|

市場調查報告書

商品編碼

1871108

形狀記憶陶瓷在致動器應用領域的市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Shape Memory Ceramics for Actuator Applications Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

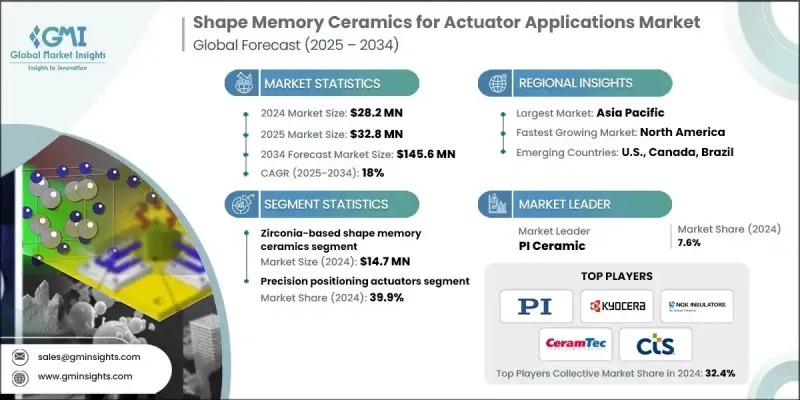

2024 年全球形狀記憶陶瓷致動器應用市場價值為 2,820 萬美元,預計到 2034 年將以 18% 的複合年成長率成長至 1.456 億美元。

形狀記憶陶瓷正迅速成為致動器技術領域最具創新性的智慧材料之一,它能夠在應力、溫度或電場等特定外部刺激下改變並恢復自身形狀。其高可靠性、優異的耐久性和高效性使其在包括航太、汽車、國防和醫療保健在內的現代工業中發揮著至關重要的作用。自動化、機器人和智慧製造技術的快速發展,進一步推動了對輕質、耐腐蝕且能夠在極端條件下工作的致動器的需求。與傳統的金屬致動器相比,這些陶瓷具有更優異的機械和熱性能,能夠在更長的使用壽命內保持穩定的運作。政府對先進材料和製造技術的扶持,以及不斷成長的研發投入,正在推動技術創新。此外,形狀記憶陶瓷在生物醫學設備和基於微機電系統(MEMS)的組件等新興領域的應用,凸顯了其在下一代工程應用中日益重要的作用。隨著各行業尋求能夠在嚴苛的運作環境中提供高精度、高重複性和高韌性的高效高性能致動器材料,形狀記憶陶瓷的重要性也與日俱增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2820萬美元 |

| 預測值 | 1.456億美元 |

| 複合年成長率 | 18% |

2024年,氧化鋯基形狀記憶陶瓷的市場規模達到1,470萬美元,佔據最大的市場佔有率。氧化鋯優異的抗張強度、高斷裂韌性和卓越的熱穩定性使其成為在極端溫度和壓力條件下應用的理想選擇。這些特性使得氧化鋯基材料能夠在維持形狀記憶特性的同時,克服陶瓷材料通常存在的脆性問題,從而確保其在航太、工業和能源應用中的穩定性能。

2024年,精密定位執行器市佔率達39.9%。其主導地位主要得益於其在半導體製造、光學系統和先進儀器等需要亞微米級精度的產業中的重要角色。對能夠在高溫下提供穩定運動控制和高精度的執行器的需求不斷成長,並持續推動此類執行器的應用。此外,陶瓷基執行器在超過300°C的高溫環境中也日益受到重視,因為傳統的金屬形狀記憶合金在這種高溫下往往會失去功能,這使得陶瓷基執行器成為航太和工業自動化系統的首選解決方案。

2025年至2034年間,北美形狀記憶陶瓷驅動器市場將以18.1%的複合年成長率成長。該地區市場成長的主要驅動力是航太、汽車和醫療器材製造等行業對精密高性能驅動器日益成長的需求。陶瓷成分技術的進步提高了其機械強度和反應速度,使其適用於在嚴苛環境下連續運作。此外,該地區對自動化、機器人和智慧製造的重視也加速了陶瓷驅動器系統的應用,這些系統具有更快、更耐用、更有效率的特性。

全球形狀記憶陶瓷驅動器應用市場的主要參與者包括京瓷株式會社、富士陶瓷株式會社、CeramTec集團、摩根先進材料公司、CTS株式會社、太陽誘電株式會社、東曹株式會社、先進陶瓷材料公司、NGK絕緣體公司、Niterra株式會社、PI Ceramic和Piezo。這些公司正實施多元化的策略,以鞏固其市場地位和競爭優勢。許多公司正投入大量資金進行研發,以開發具有更高耐熱性和機械強度的先進氧化鋯和氧化鋁基配方。與航太、醫療和工業製造商的合作有助於拓展應用領域。此外,各公司也著力擴大產能,以滿足關鍵產業對精密驅動器日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 航太工業對高性能執行器的需求

- MEMS和微型致動器系統的小型化趨勢

- 優異的耐化學腐蝕性能

- 產業陷阱與挑戰

- 高昂的製造成本和複雜的加工要求

- 脆性和斷裂韌性限制

- 市場機遇

- 混合金屬-陶瓷複合材料的開發

- 用於環境合規的無鉛鐵電系統

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)

(註:僅提供重點國家的貿易統計。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- 氧化鋯基形狀記憶陶瓷

- 鈰摻雜氧化鋯(CeO2-ZrO2)

- 氧化釔穩定四方氧化鋯

- 摻雜異價摻雜劑的改質氧化鋯

- 鐵電形狀記憶陶瓷

- 鋯鈦酸鉛(PZT)

- 無鉛鐵電陶瓷

- 氧化鉿(HfO2)薄膜

- 複合形狀記憶陶瓷

- 金屬基複合材料

- 氧化鋯增韌氧化鋁(ZTA)

- 有機-無機雜化複合材料

- 其他

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 精密定位執行器

- 奈米級光學定位系統

- MEMS和微型致動器應用

- 快速轉向鏡和光學指向

- 高溫致動器

- 航太引擎控制系統

- 深井及極端環境應用

- 工業高溫製程控制

- 射頻和微波致動器

- 可重構天線系統

- 超材料和超表面應用

- 立方體衛星和太空通訊系統

- 微流控和晶片實驗室致動器

- 微型閥和微型幫浦系統

- 微型機器人應用

- 生物醫學設備整合

- 其他

第7章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 航太與國防

- 飛機變形機翼結構

- 太空船可展開機構

- 軍用精密光學系統

- 汽車

- 引擎熱管理系統

- 自適應懸吊和振動控制

- 電池熱管理

- 工業自動化與機器人

- 精密製造設備

- 機器人系統執行器

- 過程控制與流程管理

- 電子與半導體

- 微機電系統及微機電系統

- 光交換和光纖定位

- 半導體加工設備

- 醫學與生物醫學

- 手術器械驅動器

- 晶片實驗室診斷設備

- 生物相容性驅動系統

- 其他

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Advanced Ceramic Material

- CeramTec Group

- CTS Corporation

- FUJI CERAMICS CORPORATION

- Kyocera Corporation

- Morgan Advanced Materials

- NGK Insulators

- Niterra Co., Ltd.

- PI Ceramic

- Piezo Direct

- TAIYO YUDEN CO., LTD.

- Tosoh Corporation

The Global Shape Memory Ceramics for Actuator Applications Market was valued at USD 28.2 million in 2024 and is estimated to grow at a CAGR of 18% to reach USD 145.6 million by 2034.

Shape memory ceramics are emerging as one of the most innovative smart materials in actuator technology, capable of changing and restoring their shape under specific external stimuli such as stress, temperature, or electric fields. Their ability to offer high reliability, excellent durability, and efficiency makes them vital in modern industries, including aerospace, automotive, defense, and healthcare. The rapid expansion of automation, robotics, and smart manufacturing technologies is amplifying the demand for actuators that are lightweight, corrosion-resistant, and capable of functioning under extreme conditions. Compared with conventional metallic actuators, these ceramics deliver superior mechanical and thermal performance, allowing consistent operation over extended lifecycles. Increasing R&D investments, supported by government initiatives focused on advanced materials and manufacturing, are fueling technological innovation. Furthermore, the integration of shape memory ceramics into emerging fields such as biomedical devices and MEMS-based components highlights their expanding role in next-generation engineering applications. Their significance continues to rise as industries seek efficient and high-performance actuator materials that deliver precision, repeatability, and resilience in demanding operational environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $28.2 million |

| Forecast Value | $145.6 million |

| CAGR | 18% |

The zirconia-based shape memory ceramics generated USD 14.7 million in 2024, accounting for the largest share of the market. Zirconia's superior tensile strength, high fracture toughness, and remarkable thermal stability make it a preferred choice for applications operating in extreme temperature and pressure conditions. These properties allow zirconia-based materials to retain shape memory characteristics while addressing the brittleness typically associated with ceramic materials, ensuring stable performance in aerospace, industrial, and energy applications.

The precision positioning actuator segment held a 39.9% share in 2024. This dominance is driven by their critical use in industries requiring sub-micrometer accuracy, such as semiconductor manufacturing, optical systems, and advanced instrumentation. The growing demand for actuators that provide consistent motion control and high accuracy under elevated temperatures continues to boost adoption. Ceramic-based actuators are also gaining prominence in high-temperature environments exceeding 300°C, where conventional metallic shape memory alloys tend to lose functionality, positioning them as the preferred solution for aerospace and industrial automation systems.

North America Shape Memory Ceramics for Actuator Applications Market will grow at a CAGR of 18.1% between 2025 and 2034. Regional growth is driven by the increasing need for precise and high-performance actuators across aerospace, automotive, and medical device manufacturing sectors. Technological advancements in ceramic compositions have improved their mechanical strength and response time, making them suitable for continuous operation in challenging environments. Additionally, the region's emphasis on automation, robotics, and smart manufacturing is accelerating the adoption of ceramic-based actuator systems that offer faster, more durable, and efficient performance.

Key players operating in the Global Shape Memory Ceramics for Actuator Applications Market include Kyocera Corporation, FUJI CERAMICS CORPORATION, CeramTec Group, Morgan Advanced Materials, CTS Corporation, TAIYO YUDEN CO., LTD., Tosoh Corporation, Advanced Ceramic Material, NGK Insulators, Niterra Co., Ltd., PI Ceramic, and Piezo Direct. Companies in the Global Shape Memory Ceramics for Actuator Applications Market are implementing diverse strategies to reinforce their market foothold and competitive edge. Many are channeling significant investments into R&D to develop advanced zirconia and alumina-based formulations with enhanced thermal endurance and mechanical strength. Partnerships and collaborations with aerospace, medical, and industrial manufacturers are helping broaden application portfolios. Firms are also emphasizing capacity expansion to meet the growing demand for precision actuators across critical industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aerospace industry demand for high-performance actuators

- 3.2.1.2 Miniaturization trends in mems & microactuator systems

- 3.2.1.3 Superior chemical & corrosion resistance properties

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs & complex processing requirements

- 3.2.2.2 Brittleness & fracture toughness limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Hybrid metal-ceramic composite development

- 3.2.3.2 Lead-free ferroelectric systems for environmental compliance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Zirconia-based shape memory ceramics

- 5.2.1 Ceria-doped zirconia (CeO2-ZrO2)

- 5.2.2 Yttria-stabilized tetragonal zirconia

- 5.2.3 Modified zirconia with aliovalent dopants

- 5.3 Ferroelectric shape memory ceramics

- 5.3.1 Lead zirconate titanate (PZT)

- 5.3.2 Lead-free ferroelectric ceramics

- 5.3.3 Hafnium oxide (HfO2) thin film

- 5.4 Composite shape memory ceramics

- 5.4.1 Metal matrix composites

- 5.4.2 Zirconia-toughened alumina (ZTA)

- 5.4.3 Hybrid organic-inorganic composites

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Precision positioning actuators

- 6.2.1 Nanometer-scale optical positioning systems

- 6.2.2 MEMS & microactuator applications

- 6.2.3 Fast-steering mirrors & optical pointing

- 6.3 High-temperature actuators

- 6.3.1 Aerospace engine control systems

- 6.3.2 Deep borehole & extreme environment applications

- 6.3.3 Industrial high-temperature process control

- 6.4 RF & microwave actuators

- 6.4.1 Reconfigurable antenna systems

- 6.4.2 Metamaterial & metasurface applications

- 6.4.3 CubeSat & space communication systems

- 6.5 Microfluidic & lab-on-chip actuators

- 6.5.1 Microvalves & micropump systems

- 6.5.2 Microrobotic applications

- 6.5.3 Biomedical device integration

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Aerospace & defense

- 7.2.1 Aircraft morphing wing structures

- 7.2.2 Spacecraft deployable mechanisms

- 7.2.3 Military precision optical systems

- 7.3 Automotive

- 7.3.1 Engine thermal management systems

- 7.3.2 Adaptive suspension & vibration control

- 7.3.3 Battery thermal management

- 7.4 Industrial automation & robotics

- 7.4.1 Precision manufacturing equipment

- 7.4.2 Robotic system actuators

- 7.4.3 Process control & flow management

- 7.5 Electronics & semiconductors

- 7.5.1 MEMS & microelectromechanical systems

- 7.5.2 Optical switching & fiber positioning

- 7.5.3 Semiconductor processing equipment

- 7.6 Medical & biomedical

- 7.6.1 Surgical instrument actuators

- 7.6.2 Lab-on-chip diagnostic devices

- 7.6.3 Biocompatible actuation systems

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Advanced Ceramic Material

- 9.2 CeramTec Group

- 9.3 CTS Corporation

- 9.4 FUJI CERAMICS CORPORATION

- 9.5 Kyocera Corporation

- 9.6 Morgan Advanced Materials

- 9.7 NGK Insulators

- 9.8 Niterra Co., Ltd.

- 9.9 PI Ceramic

- 9.10 Piezo Direct

- 9.11 TAIYO YUDEN CO., LTD.

- 9.12 Tosoh Corporation