|

市場調查報告書

商品編碼

1871149

智慧電網網路安全市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Smart Grid Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

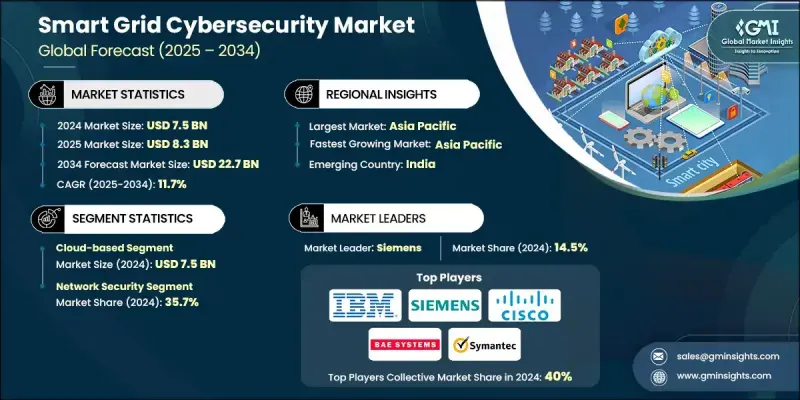

2024 年全球智慧電網網路安全市場價值為 75 億美元,預計到 2034 年將以 11.7% 的複合年成長率成長至 227 億美元。

電力系統數位轉型加速,擴大了攻擊面,從智慧電錶到分散式能源(DER)和電動車充電樁,網路韌性成為電網設計和採購的關鍵考量。電網現代化和再生能源併網需要複雜的數位控制系統,促使電力公司採用安全的遙測、邊緣運算和協調平台。隨著新興市場規模擴大和分散式資產激增,正式的網路安全標準變得至關重要。分散式能源、太陽能裝置、儲能解決方案和電動車充電樁的興起,增加了聚合平台和逆變器型資源的脆弱性。監管機構和電力公司正在透過統一的框架、人工智慧驅動的異常檢測和自動化事件回應來應對這些挑戰,以確保預測分析和即時威脅緩解,但自動化也帶來了諸如對抗性人工智慧攻擊等風險。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 75億美元 |

| 預測值 | 227億美元 |

| 複合年成長率 | 11.7% |

受電網數位化程度提高和針對營運技術的網路威脅日益加劇的推動,基於雲端的解決方案市場在2024年創造了75億美元的收入。公用事業公司和監管機構正優先考慮建立強大的安全系統,以保護分散式能源資產和進階計量基礎設施,從而推動了對可擴展雲端部署的需求。

網路安全領域預計在2024年將佔據35.7%的市場佔有率,這反映出保護互聯通訊通道免受日益複雜的攻擊的必要性。隨著先進計量基礎設施和分散式能源(DER)的普及,公用事業公司需要強大的邊界和內部防禦體系來維持營運彈性並確保合規性。

2024年,美國智慧電網網路安全市場規模預計將達到18億美元,佔全球市場佔有率的81.5%。該市場的成長主要得益於聯邦政府旨在提升關鍵基礎設施網路韌性的各項舉措,以及分散式能源(DER)和高級計量系統的日益普及。公用事業公司正大力投資符合美國能源部和北美電力可靠性公司(NERC)標準的框架,以確保營運技術網路的安全。

推動全球智慧電網網路安全市場發展的關鍵企業包括思科系統、趨勢科技、洛克希德·馬丁、惠普、英國航空航太系統公司、IBM、施耐德電氣、ABB、AlienVault、Fortinet、CyberArk、Itron、Check Point軟體技術公司、霍尼韋爾、賽門鐵克、GEnovan、Blacktoatch、PIO、Enter這些企業透過開發針對營運技術和分散式能源(DER)保護量身定做的整合式網路安全平台、投資人工智慧驅動的威脅偵測和自動化事件回應解決方案,以及確保符合不斷變化的監管標準,來鞏固其在智慧電網網路安全市場的地位。他們專注於與公用事業公司和技術供應商建立策略合作夥伴關係,擴展基於雲端的產品以提高可擴展性,並不斷創新,開發下一代加密、異常檢測和漏洞評估工具。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 監管環境

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

- 新興機會與趨勢

- 智慧電網網路安全投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 戰略儀錶板

- 競爭性標竿分析

- 創新與技術格局

第5章:市場規模及預測:依解決方案分類,2021-2034年

- 主要趨勢

- 身分和存取管理 (IAM)

- 防火牆及網路安全

- 入侵偵測/防禦系統(IDS/IPS)

- 加密解決方案

- 安全資訊和事件管理 (SIEM)

- 端點保護

- 其他

第6章:市場規模及預測:依服務類型分類,2021-2034年

- 主要趨勢

- 諮詢

- 整合與部署

- 支援和維護

第7章:市場規模及預測:依部署模式分類,2021-2034年

- 主要趨勢

- 現場

- 雲

第8章:市場規模及預測:以子系統分類,2021-2034年

- 主要趨勢

- SCADA/ICS

- AMI(進階計量基礎設施)

- 需量反應系統

- 家庭能源管理

- 其他

第9章:市場規模及預測:依證券類型分類,2021-2034年

- 主要趨勢

- 端點安全

- 網路安全

- 應用程式安全

- 資料庫安全

第10章:市場規模及預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 澳洲

- 日本

- 韓國

- 印度

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 智利

第11章:公司簡介

- ABB

- AlertEnterprise

- AlienVault

- BAE Systems

- Black & Veatch

- Check Point Software Technologies

- Cisco Systems

- CyberArk

- Entergy

- Fortinet

- GE Vernova

- Honeywell

- Hewlett Packard

- IBM

- IOActive

- Itron

- Kaspersky Lab

- Lockheed Martin

- McAfee

- Palo Alto Networks

- Schneider Electric

- Siemens

- Symantec

- Trend Micro

The Global Smart Grid Cybersecurity Market was valued at USD 7.5 Billion in 2024 and is estimated to grow at a CAGR of 11.7% to reach USD 22.7 Billion by 2034.

The accelerated digital transformation of power systems has broadened the attack surface, ranging from smart meters to distributed energy resources (DERs) and electric vehicle chargers, making cyber resilience a critical consideration in grid design and procurement. Grid modernization and the integration of renewable energy necessitate sophisticated digital control systems, prompting utilities to adopt secure telemetry, edge computing, and coordination platforms. As emerging markets scale and distributed assets proliferate, formal cybersecurity standards are becoming essential. The rise of DERs, solar installations, storage solutions, and EV chargers has increased vulnerability across aggregation platforms and inverter-based resources. Regulators and utilities are responding with harmonized frameworks, AI-driven anomaly detection, and automated incident response to ensure predictive analytics and real-time threat mitigation, though automation also introduces risks such as adversarial AI attacks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $22.7 Billion |

| CAGR | 11.7% |

The cloud-based solutions segment generated USD 7.5 Billion in 2024, fueled by heightened grid digitalization and escalating cyber threats targeting operational technology. Utilities and regulators are prioritizing robust security systems to protect distributed energy assets and advanced metering infrastructures, driving demand for scalable cloud deployments.

The network security segment held a 35.7% share in 2024, reflecting the need to protect interconnected communication channels against increasingly sophisticated attacks. With the adoption of advanced metering infrastructure and DERs, utilities require strong perimeter and internal defenses to maintain operational resilience and regulatory compliance.

U.S Smart Grid Cybersecurity Market generated USD 1.8 Billion in 2024, accounting for 81.5% share. Growth is largely supported by federal initiatives focused on enhancing cyber resilience in critical infrastructure, alongside rising adoption of DERs and advanced metering systems. Utilities are investing heavily in frameworks aligned with Department of Energy and NERC standards to secure operational technology networks.

Key players driving the Global Smart Grid Cybersecurity Market include Cisco Systems, Trend Micro, Lockheed Martin, Hewlett Packard, BAE Systems, IBM, Schneider Electric, ABB, AlienVault, Fortinet, CyberArk, Itron, Check Point Software Technologies, Honeywell, Symantec, GE Vernova, Black & Veatch, Palo Alto Networks, IOActive, Entergy, Kaspersky Lab, and Siemens. Companies in the Smart Grid Cybersecurity Market strengthen their presence by developing integrated cybersecurity platforms tailored for operational technology and DER protection, investing in AI-driven threat detection and automated incident response solutions, and ensuring compliance with evolving regulatory standards. They focus on strategic partnerships with utilities and technology providers, expand cloud-based offerings for scalability, and continuously innovate with next-generation encryption, anomaly detection, and vulnerability assessment tools.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Solution trends

- 2.1.3 Service trends

- 2.1.4 Deployment mode trends

- 2.1.5 Subsystem trends

- 2.1.6 Security type trends

- 2.1.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.7 Emerging opportunities & trends

- 3.8 Investment analysis & future outlook for the smart grid cybersecurity

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Solution, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Identity and Access Management (IAM)

- 5.3 Firewalls & network security

- 5.4 Intrusion Detection/Prevention Systems (IDS/IPS)

- 5.5 Encryption solutions

- 5.6 Security Information and Event Management (SIEM)

- 5.7 Endpoint protection

- 5.8 Others

Chapter 6 Market Size and Forecast, By Service, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Consulting

- 6.3 Integration & deployment

- 6.4 Support and maintenance

Chapter 7 Market Size and Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud

Chapter 8 Market Size and Forecast, By Subsystem, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 SCADA/ICS

- 8.3 AMI (Advanced Metering Infrastructure)

- 8.4 Demand response systems

- 8.5 Home energy management

- 8.6 Others

Chapter 9 Market Size and Forecast, By Security Type, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 Endpoint security

- 9.3 Network security

- 9.4 Application security

- 9.5 Database security

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Germany

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 India

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Chile

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 AlertEnterprise

- 11.3 AlienVault

- 11.4 BAE Systems

- 11.5 Black & Veatch

- 11.6 Check Point Software Technologies

- 11.7 Cisco Systems

- 11.8 CyberArk

- 11.9 Entergy

- 11.10 Fortinet

- 11.11 GE Vernova

- 11.12 Honeywell

- 11.13 Hewlett Packard

- 11.14 IBM

- 11.15 IOActive

- 11.16 Itron

- 11.17 Kaspersky Lab

- 11.18 Lockheed Martin

- 11.19 McAfee

- 11.20 Palo Alto Networks

- 11.21 Schneider Electric

- 11.22 Siemens

- 11.23 Symantec

- 11.24 Trend Micro