalation risks

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Hand Pallet Trucks

- 5.3 Walkie Pallet Trucks

- 5.4 Rider Pallet Trucks

- 5.5 High-Lift Pallet Trucks

- 5.6 Scissor Lift Pallet Trucks

- 5.7 Others (Straddle Pallet Trucks, etc.)

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual Pallet Trucks

- 6.3 Semi-Electric Pallet Trucks

- 6.4 Electric Pallet Trucks

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low Capacity (<2,000 kg)

- 7.3 Medium Capacity (2,000-4,000 kg)

- 7.4 High Capacity (4,000-6,000 kg)

- 7.5 Extra Heavy Capacity (>6,000 kg)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Warehousing and Distribution Centers

- 8.3 Manufacturing Facilities

- 8.4 Retail and E-commerce Operations

- 8.5 Transportation and Logistics

- 8.6 Others (Construction, Agriculture, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 U.K.

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Anhui Heli

- 11.2 CLARK

- 11.3 Crown Equipment Corporation

- 11.4 CUBLIFT

- 11.5 Hangcha

- 11.6 Howard Handling

- 11.7 HU-LIFT

- 11.8 Hyster-Yale

- 11.9 Jungheinrich AG

- 11.10 KION Group

- 11.11 Nantong Allman Industry

- 11.12 Noblelift

- 11.13 The Raymond Corporation

- 11.14 Toyota Industries Corporation

- 11.15 Vestil Manufacturing Corp.