|

市場調查報告書

商品編碼

1871125

電子業氧化鋅奈米顆粒市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Zinc Oxide Nanoparticles for Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

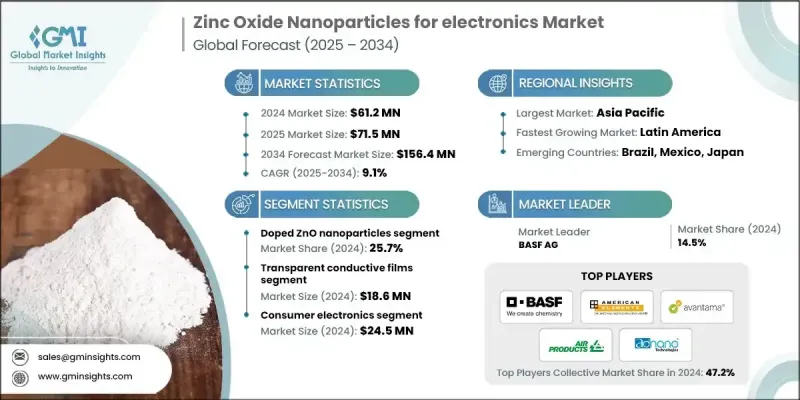

2024 年全球電子用氧化鋅奈米粒子市值為 6,120 萬美元,預計到 2034 年將以 9.1% 的複合年成長率成長至 1.564 億美元。

市場擴張的驅動力在於對小型化、高性能電子元件日益成長的需求。氧化鋅奈米結構具有卓越的電子遷移率、寬頻隙特性以及在可見光範圍內的透明性,使其成為先進電子產品(包括透明導電薄膜和高效感測器)的理想選擇。其獨特的特性,例如高比表面積、紫外線阻隔能力和優異的半導體性能,使其在薄膜電晶體、光電子裝置和軟性電子裝置中廣泛應用。亞太地區憑藉其強大的電子製造生態系統、充足的熟練勞動力和成本優勢,繼續在生產和消費領域佔據主導地位。隨著製造商將重心從通用材料轉向專用摻雜奈米顆粒、奈米棒和奈米線,以提升裝置性能和能源效率,對下一代電子產品和新型奈米結構研究的不斷投入和投入的增加,進一步推動了市場成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6120萬美元 |

| 預測值 | 1.564億美元 |

| 複合年成長率 | 9.1% |

摻雜氧化鋅奈米顆粒,連同奈米棒和奈米線,因其優異的電學和光學性能而備受關注,推動了軟性電子裝置、再生能源裝置和光電感測器等領域的創新。一維氧化鋅結構(包括奈米棒和奈米線)佔據了20.4%的市場佔有率,預計在2025年至2034年間將以9.7%的最高複合年成長率成長。其各向異性幾何結構提供了更大的表面積和定向電子傳輸能力,使其在感測器應用中表現出極高的效率。然而,可控比例合成仍然是一個挑戰,限制了其產量,同時也推動了持續的研發工作。此外,人們也正在探索諸如超音波輔助分散等先進製造方法來最佳化材料性能。

2024年,氣體感測器市佔率達到21.6%,預計到2034年將以8.4%的複合年成長率成長,這主要得益於物聯網設備和環境監測系統日益普及。氧化鋅奈米顆粒對多種氣體高度敏感,某些氣體的檢測反應時間僅需6-8秒。其自供電特性解決了能源效率問題,使其適用於分散式智慧感測器網路和即時監測應用。

2024年,北美電子用氧化鋅奈米顆粒市場規模達1,490萬美元。該地區受益於強大的電子製造基礎設施、先進的研究機構以及對智慧和穿戴式技術日益成長的需求。透明導電薄膜、紫外線感測器和壓電裝置等應用引領市場,並得到政府和私營部門的大力支持。科技公司與大學之間的策略合作正在加速商業化進程,並推動創新產品的開發。

全球電子氧化鋅奈米顆粒市場的主要企業包括American Elements、MSE Supplies LLC、SAT NANO、Techinstro、巴斯夫股份公司、Noah Chemicals、Shilpa Enterprises、Silox India Pvt Ltd、Avantama AG、AdNano Technologies Pvt Ltd和Ossila Ltd。這些企業正透過大力投資研發來提升氧化鋅奈米結構的電學和光學性能,從而鞏固其市場地位。他們正透過開發摻雜奈米顆粒、奈米棒和奈米線等產品,豐富其產品組合,以滿足軟性電子、感測器和再生能源設備等特殊應用的需求。與大學、研究機構和產業夥伴的策略合作正在加速創新和商業化進程。各企業致力於在維持產品品質的同時擴大生產規模,以滿足新興市場不斷成長的需求。強調卓越性能、可靠性和能源效率的行銷措施有助於提升品牌知名度並鞏固市場地位。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 電子設備小型化

- 對透明導電薄膜的需求日益成長

- 軟性電子技術的進步

- 日益成長的紫外線防護需求

- 產業陷阱與挑戰

- 監理合規的複雜性

- 製造規模化挑戰

- 健康與安全問題

- 市場機遇

- 新興量子點應用

- 下一代太陽能電池整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品

- 應用

- 最終用戶產業

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- Zno奈米顆粒(0d)

- 球形奈米顆粒(1-50 nm)

- 球形奈米顆粒(50-100 nm)

- 球形奈米顆粒(100-200 nm)

- ZnO奈米棒/奈米線(1d)

- 短奈米棒(長度<1 μm)

- 長奈米線(長度>1 μm)

- 排列整齊的奈米棒陣列

- 摻雜氧化鋅奈米粒子

- 鋁摻雜氧化鋅(AZO)

- 鎵摻雜氧化鋅(GZO)

- 摻銦氧化鋅(IZO)

- 其他金屬摻雜變體

- Zno量子點

- 超小型量子點(<5奈米)

- 中等量子點(5-10奈米)

- Zno奈米複合材料

- ZnO-石墨烯複合材料

- 鋅金屬雜化結構

- Zno-聚合物奈米複合材料

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 透明導電薄膜

- 顯示應用程式

- 觸控面板整合

- 太陽能電池電極

- 智慧窗戶技術

- 氣體感測器

- 環境監測感測器

- 工業製程控制感測器

- 汽車排放感知器

- 室內空氣品質感測器

- 光電探測器和紫外線感測器

- 紫外線A波段檢測系統

- 紫外線B和紫外線C檢測

- 火焰偵測應用

- 光通訊組件

- 薄膜電晶體(TFT)

- 顯示背板 TFT

- 軟性電子薄膜電晶體

- 射頻TFT

- 太陽能電池組件

- 電子傳輸層

- 光陽極應用

- 緩衝區整合

- 儲存裝置

- 阻變式隨機存取記憶體(ReRAM)

- 一次寫入多次讀取 (WORM) 內存

- 神經形態計算應用

第7章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 半導體製造

- 晶圓加工應用

- 濺鍍靶材生產

- 化學氣相沉積

- 原子層沉積

- 消費性電子產品

- 智慧型手機和平板電腦整合

- 穿戴式裝置應用

- 家用電器電子產品

- 遊戲和娛樂系統

- 汽車電子

- 高級駕駛輔助系統(ADA)

- 電動汽車零件

- 資訊娛樂系統

- 引擎控制單元

- 再生能源

- 光電電池製造

- 儲能系統

- 智慧電網技術

- 風能電子裝置

- 工業電子

- 過程控制系統

- 工廠自動化

- 機器人應用

- 電源管理系統

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- American Elements

- BASF AG

- Air Products and Chemicals Inc

- SAT NANO

- Techinstro

- MSE Supplies LLC

- Noah Chemicals

- Silox India Pvt Ltd

- Shilpa Enterprises

- Avantama AG

- Ossila Ltd

- AdNano Technologies Pvt Ltd

The Global Zinc Oxide Nanoparticles for Electronics Market was valued at USD 61.2 million in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 156.4 million by 2034.

The market expansion is driven by rising demand for miniaturized, high-performance electronic components. Zinc oxide nanostructures exhibit exceptional electron mobility, wide bandgap properties, and transparency in the visible light spectrum, making them ideal for advanced electronics, including transparent conductive films and high-efficiency sensors. Their unique features, such as high surface area, UV-blocking capability, and superior semiconducting behavior, have led to widespread adoption in thin-film transistors, optoelectronics, and flexible electronic devices. Asia Pacific continues to dominate production and consumption due to its robust electronics manufacturing ecosystem, availability of skilled labor, and cost advantages. Increasing investment in next-generation electronics and research into novel nanostructures further fuels growth, as manufacturers shift focus from commodity-grade materials to specialized doped nanoparticles, nanorods, and nanowires to enhance device performance and energy efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $61.2 Million |

| Forecast Value | $156.4 Million |

| CAGR | 9.1% |

Doped zinc oxide nanoparticles, along with nanorods and nanowires, are gaining prominence for their electrical and optical improvements, supporting innovations in flexible electronics, renewable energy devices, and optoelectronic sensors. One-dimensional ZnO structures, including nanorods and nanowires segments, held a 20.4% share and are expected to grow at the highest CAGR of 9.7% from 2025 to 2034. Their anisotropic geometry provides increased surface area and directional electron transport, making them highly effective in sensor applications. However, controlled ratio synthesis remains a challenge, limiting production while driving ongoing research and development efforts. Advanced manufacturing methods, such as ultrasonic-assisted distribution, are also being explored to optimize material performance.

The gas sensors segment held 21.6% share in 2024 and is expected to grow at a CAGR of 8.4% through 2034, driven by increasing adoption of IoT devices and environmental monitoring systems. Zinc oxide nanoparticles are highly sensitive to various gases and provide rapid response times of 6-8 seconds for certain detections. Their self-powered capability addresses energy efficiency concerns, making them suitable for distributed smart sensor networks and real-time monitoring applications.

North America Zinc Oxide Nanoparticles for Electronics Market accounted for USD 14.9 million in 2024. The region benefits from strong electronics manufacturing infrastructure, advanced research institutions, and growing demand for smart and wearable technologies. Applications in transparent conductive films, UV sensors, and piezoelectric devices are leading the market, supported by substantial government funding and private sector investment. Strategic collaborations between technology companies and universities are accelerating commercialization and enabling innovative product development.

Key companies operating in the Global Zinc Oxide Nanoparticles for Electronics Market include American Elements, MSE Supplies LLC, SAT NANO, Techinstro, BASF AG, Noah Chemicals, Shilpa Enterprises, Silox India Pvt Ltd, Avantama AG, AdNano Technologies Pvt Ltd, and Ossila Ltd. Companies in the Global Zinc Oxide Nanoparticles for Electronics Market are adopting strategies to solidify their position by investing heavily in research and development to improve the electrical and optical performance of ZnO nanostructures. They are diversifying their product portfolios with doped nanoparticles, nanorods, and nanowires for specialized applications in flexible electronics, sensors, and renewable energy devices. Strategic collaborations with universities, research institutes, and industrial partners are accelerating innovation and commercialization. Firms are focusing on scaling production while maintaining quality to meet rising demand in emerging markets. Marketing initiatives emphasizing superior performance, reliability, and energy efficiency help enhance brand visibility and strengthen market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of electronic devices

- 3.2.1.2 Growing demand for transparent conductive films

- 3.2.1.3 Advancement in flexible electronics

- 3.2.1.4 Increasing uv protection requirement

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory compliance complexity

- 3.2.2.2 Manufacturing scalability challenges

- 3.2.2.3 Health & safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging quantum dot applications

- 3.2.3.2 Next-generation solar cell integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.7.3 Application

- 3.7.4 End Use Industry

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Zno nanoparticles (0d)

- 5.2.1 Spherical nanoparticles (1-50 nm)

- 5.2.2 Spherical nanoparticles (50-100 nm)

- 5.2.3 Spherical nanoparticles (100-200 nm)

- 5.3 Zno nanorods/nanowires (1d)

- 5.3.1 Short nanorods (length <1 μm)

- 5.3.2 Long nanowires (length >1 μm)

- 5.3.3 Aligned nanorod arrays

- 5.4 Doped zno nanoparticles

- 5.4.1 Aluminum-doped zno (AZO)

- 5.4.2 Gallium-doped zno (GZO)

- 5.4.3 Indium-doped zno (IZO)

- 5.4.4 Other metal-doped variants

- 5.5 Zno quantum dots

- 5.5.1 Ultra-small quantum dots (<5 nm)

- 5.5.2 Medium quantum dots (5-10 nm)

- 5.6 Zno nanocomposites

- 5.6.1 Zno-graphene composites

- 5.6.2 Zno-metal hybrid structures

- 5.6.3 Zno-polymer nanocomposites

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Transparent conductive films

- 6.2.1 Display applications

- 6.2.2 Touch panel integration

- 6.2.3 Solar cell electrodes

- 6.2.4 Smart window technologies

- 6.3 Gas sensors

- 6.3.1 Environmental monitoring sensors

- 6.3.2 Industrial process control sensors

- 6.3.3 Automotive emission sensors

- 6.3.4 Indoor air quality sensors

- 6.4 Photodetectors & UV sensors

- 6.4.1 UV-a detection systems

- 6.4.2 UV-b & UV-c detection

- 6.4.3 Flame detection applications

- 6.4.4 Optical communication components

- 6.5 Thin Film Transistors (TFTs)

- 6.5.1 Display Backplane TFTs

- 6.5.2 Flexible Electronics TFTs

- 6.5.3 Radio Frequency TFTs

- 6.6 Solar Cell Components

- 6.6.1 Electron Transport Layers

- 6.6.2 Photoanode Applications

- 6.6.3 Buffer Layer Integration

- 6.7 Memory Devices

- 6.7.1 Resistive Random Access Memory (ReRAM)

- 6.7.2 Write-Once Read-Many (WORM) Memory

- 6.7.3 Neuromorphic Computing Applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Semiconductor manufacturing

- 7.2.1 Wafer processing applications

- 7.2.2 Sputtering target production

- 7.2.3 Chemical vapor deposition

- 7.2.4 Atomic layer deposition

- 7.3 Consumer electronics

- 7.3.1 Smartphone & tablet integration

- 7.3.2 Wearable device applications

- 7.3.3 Home appliance electronics

- 7.3.4 Gaming & entertainment systems

- 7.4 Automotive electronics

- 7.4.1 Advanced driver assistance systems (adas)

- 7.4.2 Electric vehicle components

- 7.4.3 Infotainment systems

- 7.4.4 Engine control units

- 7.5 Renewable energy

- 7.5.1 Photovoltaic cell manufacturing

- 7.5.2 Energy storage systems

- 7.5.3 Smart grid technologies

- 7.5.4 Wind power electronics

- 7.6 Industrial electronics

- 7.6.1 Process control systems

- 7.6.2 Factory automation

- 7.6.3 Robotics applications

- 7.6.4 Power management systems

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 American Elements

- 9.2 BASF AG

- 9.3 Air Products and Chemicals Inc

- 9.4 SAT NANO

- 9.5 Techinstro

- 9.6 MSE Supplies LLC

- 9.7 Noah Chemicals

- 9.8 Silox India Pvt Ltd

- 9.9 Shilpa Enterprises

- 9.10 Avantama AG

- 9.11 Ossila Ltd

- 9.12 AdNano Technologies Pvt Ltd

氧化鋅市場:依形態、通路和應用分類-2026-2032年全球市場預測

氧化鋅市場:依形態、通路和應用分類-2026-2032年全球市場預測 全球氧化鋅市場(至 2031 年):按製造流程(間接法、直接法和濕化學法)、等級(標準級、加工級、USP 級和 FCC 級)、應用(橡膠、陶瓷、化學品、化妝品和個人護理用品以及藥品)和地區分類。

全球氧化鋅市場(至 2031 年):按製造流程(間接法、直接法和濕化學法)、等級(標準級、加工級、USP 級和 FCC 級)、應用(橡膠、陶瓷、化學品、化妝品和個人護理用品以及藥品)和地區分類。 2026年全球氧化鋅市場報告

2026年全球氧化鋅市場報告 氧化鋅市場-全球產業規模、佔有率、趨勢、機會和預測,按形態、最終用戶、地區和競爭格局分類,2020-2030年預測

氧化鋅市場-全球產業規模、佔有率、趨勢、機會和預測,按形態、最終用戶、地區和競爭格局分類,2020-2030年預測 氧化鋅全球市場 - 預測 2025-20302026-2032年氧化鋅市場(依等級、應用、最終用途產業及地區)

氧化鋅全球市場 - 預測 2025-20302026-2032年氧化鋅市場(依等級、應用、最終用途產業及地區) 奈米氧化鋅市場報告,按類型(未塗層奈米氧化鋅、塗層奈米氧化鋅)、應用(個人護理和化妝品、油漆和塗料等)和地區,2025 年至 2033 年

奈米氧化鋅市場報告,按類型(未塗層奈米氧化鋅、塗層奈米氧化鋅)、應用(個人護理和化妝品、油漆和塗料等)和地區,2025 年至 2033 年 全球氧化鋅市場需求及預測分析(2018-2034)

全球氧化鋅市場需求及預測分析(2018-2034) 氧化鋅市場規模、佔有率、成長分析(按製程、應用、等級和地區)-2025-2032 年產業預測

氧化鋅市場規模、佔有率、成長分析(按製程、應用、等級和地區)-2025-2032 年產業預測 奈米氧化鋅市場、機會、成長動力、產業趨勢分析與預測,2024-2032

奈米氧化鋅市場、機會、成長動力、產業趨勢分析與預測,2024-2032