|

市場調查報告書

商品編碼

1871169

3D列印醫療器材原型市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)3D Printed Medical Device Prototyping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

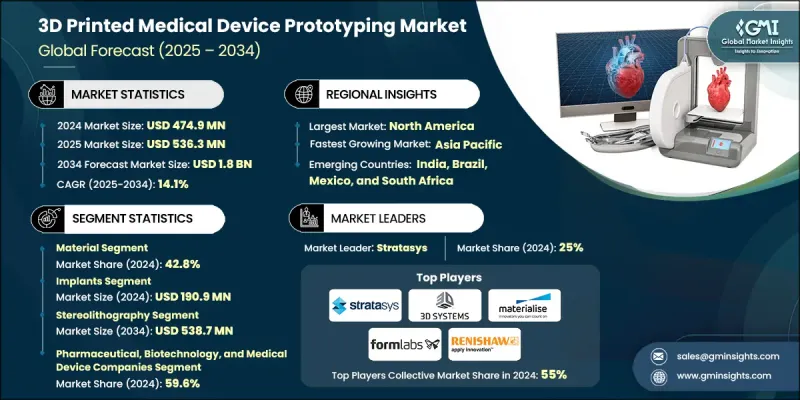

2024 年全球 3D 列印醫療器材原型市值為 4.749 億美元,預計到 2034 年將以 14.1% 的複合年成長率成長至 18 億美元。

持續成長歸功於骨科和牙科疾病數量的增加、積層製造技術的不斷進步、醫療創新投資的不斷成長以及3D列印在醫療應用中的日益普及。 3D列印醫療器材原型製作是指利用積層製造技術開發醫療器材的初步模型,以便在全面生產前測試設計的精確度、適配性和功能性。這個過程能夠加速產品開發,支持針對個別患者的客製化治療,並確保高效的設計驗證。它在術前規劃中尤其重要,臨床醫生可以利用該技術創建患者專屬的原型,從而提高植入物的精準度,縮短手術時間,並改善術後恢復效果。透過實現快速迭代和即時測試,3D列印確保醫療器材符合嚴格的性能和生物相容性標準,從而加快產品上市速度,並推動醫療領域以精準為導向的創新。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4.749億美元 |

| 預測值 | 18億美元 |

| 複合年成長率 | 14.1% |

2024年,材料細分市場佔據42.8%的市場佔有率,預計在整個預測期內將保持主導地位。材料是原型可靠性、功能性和安全性的基礎。製造商能夠從先進的金屬、塑膠和生物材料中進行選擇,從而滿足醫療應用中嚴格的生物相容性、耐久性和滅菌標準。由於積層製造技術的突破和對個人化醫療保健需求的不斷成長,該細分市場持續擴張。熱塑性塑膠和光敏聚合物的新興發展正在提升材料的柔韌性、精度和滅菌性能,進一步支持其在醫療原型製作中的廣泛應用。

預計到2034年,立體光刻技術市場規模將達5.387億美元。該技術採用雷射工藝,逐層固化液態樹脂,從而製造出表面品質和尺寸精度極高的原型。立體光刻技術能夠製作複雜且高度精確的模型,使其成為製造對精度和光滑度要求極高的複雜醫療零件的理想選擇。此外,立體光刻技術與生物相容性材料的兼容性也進一步鞏固了其在醫療保健原型製作領域的應用前景。

2024年,美國3D列印醫療器材原型市場規模預計將達到1.772億美元。推動美國市場成長的主要因素是骨科和牙科疾病發病率的上升,這些疾病影響了相當一部分成年人口。隨著醫療機構和器材製造商將3D列印技術融入產品開發流程,美國仍是創新和生產的關鍵中心。先進的製造能力、完善的監管體係以及不斷成長的醫療研發投入,鞏固了美國在醫療器材原型領域的領先地位。

在全球3D列印醫療器材原型市場中,Renishaw、3D Systems、Proto Labs、Stratasys、Materialise、Envision TEC、Paragon Medical、SolidWorks、Empire Group USA、Formlabs、Organovo Holdings、Arcam、Inventex Medical、COSA和EOS等公司佔據主導地位。這些領導企業正實施多項策略以鞏固其市場地位。他們大力投資研發,以提升材料性能和列印精度。與醫療機構和研究機構的策略合作有助於擴大臨床驗證範圍並加速產品應用。許多公司正致力於擴大其全球產能和分銷網路,以滿足不斷成長的市場需求。此外,他們還透過併購和合作來整合先進技術並拓展產品組合。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 骨科和牙科疾病高發生率

- 3D列印技術的持續進步

- 對醫療保健創新和數位化製造的投資不斷增加

- 3D列印醫療器材的應用日益廣泛

- 產業陷阱與挑戰

- 嚴格的監理合規要求

- 原料成本高

- 市場機遇

- 將3D列印與醫學影像和CAD軟體整合

- 開發可生物吸收的、病人客製的植入物

- 成長促進因素

- 成長潛力分析

- 監管環境

- 技術進步

- 當前技術趨勢

- 新興技術

- 供應鏈分析

- 報銷方案

- 2024年定價分析

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 裝置

- 3D印表機

- 3D生物列印機

- 軟體

- 材料

- 塑膠

- 光敏聚合物

- 熱塑性塑膠

- 金屬和合金

- 鈦

- 不銹鋼

- 鈷鉻合金

- 生物材料

- 陶瓷製品

- 其他材料

- 塑膠

- 服務

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 義肢

- 植入物

- 顱頜面植入物

- 植牙

- 骨科植入物

- 手術導板

- 組織工程產品

- 穿戴式醫療設備

- 其他應用

第7章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 立體光刻技術

- 熔融沈積成型

- 電子束熔化

- 雷射燒結

- 黏結劑噴射成型

- 數位光處理

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和醫療機構

- 製藥、生技和醫療器材公司

- 其他最終用途

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- 3D Systems

- Arcam

- COSA

- Empire Group USA

- Envision TEC

- EOS

- Formlabs

- Inventex Medical

- Materialise

- Organovo Holdings

- Paragon Medical

- Proto Labs

- Renishaw

- SolidWorks

- Stratasys

The Global 3D Printed Medical Device Prototyping Market was valued at USD 474.9 million in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 1.8 Billion by 2034.

The consistent growth is attributed to the increasing number of orthopedic and dental conditions, ongoing advancements in additive manufacturing, rising investments in healthcare innovation, and the expanding use of 3D printing in medical applications. 3D printed medical device prototyping involves developing preliminary models of medical instruments using additive manufacturing to test design accuracy, fit, and functionality prior to full-scale production. This process accelerates product development, supports customization for individual patients, and ensures efficient design validation. It is especially beneficial in pre-surgical planning, where clinicians can create patient-specific prototypes that improve implant accuracy, shorten surgical durations, and enhance recovery outcomes. By enabling rapid iteration and real-time testing, 3D printing ensures medical devices meet rigorous performance and biocompatibility standards, allowing faster market readiness and precision-driven innovation in healthcare.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $474.9 Million |

| Forecast Value | $1.8 Billion |

| CAGR | 14.1% |

The material segment held a 42.8% share in 2024 and is projected to remain dominant throughout the forecast period. Materials form the foundation of prototype reliability, functionality, and safety. The ability to select from advanced metals, plastics, and biomaterials enables manufacturers to meet strict biocompatibility, durability, and sterilization standards in medical applications. This segment continues to expand due to breakthroughs in additive manufacturing and the growing demand for personalized healthcare. Emerging developments in thermoplastics and photopolymers are enhancing material flexibility, precision, and sterilization performance, further supporting their extensive use in medical prototyping.

The stereolithography segment is expected to reach USD 538.7 million by 2034. This technique utilizes a laser-based process that solidifies liquid resin in successive layers, producing prototypes with exceptional surface quality and dimensional precision. The technology's ability to deliver intricate and highly accurate models makes it an ideal choice for creating complex medical components where precision and smoothness are crucial. Furthermore, the compatibility of stereolithography with biocompatible materials reinforces its continued adoption in healthcare prototyping applications.

United States 3D Printed Medical Device Prototyping Market was valued at USD 177.2 million in 2024. The country's growth is fueled by the rising occurrence of orthopedic and dental conditions affecting a significant portion of the adult population. With healthcare organizations and device manufacturers integrating 3D printing into product development workflows, the U.S. remains a key hub for innovation and production. The convergence of advanced manufacturing capabilities, strong regulatory infrastructure, and increasing healthcare R&D investment solidifies the nation's leadership in medical device prototyping.

Prominent companies shaping the Global 3D Printed Medical Device Prototyping Market landscape include Renishaw, 3D Systems, Proto Labs, Stratasys, Materialise, Envision TEC, Paragon Medical, SolidWorks, Empire Group USA, Formlabs, Organovo Holdings, Arcam, Inventex Medical, COSA, and EOS. Leading companies in the 3D Printed Medical Device Prototyping Market are implementing multiple strategies to strengthen their market position. They are investing heavily in research and development to enhance material performance and printing precision. Strategic collaborations with healthcare institutions and research organizations are helping expand clinical validation and accelerate adoption. Many firms are focusing on expanding their global production capacities and distribution networks to meet rising demand. Mergers, acquisitions, and partnerships are being leveraged to integrate advanced technologies and broaden product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trend

- 2.2.4 Technology trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High prevalence of orthopedic and dental disorders

- 3.2.1.2 Continuous technological advancement in 3D printing technologies

- 3.2.1.3 Rising investment in healthcare innovation and digital manufacturing

- 3.2.1.4 Growing application of 3D printed medical devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory compliance requirements

- 3.2.2.2 High cost of raw materials

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of 3D printing with medical imaging and CAD software

- 3.2.3.2 Development of bioresorbable and patient-specific implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Equipment

- 5.2.1 3D printer

- 5.2.2 3D bioprinter

- 5.3 Software

- 5.4 Materials

- 5.4.1 Plastic

- 5.4.1.1 Photopolymers

- 5.4.1.2 Thermoplastics

- 5.4.2 Metals and alloys

- 5.4.2.1 Titanium

- 5.4.2.2 Stainless steel

- 5.4.2.3 Cobalt-chromium

- 5.4.3 Biomaterials

- 5.4.4 Ceramic

- 5.4.5 Other materials

- 5.4.1 Plastic

- 5.5 Services

Chapter 6 Market Estimates and Forecast, By Applications, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Prosthetics

- 6.3 Implants

- 6.3.1 Craniomaxillofacial implants

- 6.3.2 Dental implants

- 6.3.3 Orthopedic implants

- 6.4 Surgical guides

- 6.5 Tissue engineered products

- 6.6 Wearable medical devices

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stereolithography

- 7.3 Fused deposition modeling

- 7.4 Electron beam melting

- 7.5 Laser sintering

- 7.6 Binder jetting

- 7.7 Digital light processing

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and healthcare institutions

- 8.3 Pharmaceutical, biotechnology, and medical device companies

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3D Systems

- 10.2 Arcam

- 10.3 COSA

- 10.4 Empire Group USA

- 10.5 Envision TEC

- 10.6 EOS

- 10.7 Formlabs

- 10.8 Inventex Medical

- 10.9 Materialise

- 10.10 Organovo Holdings

- 10.11 Paragon Medical

- 10.12 Proto Labs

- 10.13 Renishaw

- 10.14 SolidWorks

- 10.15 Stratasys