|

市場調查報告書

商品編碼

1871148

汽車儲存半導體市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Automotive Memory Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

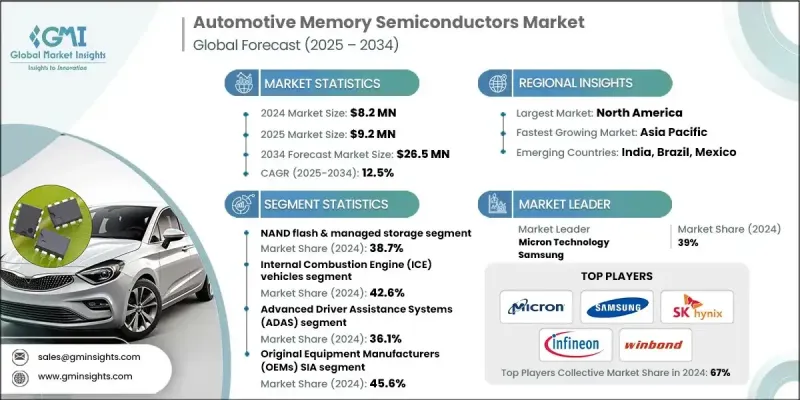

2024 年全球汽車儲存半導體市場價值為 820 萬美元,預計到 2034 年將以 12.5% 的複合年成長率成長至 2,650 萬美元。

高級駕駛輔助系統 (ADAS) 和自動駕駛技術的日益普及推動了對高性能汽車儲存半導體的需求。這些系統需要對來自感測器、攝影機、LiDAR和雷達單元的大量資料進行瞬時處理,因此對快速、可靠的儲存解決方案提出了迫切需求。 DRAM 和 NAND 快閃記憶體對於在複雜的運算平台中實現快速儲存、傳輸和分析至關重要。隨著車輛自動化程度的不斷提高,容量更大、延遲更低、耐久性更強的記憶體變得日益重要。向電動和混合動力汽車 (EV 和 HEV) 的轉型進一步推動了這一成長,因為複雜的電子控制單元 (ECU) 和電池管理系統需要先進的記憶體來監控能源使用、性能和安全性。 NOR 快閃記憶體、NAND 和 DRAM 等儲存組件支援感測器、動力系統和控制模組之間的即時通訊,從而最佳化效率和穩定性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 820萬美元 |

| 預測值 | 2650萬美元 |

| 複合年成長率 | 12.5% |

2024年,NAND快閃記憶體和託管儲存領域的市場規模預計為320萬美元。包括DRAM和SRAM在內的易失性記憶體對於ADAS(高級駕駛輔助系統)、資訊娛樂系統和自動駕駛應用中的高速處理至關重要。汽車製造商正擴大部署DRAM和SRAM來處理即時感測器資料和人工智慧驅動的功能,從而推動了下一代汽車平台的需求。

2024年,內燃機(ICE)汽車市場規模預計將達350萬美元。傳統汽車的ECU、資訊娛樂系統和安全系統仍然需要記憶體。 ADAS、車載資訊系統和車聯網功能的整合增加了對即時資料處理、儲存和監控的記憶體需求,從而持續推動了對DRAM、SRAM和快閃記憶體解決方案的需求。

美國汽車儲存半導體市場規模預計在2024年達到220萬美元,到2034年將以13%的複合年成長率成長。電動車、智慧網聯汽車和高級駕駛輔助系統(ADAS)的普及是推動市場成長的主要動力。包括《晶片和資訊安全法案》(CHIPS Act)在內的政府項目,促進了國內半導體生產,增強了供應鏈韌性,並刺激了汽車級記憶體的創新。機會包括原始設備製造商(OEM)與半導體製造商之間的合作,共同開發適用於電動車、自動駕駛汽車和支援空中升級(OTA)系統的可擴展、高能源效率儲存解決方案。

全球汽車記憶體半導體市場的主要參與者包括:Analog Devices, Inc.、Applied Materials, Inc.、Denso、L&T Semiconductor Technologies、Macronix International Co., Ltd.、Microchip Technology Inc.、NXP Semiconductors NV、OmniVision、ON Semem. Industries, LLC、Tongfu Microelectronics (TFME)、Toshiba 和 Valens Semiconductor。這些公司採取的關鍵策略包括:與汽車製造商建立策略合作夥伴關係,共同開發客製化的儲存解決方案;透過併購拓展技術組合;以及大力投資研發高容量、低延遲和高能源效率的記憶體。此外,各公司也正在擴大生產規模、提升供應鏈韌性並實現半導體製造的在地化。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 高級駕駛輔助系統(ADAS)和自動駕駛技術的日益普及

- 汽車電氣化(電動車和混合動力車)的成長

- 資訊娛樂系統與連網汽車系統的整合

- 汽車級記憶體技術的進步

- 車聯網(V2X)通訊的擴展

- 產業陷阱與挑戰

- 汽車級半導體的高製造成本和認證成本

- 快速的技術演進

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 歷史價格分析(2021-2024)

- 價格趨勢促進因素

- 區域價格差異

- 價格預測(2025-2034)

- 定價策略

- 新興商業模式

- 合規要求

- 永續性措施

- 永續材料評估

- 碳足跡分析

- 循環經濟實施

- 永續性認證和標準

- 永續性投資報酬率分析

- 全球消費者情緒分析

- 專利分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 對主要參與者進行競爭基準分析

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導人

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年主要發展動態

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型計劃

- 新興/新創企業競爭對手格局

第5章:市場估算與預測:依記憶體類型分類,2021-2034年

- 主要趨勢

- 揮發性記憶體(DRAM/SRAM)

- NOR快閃記憶體

- NAND快閃記憶體和管理型儲存

- 新興的非揮發性記憶體

第6章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 內燃機(ICE)車輛

- 混合動力電動車(HEV)

- 電池電動車(BEV)

- 自動駕駛汽車

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 高級駕駛輔助系統(ADAS)

- 資訊娛樂與互聯

- 動力系統和引擎控制

- 車身電子設備和儀錶板

- 其他

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 原始設備製造商 (OEM) SIA

- 一級汽車供應商 SEMI

- 記憶體模組製造商 JEDEC

- 電子控制單元 (ECU) 製造商 AEC

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Analog Devices, Inc.

- Applied Materials, Inc.

- Denso

- L&T Semiconductor Technologies

- Macronix International Co., Ltd.

- Microchip Technology Inc.

- NXP Semiconductors NV

- OmniVision

- ON Semiconductor (onsemi)

- Robert Bosch GmbH

- ROHM Co., Ltd.

- Semiconductor Components Industries, LLC

- Tongfu Microelectronics (TFME)

- Toshiba

- Valens Semiconductor

The Global Automotive Memory Semiconductors Market was valued at USD 8.2 million in 2024 and is estimated to grow at a CAGR of 12.5% to reach USD 26.5 million by 2034.

The rising adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies is fueling demand for high-performance automotive memory semiconductors. These systems require instantaneous processing of massive amounts of data from sensors, cameras, LiDAR, and radar units, creating a strong need for fast, reliable memory solutions. DRAM and NAND flash are crucial for enabling rapid storage, transfer, and analysis within complex computing platforms. As vehicles evolve toward higher automation, memory with larger capacity, low latency, and long-term endurance is becoming increasingly critical. The shift to electric and hybrid vehicles (EVs and HEVs) is further driving growth, as sophisticated electronic control units (ECUs) and battery management systems demand advanced memory for monitoring energy usage, performance, and safety. Memory components like NOR flash, NAND, and DRAM support real-time communication between sensors, powertrains, and control modules to optimize efficiency and stability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.2 Million |

| Forecast Value | $26.5 Million |

| CAGR | 12.5% |

The NAND flash and managed storage segment was valued at USD 3.2 million in 2024. Volatile memory types, including DRAM and SRAM, are essential for high-speed processing in ADAS, infotainment, and autonomous driving applications. Automakers are increasingly deploying DRAM and SRAM to handle real-time sensor data and AI-driven functions, fueling demand across next-generation vehicle platforms.

The internal combustion engine (ICE) vehicles segment generated USD 3.5 million in 2024. Traditional vehicles continue to require memory for ECUs, infotainment, and safety systems. The incorporation of ADAS, telematics, and connected vehicle features increases memory demands for real-time data processing, storage, and monitoring, sustaining the need for DRAM, SRAM, and flash solutions.

United States Automotive Memory Semiconductors Market reached USD 2.2 million in 2024 with a CAGR of 13% through 2034. Growth is driven by the adoption of EVs, connected vehicles, and ADAS. Government programs, including the CHIPS Act, promote domestic semiconductor production, enhance supply chain resilience, and stimulate innovation in automotive-grade memory. Opportunities include collaborations between OEMs and semiconductor manufacturers to develop scalable, energy-efficient memory solutions for EVs, autonomous vehicles, and over-the-air update-enabled systems.

Prominent Automotive Memory Semiconductors Market participants include Analog Devices, Inc., Applied Materials, Inc., Denso, L&T Semiconductor Technologies, Macronix International Co., Ltd., Microchip Technology Inc., NXP Semiconductors N.V., OmniVision, ON Semiconductor (onsemi), Robert Bosch GmbH, ROHM Co., Ltd., Semiconductor Components Industries, LLC, Tongfu Microelectronics (TFME), Toshiba, and Valens Semiconductor. Key strategies adopted by companies in the Global Automotive Memory Semiconductors Market include forging strategic partnerships with automakers to co-develop tailored memory solutions, pursuing mergers and acquisitions to broaden technology portfolios, and investing heavily in R&D for high-capacity, low-latency, and energy-efficient memory. Firms are also scaling up production facilities, improving supply chain resilience, and localizing semiconductor manufacturing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Packaging type trends

- 2.2.2 Material trends

- 2.2.3 Application trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspective: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of Advanced Driver Assistance Systems (ADAS) and autonomous driving

- 3.2.1.2 Growing vehicle electrification (EVs and HEVs)

- 3.2.1.3 Integration of infotainment and connected car systems

- 3.2.1.4 Advancements in automotive-grade memory

- 3.2.1.5 Expansion of vehicle-to-everything (V2X) communication

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and qualification costs of automotive-grade semiconductors

- 3.2.2.2 Rapid technology evolution

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability ROI analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Memory Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Volatile Memory (DRAM/SRAM)

- 5.3 NOR flash memory

- 5.4 NAND flash & managed storage

- 5.5 Emerging non-volatile memory

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Internal Combustion Engine (ICE) Vehicles

- 6.3 Hybrid Electric Vehicles (HEV)

- 6.4 Battery Electric Vehicles (BEV)

- 6.5 Autonomous vehicles

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Advanced Driver Assistance Systems (ADAS)

- 7.3 Infotainment & connectivity

- 7.4 Powertrain & engine control

- 7.5 Body electronics & instrument clusters

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Original Equipment Manufacturers (OEMs) SIA

- 8.3 Tier-1 automotive suppliers SEMI

- 8.4 Memory module manufacturers JEDEC

- 8.5 Electronic Control Unit (ECU) manufacturers AEC

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Analog Devices, Inc.

- 10.2 Applied Materials, Inc.

- 10.3 Denso

- 10.4 L&T Semiconductor Technologies

- 10.5 Macronix International Co., Ltd.

- 10.6 Microchip Technology Inc.

- 10.7 NXP Semiconductors N.V.

- 10.8 OmniVision

- 10.9 ON Semiconductor (onsemi)

- 10.10 Robert Bosch GmbH

- 10.11 ROHM Co., Ltd.

- 10.12 Semiconductor Components Industries, LLC

- 10.13 Tongfu Microelectronics (TFME)

- 10.14 Toshiba

- 10.15 Valens Semiconductor