|

市場調查報告書

商品編碼

1871172

精準發酵生物反應器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Precision Fermentation Bioreactors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

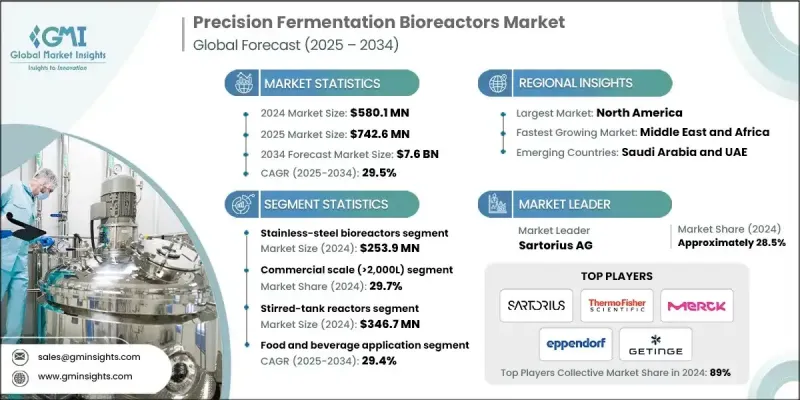

2024 年全球精準發酵生物反應器市值為 5.801 億美元,預計到 2034 年將以 29.5% 的複合年成長率成長至 76 億美元。

市場擴張的驅動力在於消費者對永續且不含動物成分的蛋白質和酵素生產的日益成長的需求。隨著消費者擴大選擇植物性和符合倫理的替代品,精準發酵已成為一種永續且可擴展的解決方案,用於生產高價值成分,例如乳製品替代品和分離蛋白,而無需依賴動物。對環境責任和符合倫理的採購方式的日益重視,正在加速食品和生物技術領域對精準發酵的採用。此外,該技術能夠提供穩定的產品品質並減少傳統蛋白質生產的碳足跡,這鞏固了其作為未來食品生態系統關鍵推動因素的地位。微生物菌株工程和即時製程監控的不斷進步也提高了發酵系統的精確度、效率和產量,為產業的快速發展創造了有利條件。此外,技術整合、自動化和資料分析正在幫助企業有效地從試點階段擴展到商業化營運,從而支援發酵衍生成分的大規模生產。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.801億美元 |

| 預測值 | 76億美元 |

| 複合年成長率 | 29.5% |

2024年,容量大於2000公升的商業規模生物反應器市場規模達2.356億美元,預計2025年至2034年間將以29.7%的複合年成長率成長。大容量生物反應器已成為工業規模精準發酵的關鍵設備,有助於實現穩定、高品質且經濟高效的生產流程。商業規模部署的穩定成長表明,該產業正從研發和原型階段轉型為大規模、市場化生產。向工業規模化發展的趨勢反映了生產商對實現經濟可行性和合規性的信心日益增強,從而推動了該技術在各行業的廣泛應用。

食品飲料產業仍然是該技術的主要應用領域之一,這主要得益於市場對透過精準發酵生產的無動物性蛋白質、酵素和調味劑的需求不斷成長。消費者對永續發展意識的提高,以及對替代蛋白的需求轉變,都促進了發酵技術的廣泛應用。隨著生產商認知到該方法在生產更清潔、更永續的食品方面的長期潛力,中試規模的實驗正在迅速發展成為商業化生產線。

2024年,美國精準發酵生物反應器市場佔據了顯著佔有率,這得益於其先進的研發能力、強大的產業合作以及良好的創新生態系統。美國的生物技術和食品科技產業正積極推進實驗室培養蛋白、乳製品替代品和酵素的商業化,大學和私人企業攜手合作,不斷改進發酵技術。自動化和數位化製程控制的融合正在提升發酵系統的可靠性、生產效率和穩定性。

全球精準發酵生物反應器市場的主要參與者包括默克集團(MilliporeSigma)、賽默飛世爾科技、賽多利斯、Getinge AB 和 Eppendorf AG。精準發酵生物反應器市場中各公司採取的關鍵策略著重於創新、可擴展性和策略合作。主要製造商正大力投資研發,以提升製程控制、能源效率和發酵產量。與食品科技和生物科技公司的策略合作有助於拓展應用領域並加速市場商業化。各公司也強調模組化生物反應器設計,以實現從實驗室到工業生產的靈活擴展。自動化、人工智慧驅動的監控和數位孿生技術的整合正在提高系統精度並降低營運成本。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 供應鏈的複雜性

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 免洗生物反應器

- 不銹鋼生物反應器

- 玻璃生物反應器

- 混合生物反應器

- 攪拌槽式生物反應器

- 其他

第6章:市場規模估算與預測(2021-2034年)

- 主要趨勢

- 實驗室規模(<50公升)

- 中試規模(50公升 - 2,000公升)

- 商業規模(>2,000公升)

- 小型商用(2,000公升 - 10,000公升)

- 大型商用(>10,000公升)

第7章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 攪拌釜式反應器

- 波浪/搖擺式生物反應器

- 鼓泡柱反應器

- 其他技術

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 餐飲

- 替代蛋白

- 乳蛋白

- 肉類蛋白質

- 雞蛋蛋白

- 食品原料

- 酵素

- 維生素

- 香料和防腐劑

- 功能性食品

- 益生菌和益生元

- 營養補充品

- 替代蛋白

- 製藥

- 治療性蛋白質

- 疫苗和生物製劑

- 藥用酶

- 工業和化學

- 工業酵素

- 特種化學品

- 生物燃料和能源

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Sartorius AG

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Eppendorf AG

- Getinge AB

- Pall Corporation (Danaher)

- ABEC Inc.

- Applikon Biotechnology

- Solaris Biotechnology

- Pierre Guerin Technologies

- Perfect Day Inc.

- Impossible Foods Inc.

- TurtleTree Labs

- The EVERY Company

- Motif FoodWorks

- Geltor Inc.

- Clara Foods (The EVERY Company)

- Novonesis (formerly Novozymes)

- Ginkgo Bioworks

- Zymergen (Ginkgo Bioworks)

- Synthetic Biologics Inc.

- Amyris Inc.

- Formo (formerly LegenDairy Foods)

- Change Foods

- New Culture Inc.

- Remilk Ltd.

- Imagindairy Ltd.

- Shiru Inc.

- Tetra Pak

- Culture Biosciences

The Global Precision Fermentation Bioreactors Market was valued at USD 580.1 million in 2024 and is estimated to grow at a CAGR of 29.5% to reach USD 7.6 Billion by 2034.

Market expansion is propelled by the increasing preference for sustainable and animal-free production of proteins and enzymes. As consumers increasingly choose plant-based and ethical alternatives, precision fermentation has emerged as a sustainable and scalable solution for producing high-value ingredients such as dairy analogs and protein isolates without relying on animals. The growing emphasis on environmental responsibility and ethical sourcing is accelerating adoption in both food and biotechnology sectors. Furthermore, the technology's ability to deliver consistent product quality and reduce the carbon footprint of traditional protein production strengthens its position as a key enabler of the future food ecosystem. Continuous progress in microbial strain engineering and real-time process monitoring is also improving the precision, efficiency, and yield of fermentation systems, creating favorable conditions for rapid industry growth. Additionally, technological integration, automation, and data analytics are helping companies scale from pilot to commercial operations efficiently, supporting the shift toward mass production of fermentation-derived ingredients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $580.1 million |

| Forecast Value | $7.6 Billion |

| CAGR | 29.5% |

The commercial-scale segment > 2,000L was valued at USD 235.6 million in 2024 and is expected to register a CAGR of 29.7% during 2025-2034. Large-volume bioreactors have become essential for industrial-scale precision fermentation, facilitating consistent, high-quality, and cost-effective manufacturing processes. The steady rise in commercial-scale deployment demonstrates the industry's transition from research and prototype phases toward large-scale, market-ready production. The move toward industrial scalability reflects the growing confidence of producers in achieving economic feasibility and regulatory compliance, supporting widespread adoption across various industries.

The food & beverage sector remains one of the leading application areas, driven by increasing demand for animal-free proteins, enzymes, and flavoring agents produced through precision fermentation. Rising consumer awareness regarding sustainability, combined with a shift toward alternative proteins, has encouraged broader adoption of fermentation-based technologies. Pilot-scale experiments are rapidly evolving into commercial production lines as producers recognize the long-term potential of this method for creating cleaner, more sustainable food products.

United States Precision Fermentation Bioreactors Market held a significant share in 2024, supported by advanced R&D capabilities, strong industrial collaboration, and a favorable innovation ecosystem. The country's biotechnology and food-tech industries are actively advancing the commercialization of lab-cultured proteins, dairy substitutes, and enzymes, with universities and private firms collaborating to refine fermentation technologies. The integration of automation and digital process control is improving the reliability, productivity, and consistency of fermentation systems.

Leading players operating in the Global Precision Fermentation Bioreactors Market include Merck KGaA (MilliporeSigma), Thermo Fisher Scientific, Sartorius AG, Getinge AB, and Eppendorf AG. Key strategies adopted by companies in the Precision Fermentation Bioreactors Market focus on innovation, scalability, and strategic collaboration. Major manufacturers are investing heavily in R&D to enhance process control, energy efficiency, and fermentation yield. Strategic partnerships with food-tech and biotech firms are helping expand application areas and accelerate market commercialization. Companies are also emphasizing modular bioreactor designs that allow flexible scaling from laboratory to industrial production. Integration of automation, AI-driven monitoring, and digital twin technologies is improving system precision and reducing operational costs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Scale

- 2.2.4 Technology

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021- 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Single-use bioreactors

- 5.3 Stainless steel bioreactors

- 5.4 Glass bioreactors

- 5.5 Hybrid bioreactors

- 5.6 Stirred-tank bioreactors

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Scale, 2021- 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Laboratory scale (<50L)

- 6.3 Pilot scale (50L - 2,000L)

- 6.4 Commercial scale (>2,000L)

- 6.4.1 Small commercial (2,000L - 10,000L)

- 6.4.2 Large commercial (>10,000L)

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million, , Units)

- 7.1 Key trends

- 7.2 Stirred-tank reactors

- 7.3 Wave/rocking bioreactors

- 7.4 Bubble column reactors

- 7.5 Other technologies

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million, , Units)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.2.1 Alternative proteins

- 8.2.1.1 Dairy proteins

- 8.2.1.2 Meat proteins

- 8.2.1.3 Egg proteins

- 8.2.2 Food ingredients

- 8.2.2.1 Enzymes

- 8.2.2.2 Vitamins

- 8.2.2.3 Flavors and preservatives

- 8.2.3 Functional foods

- 8.2.3.1 Probiotics and prebiotics

- 8.2.3.2 Nutritional supplements

- 8.2.1 Alternative proteins

- 8.3 Pharmaceutical

- 8.3.1 Therapeutic proteins

- 8.3.2 Vaccines and biologics

- 8.3.3 Pharmaceutical enzymes

- 8.4 Industrial and chemical

- 8.4.1 Industrial enzymes

- 8.4.2 Specialty chemicals

- 8.4.3 Biofuels and energy

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Sartorius AG

- 10.2 Thermo Fisher Scientific Inc.

- 10.3 Merck KGaA

- 10.4 Eppendorf AG

- 10.5 Getinge AB

- 10.6 Pall Corporation (Danaher)

- 10.7 ABEC Inc.

- 10.8 Applikon Biotechnology

- 10.9 Solaris Biotechnology

- 10.10 Pierre Guerin Technologies

- 10.11 Perfect Day Inc.

- 10.12 Impossible Foods Inc.

- 10.13 TurtleTree Labs

- 10.14 The EVERY Company

- 10.15 Motif FoodWorks

- 10.16 Geltor Inc.

- 10.17 Clara Foods (The EVERY Company)

- 10.18 Novonesis (formerly Novozymes)

- 10.19 Ginkgo Bioworks

- 10.20 Zymergen (Ginkgo Bioworks)

- 10.21 Synthetic Biologics Inc.

- 10.22 Amyris Inc.

- 10.23 Formo (formerly LegenDairy Foods)

- 10.24 Change Foods

- 10.25 New Culture Inc.

- 10.26 Remilk Ltd.

- 10.27 Imagindairy Ltd.

- 10.28 Shiru Inc.

- 10.29 Tetra Pak

- 10.30 Culture Biosciences

2025年人工智慧(AI)控制灌註生物反應器市場報告2025年全球一次性液流電池生物反應器市場報告

2025年人工智慧(AI)控制灌註生物反應器市場報告2025年全球一次性液流電池生物反應器市場報告 灌注式生物反應器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

灌注式生物反應器:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 發酵槽和生物反應器市場分析及預測(至2034年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、組件、階段2025年全球中空纖維生物反應器市場報告2025年全球可攜式生物製程生物反應器市場報告2025年全球桌上型生物反應器市場報告2025年全球細胞處理設備市場報告

發酵槽和生物反應器市場分析及預測(至2034年):類型、產品、服務、技術、應用、材料類型、製程、最終用戶、組件、階段2025年全球中空纖維生物反應器市場報告2025年全球可攜式生物製程生物反應器市場報告2025年全球桌上型生物反應器市場報告2025年全球細胞處理設備市場報告 全球一次性生物反應器市場:市場規模、佔有率和趨勢分析(按產品、類型、細胞類型、分子類型、應用、最終用途、使用階段和地區分類),細分市場預測(2025-2033 年)2025年氣升生物反應器全球市場報告

全球一次性生物反應器市場:市場規模、佔有率和趨勢分析(按產品、類型、細胞類型、分子類型、應用、最終用途、使用階段和地區分類),細分市場預測(2025-2033 年)2025年氣升生物反應器全球市場報告