|

市場調查報告書

商品編碼

1871181

2nm及以下半導體節點市場機會、成長促進因素、產業趨勢分析及2025-2034年預測2nm and Beyond Semiconductor Node Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

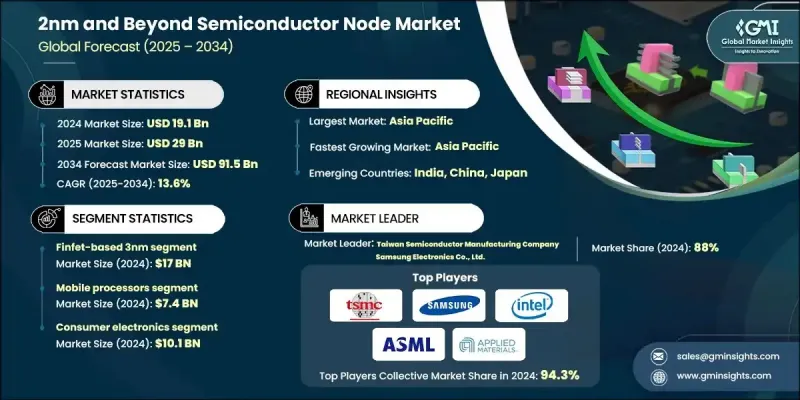

2024 年全球 2nm 及以下半導體節點市值為 191 億美元,預計到 2034 年將以 13.6% 的複合年成長率成長至 915 億美元。

市場成長主要受高效能運算需求上升、人工智慧應用範圍擴大、5G和邊緣運算發展以及下一代消費性電子產品創新不斷湧現的推動。政府支持的激勵措施和公共投資進一步加速了市場發展勢頭。人工智慧和機器學習的廣泛應用正推動半導體產業發生重大變革,從而對採用先進的2奈米及以下製程製程製造的超高效、高性能邏輯晶片的需求日益成長。隨著人工智慧領域的支出持續快速成長,這股創新浪潮將重塑運算能力,為高效能、高能源效率晶片技術創造新的機會。 5G基礎設施的擴展和邊緣運算的日益普及,進一步加劇了對更小、更快、更有效率晶片的需求,從而推動了2奈米技術在全球各行業的應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 191億美元 |

| 預測值 | 915億美元 |

| 複合年成長率 | 13.6% |

受人工智慧、5G、自動駕駛系統和高效能運算應用領域對先進晶片架構日益成長的需求推動,英特爾埃格斯特朗級製程預計將在2025年至2034年間以20.6%的複合年成長率成長。持續提升晶片能源效率、小型化和可擴展性對於維持技術進步的步伐至關重要。對下一代製程技術的持續投資對於滿足新興數位生態系統對更快、更智慧、更節能的半導體解決方案的需求至關重要。

2024年,行動處理器市場規模將達到74億美元,成為最大的收入來源。其成長主要得益於智慧型手機、穿戴式裝置和平板電腦需求的激增,以及人工智慧運算和5G網路整合等技術的進步。消費者對攜帶式設備性能的日益成長的期望,促使製造商設計出兼具能源效率和卓越運算能力的晶片。小型化、多任務處理和低功耗將是滿足消費者對連網設備日益成長的需求以及支援下一代行動技術創新的關鍵。

預計到2024年,美國2奈米及以下製程半導體市場規模將達22億美元。美國市場的成長主要得益於政府大力推動半導體製造、支援自動駕駛技術研發以及擴展高性能資料中心基礎設施等措施。人工智慧研究的拓展、雲端運算投資的成長以及數據密集型應用的日益普及,也進一步推動了市場擴張。該地區的製造商正著力提升製程可擴展性、加強研發合作以及提高晶片生產能效,以滿足工業和商業領域不斷成長的需求。

活躍於全球2奈米及以下製程半導體節點市場的知名企業包括英特爾公司、台積電、阿斯麥控股公司、三星電子有限公司、東京電子有限公司、Lam Research Corporation、KLA Corporation、應用材料公司、信越化學工業株式會社、東京櫻工業株式會社、富士膠卷電子公司、JSR Corporation、Rapidus Corporation, Eapidus Corporation。這些市場領導者正採取一系列策略來鞏固其競爭優勢。他們致力於擴大產能、加速奈米製造領域的研究,並引入創新的光刻技術以提高性能和效率。晶片製造商、材料供應商和設備供應商之間的策略聯盟與合作正在加強生態系統整合,並縮短開發週期。對人工智慧驅動的晶片設計和下一代製程節點的巨額投資,正助力企業實現更高的電晶體密度和每瓦性能。此外,各公司正在優先考慮永續製造、製程最佳化和先進封裝技術,以保持競爭力並滿足全球對超高效半導體日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 高效能運算需求

- 人工智慧和機器學習的進步

- 5G和邊緣運算的成長

- 消費性電子創新推動需求成長

- 政府投資和激勵措施

- 陷阱與挑戰

- 極高的製造複雜性

- 研發和資本成本飆升

- 市場機遇

- 量子計算的出現

- 汽車電氣化和自動駕駛汽車

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興商業模式

- 合規要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 對主要參與者進行競爭基準分析

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導人

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年主要發展動態

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型計劃

- 新興/新創企業競爭對手格局

第5章:市場估算與預測:依技術類型分類,2021-2034年

- 主要趨勢

- 基於FinFET的3nm工藝

- 標準3nm FinFET

- 增強型 3nm FinFET

- 高效能 3nm FinFET

- 高效能3nm FinFET

- 汽車等級3nm FinFET

- 3nm 環柵工藝

- 多橋通道場效電晶體

- 奈米片 GAA 3nm

- 增強型 GAA 變異體

- 英特爾埃格斯特朗級工藝

- 英特爾 3 FinFET

- 英特爾 3 增強型

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 行動處理器

- 智慧型手機應用處理器

- 平板電腦處理器

- 穿戴式裝置處理器

- 資料中心處理器

- 伺服器CPU

- 資料中心GPU

- 網路處理單元

- 人工智慧和機器學習加速器

- 訓練加速器

- 推理加速器

- 邊緣人工智慧處理器

- 高效能運算

- 科學計算處理器

- 超級電腦CPU

- 工作站處理器

- 汽車半導體

- ADAS處理器

- 自動駕駛晶片

- 資訊娛樂處理器

- 消費性電子產品

- 遊戲主機處理器

- 智慧電視晶片

- 物聯網設備處理器

第7章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 消費性電子產品

- 智慧型手機製造商

- 電腦和筆記型電腦製造商

- 遊戲設備製造商

- 穿戴式科技公司

- 資料中心和雲端運算

- 超大規模資料中心營運商

- 雲端服務供應商

- 企業資料中心

- 邊緣運算提供者

- 汽車產業

- 傳統汽車OEM廠商

- 電動汽車製造商

- 自動駕駛汽車公司

- 汽車一級供應商

- 航太與國防

- 國防承包商

- 航太製造商

- 衛星公司

- 軍事系統整合商

- 高效能運算

- 研究機構

- 政府實驗室

- 學術機構

- 超級運算中心

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- 全球關鍵參與者

- Taiwan Semiconductor Manufacturing Company

- Samsung Electronics Co., Ltd.

- Intel Corporation

- ASML Holding NV

- Applied Materials, Inc.

- 區域關鍵參與者

- 北美洲

- Lam Research Corporation

- KLA Corporation

- 歐洲

- IMEC

- Asia-Pacific

- Tokyo Electron Limited

- Shin-Etsu Chemical Co., Ltd.

- JSR Corporation

- Tokyo Ohka Kogyo Co., Ltd.

- FUJIFILM Electronic Materials

- 北美洲

- 顛覆者/小眾玩家

- Rapidus Corporation

- Tenstorrent Inc.

The Global 2nm and Beyond Semiconductor Node Market was valued at USD 19.1 Billion in 2024 and is estimated to grow at a CAGR of 13.6% to reach USD 91.5 Billion by 2034.

The market growth is driven by the rising demand for high-performance computing, expanding applications of artificial intelligence, the growth of 5G and edge computing, and increasing innovation in next-generation consumer electronics. Government-backed incentives and public investments are further accelerating market momentum. The semiconductor industry is undergoing a significant transformation fueled by the widespread integration of AI and machine learning, resulting in a heightened demand for ultra-efficient, high-performance logic chips manufactured using advanced 2nm and beyond nodes. As AI spending continues to rise sharply, this surge in innovation will reshape computing capabilities, creating new opportunities for performance-driven and energy-efficient chip technologies. Expanding 5G infrastructure and the growing adoption of edge computing are intensifying the need for smaller, faster, and more efficient chips, which is strengthening the adoption of 2nm technology across global industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.1 billion |

| Forecast Value | $91.5 billion |

| CAGR | 13.6% |

The Intel Angstrom-level process segment is expected to grow at a CAGR of 20.6% between 2025 and 2034, supported by increasing requirements for advanced chip architectures in AI, 5G, autonomous systems, and high-performance computing applications. The ongoing focus on enhancing chip energy efficiency, miniaturization, and scalability is vital to maintaining the pace of technological progress. Continued investments in next-generation process technologies are crucial for supporting the demand for faster, smarter, and more power-efficient semiconductor solutions in emerging digital ecosystems.

The mobile processor segment accounted for USD 7.4 Billion in 2024, making it the largest revenue-generating segment. Its growth is driven by surging demand for smartphones, wearables, and tablets, combined with technological advancements in AI-based computing and 5G network integration. The increasing performance expectations for portable devices are pushing manufacturers to design chips that balance energy efficiency with superior computing capabilities. Focus on miniaturization, multitasking, and low-power consumption will be key in addressing rising consumer demand for connected devices and supporting innovation in next-generation mobile technology.

United States 2nm and Beyond Semiconductor Node Market reached USD 2.2 Billion in 2024. Growth in the U.S. market is being driven by strong government initiatives to enhance semiconductor manufacturing, support autonomous technology development, and expand high-performance data center infrastructure. Expanding AI research, growing cloud computing investments, and the rising importance of data-intensive applications are further strengthening market expansion. Manufacturers in the region are emphasizing innovation in process scalability, R&D collaboration, and energy-efficient chip production to meet increasing demand across industrial and commercial sectors.

Prominent companies active in the Global 2nm and Beyond Semiconductor Node Market include Intel Corporation, Taiwan Semiconductor Manufacturing Company, ASML Holding N.V., Samsung Electronics Co., Ltd., Tokyo Electron Limited, Lam Research Corporation, KLA Corporation, Applied Materials, Inc., Shin-Etsu Chemical Co., Ltd., Tokyo Ohka Kogyo Co., Ltd., FUJIFILM Electronic Materials, JSR Corporation, Rapidus Corporation, IMEC, and Tenstorrent Inc. Leading players in the 2nm and Beyond Semiconductor Node Market are employing a range of strategies to strengthen their competitive positioning. Companies are focusing on expanding production capacity, accelerating research in nanofabrication, and introducing innovative lithography technologies to improve performance and efficiency. Strategic alliances and collaborations between chip manufacturers, materials providers, and equipment suppliers are enhancing ecosystem integration and shortening development cycles. Heavy investments in AI-driven chip design and next-generation process nodes are enabling companies to achieve higher transistor density and performance per watt. Furthermore, firms are prioritizing sustainable manufacturing, process optimization, and advanced packaging techniques to maintain competitiveness and meet rising global demand for ultra-efficient semiconductors.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Application trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 High-performance computing demand

- 3.3.1.2 Ai and machine learning advancements

- 3.3.1.3 5g and edge computing growth

- 3.3.1.4 Consumer electronics innovation driving demand

- 3.3.1.5 Government investments and incentives

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Extreme manufacturing complexity

- 3.3.2.2 Skyrocketing R&D and capital costs

- 3.3.3 Market Opportunities

- 3.3.3.1 Emergence of quantum computing

- 3.3.3.2 Automotive electrification and autonomous vehicles

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Sustainability measures

- 3.14 Consumer sentiment analysis

- 3.15 Patent and IP analysis

- 3.16 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Technology Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 FinFET-based 3nm

- 5.2.1 Standard FinFET 3nm

- 5.2.2 Enhanced FinFET 3nm

- 5.2.3 Performance FinFET 3nm

- 5.2.4 High-performance FinFET 3nm

- 5.2.5 Automotive FinFET 3nm

- 5.3 Gate-all-around 3nm

- 5.3.1 Multi-bridge channel FET

- 5.3.2 Nanosheet GAA 3nm

- 5.3.3 Enhanced GAA variants

- 5.4 Intel Angstrom-level Process

- 5.4.1 Intel 3 FinFET

- 5.4.2 Intel 3 enhanced variants

Chapter 6 Market estimates and forecast, by Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Mobile processors

- 6.2.1 Smartphone application processors

- 6.2.2 Tablet processors

- 6.2.3 Wearable device processors

- 6.3 Data Center processors

- 6.3.1 Server CPUs

- 6.3.2 Data center GPUs

- 6.3.3 Network processing units

- 6.4 AI & Machine learning accelerators

- 6.4.1 Training accelerators

- 6.4.2 Inference accelerators

- 6.4.3 Edge AI processors

- 6.5 High-performance computing

- 6.5.1 Scientific computing processors

- 6.5.2 Supercomputing CPUs

- 6.5.3 Workstation processors

- 6.6 Automotive semiconductors

- 6.6.1 Adas processors

- 6.6.2 Autonomous driving chips

- 6.6.3 Infotainment processors

- 6.7 Consumer electronics

- 6.7.1 Gaming console processors

- 6.7.2 Smart tv chips

- 6.7.3 IoT device processors

Chapter 7 Market estimates and forecast, by End Use industry, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.2.1 Smartphone manufacturers

- 7.2.2 Computer & laptop manufacturers

- 7.2.3 Gaming device manufacturers

- 7.2.4 Wearable technology companies

- 7.3 Data Centers & Cloud Computing

- 7.3.1 Hyperscale data center operators

- 7.3.2 Cloud service providers

- 7.3.3 Enterprise data centers

- 7.3.4 Edge computing providers

- 7.4 Automotive industry

- 7.4.1 Traditional automotive oems

- 7.4.2 Electric Vehicle manufacturers

- 7.4.3 Autonomous vehicle companies

- 7.4.4 Automotive tier 1 suppliers

- 7.5 Aerospace & defense

- 7.5.1 Defense contractors

- 7.5.2 Aerospace manufacturers

- 7.5.3 Satellite companies

- 7.5.4 Military system integrators

- 7.6 High-performance computing

- 7.6.1 Research institutions

- 7.6.2 Government laboratories

- 7.6.3 Academic institutions

- 7.6.4 Supercomputing centers

Chapter 8 Market estimates and forecast, by region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company profiles

- 9.1 Global Key Players

- 9.1.1 Taiwan Semiconductor Manufacturing Company

- 9.1.2 Samsung Electronics Co., Ltd.

- 9.1.3 Intel Corporation

- 9.1.4 ASML Holding N.V.

- 9.1.5 Applied Materials, Inc.

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Lam Research Corporation

- 9.2.1.2 KLA Corporation

- 9.2.2 Europe

- 9.2.2.1 IMEC

- 9.2.3 Asia-Pacific

- 9.2.3.1 Tokyo Electron Limited

- 9.2.3.2 Shin-Etsu Chemical Co., Ltd.

- 9.2.3.3 JSR Corporation

- 9.2.3.4 Tokyo Ohka Kogyo Co., Ltd.

- 9.2.3.5 FUJIFILM Electronic Materials

- 9.2.1 North America

- 9.3 Disruptors / Niche Players

- 9.3.1 Rapidus Corporation

- 9.3.2 Tenstorrent Inc.