|

市場調查報告書

商品編碼

1871100

先進光刻技術用光阻化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Photoresist Chemicals for Advanced Lithography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

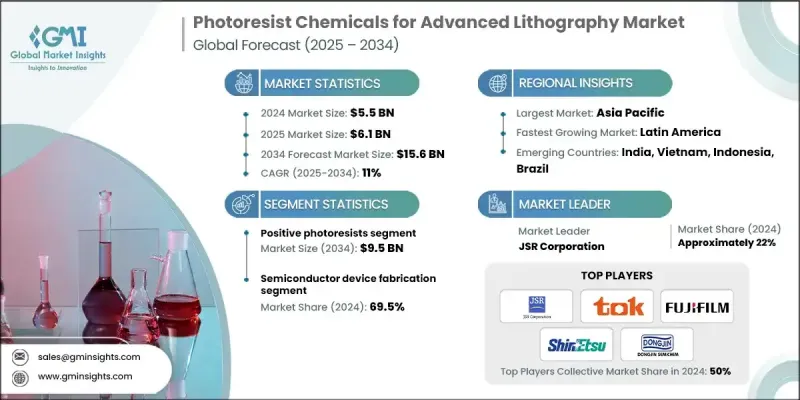

2024 年全球先進光阻化學品市場價值為 55 億美元,預計到 2034 年將以 11% 的複合年成長率成長至 156 億美元。

亞太地區投資的成長、高數值孔徑極紫外線(High-NA EUV)系統的商業化以及3D封裝技術的進步正在推動市場發展。 7奈米和5奈米以下製程節點的採用、極紫外光刻技術的日益普及以及人工智慧、5G和汽車應用領域對高性能晶片不斷成長的需求,都在推動著這項變革。波長為13.5奈米的極紫外線(EUV)光刻技術能夠實現5奈米線寬的圖案化,顯著提升了對化學放大光阻(CAR)和金屬氧化物基極紫外光阻的需求。向高數值孔徑極紫外光刻、結合深紫外線(DUV)和極紫外光(EUV)的混合微影以及定向自組裝(DSA)技術的演進,正在重塑光阻的化學系統。像 JSR、TOK、東進半導體和富士膠片這樣的行業領導者正在調整產品路線圖,以適應 2nm 和 1.4nm 節點的準備情況,這標誌著從傳統的 KrF/i 線光阻向 EUV 平台的明顯轉變。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 55億美元 |

| 預測值 | 156億美元 |

| 複合年成長率 | 11% |

2024年,正性光阻市場規模達34億美元,預計2034年將達95億美元,年複合成長率達10.7%。化學放大光阻在該領域佔據主導地位,其對10奈米以下尺寸的裝置具有高靈敏度,並能實現精確的製程控制。該領域的創新主要集中在提高抗蝕刻性、開發模組化光阻方案以及最大限度地減少極紫外光刻中的二次電子模糊,所有這些對於在小尺寸下最大限度地提高良率都至關重要。

由於半導體裝置製造領域對用於先進邏輯、記憶體、類比和人工智慧晶片的高純度、高效能光阻的需求,預計到2024年,該領域將佔據69.5%的市場佔有率。多重曝光複雜性的增加和高數值孔徑極紫外光刻(High-NA EUV)技術的普及,使得採用5nm、3nm以及即將推出的2nm製程節點生產的邏輯元件(包括CPU、GPU和SoC)成為光阻材料的最大消耗者。

2024年,美國先進光阻化學品市場規模為8.174億美元,預計將以10.8%的複合年成長率成長,到2034年達到23億美元。北美市場的成長主要得益於半導體產業振興政策,包括鼓勵國內晶片生產的立法。隨著主要製造商新建製造工廠,這些政策正在推動對本地採購的光阻和先進光刻材料的需求。

先進光阻劑化學品市場的主要參與者包括默克集團(Merck KGaA)、布魯爾科學公司(Brewer Science, Inc.)、陶氏化學(Dow)、富士膠卷控股株式會社(Fujifilm Holdings Corporation)、Inpria Corporation、東進半導體株式會(Dongjtern Schemy. Ltd.)、信越化學株式會社(Shin-Etsu Chemical Co., Ltd.)、JSR株式會社(JSR Corporation)、化藥先進材料株式會社(Kayaku Advanced Materials)、東京櫻工業株式會社(Tokyo Ohka Kogyo Co., Ltd.)、Micro Chemist Technology GmbH、起友化學公司(Sucroed Resist Technology Gmbical) Company)、江蘇那塔光電材料有限公司(Jiangsu Nata Opto-electronic Material Co., Ltd.)及Irresistible Materials Ltd.。領先企業正大力投資研發,以開發適用於高數值孔徑極紫外光刻(High-NA EUV)和5奈米以下製程節點的新一代光阻化學品。與半導體製造商的策略合作有助於將產品創新與商業光刻需求相匹配。各公司正在擴大亞太和北美地區的產能,以滿足不斷成長的區域需求。一些企業專注於混合光刻解決方案和定向自組裝技術,以拓寬產品的應用範圍。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依類型分類,2021-2034年

- 主要趨勢

- 正性光阻

- 丙烯酸酯類光阻

- 基於酚醛樹脂(dnq)的系統

- 聚甲基丙烯酸甲酯(PMMA)

- 負性光阻

- 環氧樹脂基

- 含矽光阻劑

- 金屬基光阻

第6章:市場估算與預測:依光刻技術分類,2021-2034年

- 主要趨勢

- 杜夫光刻

- 248nm krf光刻

- 193nm乾法光刻

- 193nm浸沒式微影(arfi)

- 極紫外線(EUV)光刻

- 紫外光@13.5 nm

- 高納 euv

- I線光刻(365奈米)

- 奈米壓印光刻(無)

- 電子束光刻

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 半導體裝置製造

- 邏輯元件

- 儲存裝置

- 邊緣設備

- 影像感測器

- MEMS元件

- 汽車記憶體

- 消費性電子記憶體

- 工業和醫療保健存儲器

- 顯示電子應用

- LCD製造

- OLED顯示器生產

- 下一代顯示器

- 先進封裝應用

- 3D包裝

- 系統級封裝(SIP)

- 晶圓級封裝(WLP)

- 光掩模製造

- EUV掩模

- DUV 掩模

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Brewer Science, Inc.

- Dongjin Semichem Co., Ltd.

- Dow

- Eternal Materials Co., Ltd.

- Fujifilm Holdings Corporation

- Inpria Corporation

- Irresistible Materials Ltd.

- Jiangsu Nata Opto-electronic Material Co., Ltd.

- JSR Corporation

- Kayaku Advanced Materials

- Merck KGaA

- Micro Resist Technology GmbH

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Company

- Tokyo Ohka Kogyo Co., Ltd.

- Others

The Global Photoresist Chemicals for Advanced Lithography Market was valued at USD 5.5 Billion in 2024 and is estimated to grow at a CAGR of 11% to reach USD 15.6 Billion by 2034.

The market is being propelled by rising investments in the Asia-Pacific region, the commercialization of High-NA EUV systems, and advancements in 3D packaging technologies. The adoption of sub-7nm and sub-5nm process nodes, growing use of EUV lithography, and increasing demand for high-performance chips in AI, 5G, and automotive applications are driving this transformation. Extreme Ultraviolet (EUV) lithography at 13.5 nm wavelengths is enabling the patterning of 5nm line widths, significantly boosting demand for chemically amplified resists (CARs) and metal-oxide-based EUV photoresists. The evolution toward High-NA EUV, hybrid lithography combining DUV and EUV, and directed self-assembly (DSA) is reshaping resist chemistries. Industry leaders like JSR, TOK, Dongjin Semichem, and Fujifilm are aligning product roadmaps with 2nm and 1.4nm node readiness, marking a clear shift from traditional KrF/i-line resists to EUV-focused platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.5 Billion |

| Forecast Value | $15.6 Billion |

| CAGR | 11% |

The positive photoresists segment generated USD 3.4 Billion in 2024 and is expected to reach USD 9.5 Billion by 2034, growing at a CAGR of 10.7%. Chemically amplified resists dominate this segment, offering high sensitivity for sub-10nm geometries and enabling precise process control. Innovations in this space focus on improving etch resistance, developing modular photoresist options, and minimizing secondary electron blur in EUV lithography, all critical to maximizing yields at small dimensions.

The semiconductor device fabrication segment held a 69.5% share in 2024 owing to its need for high-purity, high-performance photoresists used in advanced logic, memory, analog, and AI-focused chips. Increasing multi-patterning complexity and High-NA EUV adoption make logic devices, including CPUs, GPUs, and SoCs produced at 5nm, 3nm, and soon 2nm nodes, the largest consumers of photoresist materials.

U.S. Photoresist Chemicals for Advanced Lithography Market generated USD 817.4 million in 2024 and is expected to grow at a CAGR of 10.8% to reach USD 2.3 Billion by 2034. North America's growth is being fueled by semiconductor revitalization policies, including legislation encouraging domestic chip production. These policies are driving the demand for locally sourced photoresist and advanced lithography materials as new fabrication facilities are established by major manufacturers.

Key players in the Photoresist Chemicals for Advanced Lithography Market include Merck KGaA, Brewer Science, Inc., Dow, Fujifilm Holdings Corporation, Inpria Corporation, Dongjin Semichem Co., Ltd., Eternal Materials Co., Ltd., Shin-Etsu Chemical Co., Ltd., JSR Corporation, Kayaku Advanced Materials, Tokyo Ohka Kogyo Co., Ltd., Micro Resist Technology GmbH, Sumitomo Chemical Company, Jiangsu Nata Opto-electronic Material Co., Ltd., and Irresistible Materials Ltd. Leading companies are investing heavily in R&D to develop next-generation resist chemistries suitable for High-NA EUV and sub-5nm process nodes. Strategic collaborations with semiconductor manufacturers help align product innovations with commercial lithography requirements. Firms are expanding production capacities in Asia-Pacific and North America to meet rising regional demand. Some players focus on hybrid lithography solutions and directed self-assembly technologies to broaden product applicability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Lithography technology

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Positive photoresists

- 5.2.1 Acrylate-based photoresists

- 5.2.2 Novolac-based (dnq) systems

- 5.2.3 Poly (methyl methacrylate) (PMMA)

- 5.3 Negative photoresists

- 5.3.1 Epoxy-based

- 5.3.2 Silicon-containing resists

- 5.3.3 Metal-based resists

Chapter 6 Market Estimates and Forecast, By Lithography Technology, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Duv lithography

- 6.2.1 248nm krf lithography

- 6.2.2 193nm dry lithography

- 6.2.3 193nm immersion lithography (arfi)

- 6.3 Extreme ultraviolet (euv) lithography

- 6.3.1 Euv @ 13.5 nm

- 6.3.2 High-na euv

- 6.4 I-line lithography (365 nm)

- 6.5 Nanoimprint lithography (nil)

- 6.6 E-beam lithography

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Semiconductor device fabrication

- 7.2.1 Logic devices

- 7.2.2 Memory devices

- 7.2.3 Edge devices

- 7.2.4 Image sensors

- 7.3 Mems devices

- 7.3.1 Automotive mems

- 7.3.2 Consumer electronics mems

- 7.3.3 Industrial & healthcare mems

- 7.4 Display electronics applications

- 7.4.1 LCD manufacturing

- 7.4.2 OLED display production

- 7.4.3 Next-generation displays

- 7.5 Advanced packaging applications

- 7.5.1 3d packaging

- 7.5.2 System-in-package (SIP)

- 7.5.3 Wafer-level packaging (WLP)

- 7.6 Photomask manufacturing

- 7.6.1 EUV mask

- 7.6.2 DUV mask

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Brewer Science, Inc.

- 9.2 Dongjin Semichem Co., Ltd.

- 9.3 Dow

- 9.4 Eternal Materials Co., Ltd.

- 9.5 Fujifilm Holdings Corporation

- 9.6 Inpria Corporation

- 9.7 Irresistible Materials Ltd.

- 9.8 Jiangsu Nata Opto-electronic Material Co., Ltd.

- 9.9 JSR Corporation

- 9.10 Kayaku Advanced Materials

- 9.11 Merck KGaA

- 9.12 Micro Resist Technology GmbH

- 9.13 Shin-Etsu Chemical Co., Ltd.

- 9.14 Sumitomo Chemical Company

- 9.15 Tokyo Ohka Kogyo Co., Ltd.

- 9.16 Others

2026年光阻劑電子化學品全球市場報告

2026年光阻劑電子化學品全球市場報告 光阻劑原料市場按應用、抗蝕劑類型、材料類型、技術和最終用戶分類-2026-2032年全球預測光阻劑電子化學品市場按類型、形態、技術、應用和最終用戶分類 - 全球預測 2026-2032半導體光阻劑材料市場:按類型、曝光技術、晶圓尺寸和應用分類-2026-2032年全球預測

光阻劑原料市場按應用、抗蝕劑類型、材料類型、技術和最終用戶分類-2026-2032年全球預測光阻劑電子化學品市場按類型、形態、技術、應用和最終用戶分類 - 全球預測 2026-2032半導體光阻劑材料市場:按類型、曝光技術、晶圓尺寸和應用分類-2026-2032年全球預測 光阻劑化學品市場-2025-2030年預測

光阻劑化學品市場-2025-2030年預測 全球液態光阻劑市場

全球液態光阻劑市場 2030 年光致變色材料市場預測:按產品、類型、材料、技術、應用、最終用戶和地區進行的全球分析ArF乾式及ArF浸液抗蝕劑材料的全球市場規模:各類型,各用途,各地區,範圍及預測負性光阻劑化學品的全球市場:分析 - 按類型、按藥物、按應用、按地區、預測(至 2030 年)

2030 年光致變色材料市場預測:按產品、類型、材料、技術、應用、最終用戶和地區進行的全球分析ArF乾式及ArF浸液抗蝕劑材料的全球市場規模:各類型,各用途,各地區,範圍及預測負性光阻劑化學品的全球市場:分析 - 按類型、按藥物、按應用、按地區、預測(至 2030 年) 光阻電子化學品市場,按類型、形式、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

光阻電子化學品市場,按類型、形式、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測