|

市場調查報告書

商品編碼

1871087

阻火器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Flame Arrestors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

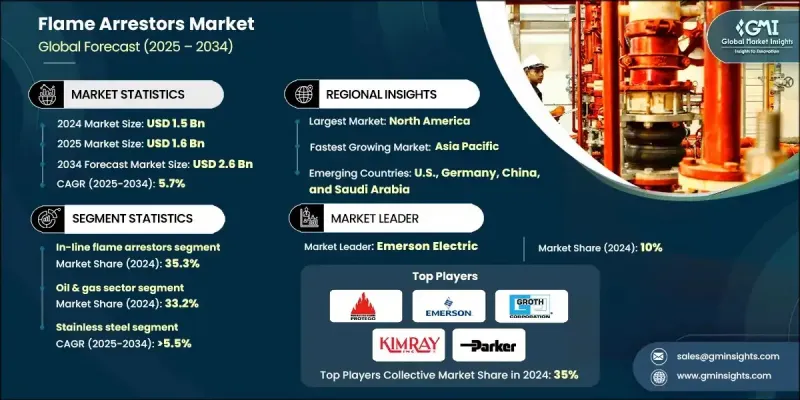

2024 年全球阻火器市場價值為 15 億美元,預計到 2034 年將以 5.7% 的複合年成長率成長至 26 億美元。

對工業安全合規性的日益重視,以及石化、煉油和倉儲行業監管的加強,正推動市場穩步擴張。發展中國家燃料和化學品儲存設施建設的不斷增加,以及與空氣排放相關的環境審查日益嚴格,並持續影響市場前景。阻火器是一種關鍵的安全裝置,它透過吸熱元件(通常由金屬網或多孔材料構成)抑制火焰鋒面,從而防止含有易燃氣體或蒸氣混合物的系統中火焰蔓延。這種設計將火焰冷卻到燃點以下,有效阻止燃燒。在嚴格的防爆和安全標準的推動下,工業設施中氫氣利用和混合活動的激增,正在推動市場成長。工業基礎設施的不斷進步、蒸汽回收和排放控制技術的整合,以及對可靠通風解決方案日益成長的需求,進一步促進了產品的推廣應用。不斷擴大的海上支援作業和海上加油活動,以及日益嚴格的船舶安全要求,也為全球市場的發展勢頭做出了貢獻。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15億美元 |

| 預測值 | 26億美元 |

| 複合年成長率 | 5.7% |

2024年,管道式阻火器市佔率達到35.3%,預計到2034年將以5.5%的複合年成長率成長。這些裝置對於維護工業管道網路的製程安全至關重要,能夠阻止火焰向上游和下游方向蔓延。由於高風險環境中對持續雙向保護的需求,管道式阻火器在化學、石化和流程製造設施中的應用日益廣泛。其可靠性和對複雜製程系統的適應性使其成為現代工業運作中不可或缺的組件,這些運作旨在預防爆炸並確保製程完整性。

2024年,石油天然氣產業佔33.2%的市場佔有率,預計2025年至2034年間將以5.5%的複合年成長率成長。該產業的成長主要得益於上游、中游和下游業務的持續擴張,而這些業務都需要可靠的阻燃技術。在生產、鑽井和加工作業中,阻火器用於在日常和緊急情況下保護設施免受碳氫化合物蒸氣的點燃。整個能源價值鏈對營運安全和合規性的持續關注仍然是影響產品需求的關鍵因素。

2024年,美國阻火器市場規模預計將達到4.17億美元。該國市場成長主要得益於煉油、石化和發電設施的現代化改造,以及職業安全和消防安全法規執行的加強。液化天然氣設施和氫氣摻混專案的投資增加,進一步加速了阻火器在工業應用中的部署。此外,企業擴大採用基於風險的維護計劃和資產完整性管理策略,從而主動用先進合規的系統取代老舊的阻火設備。

全球阻火器市場的主要參與者包括派克漢尼汾 (Parker Hannifin)、艾爾馬克科技 (Elmac Technologies)、艾默生電氣 (Emerson Electric)、Protectoseal 公司、PROTEGO、Sunflow Technologies、D-KTC 流體控制、L&J Technologies、Cashco、Kimray、GrTT-GASETEC、GrTT. Innovations、Cochin Steel、Paradox IP、Aager 和 Mott。阻火器市場的關鍵企業正在實施多元化的策略,以鞏固其市場地位並提升競爭力。領先的製造商正加大研發投入,開發符合不斷更新的安全標準且能在極端工業條件下運作的高性能阻火器。他們積極尋求策略併購、合作與聯盟,以拓展產品組合併擴大地域覆蓋範圍。此外,各公司也致力於利用先進材料和自動化技術來提高生產效率。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

- 阻火器的成本結構分析

- 新興機會與趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- Key partnerships & collaborations

- Major M&A activities

- Product innovations & launches

- Market expansion strategies

- 策略舉措

- 競爭性標竿分析

- 創新與技術格局

第5章:市場規模及預測:依產品分類,2021-2034年

- 主要趨勢

- 直列式阻火器

- 管線末端阻火器

- 爆燃抑制器

- 防爆器

- 其他

第6章:市場規模及預測:依材料分類,2021-2034年

- 主要趨勢

- 不銹鋼

- 碳鋼

- 鋁

- 其他

第7章:市場規模及預測:依最終用途分類,2021-2034年

- 主要趨勢

- 石油和天然氣

- 化學品

- 製藥

- 煉油廠

- 發電廠

- 礦業

- 廢水處理

- 其他

第8章:市場規模及預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- PROTEGO

- Aager

- Amarama Engineers

- BS&B Innovations

- Cashco

- Cochin Steel

- D-KTC Fluid Control

- Elmac Technologies

- Emerson Electric

- Essex Industries

- Fidicon Devices

- Groth Corporation

- Kimray

- L&J Technologies

- Mott

- Paradox IP

- Parker Hannifin

- Sunflow Technologies

- The Protectoseal Company

- WITT-GASETECHNIK

The Global Flame Arrestors Market was valued at USD 1.5 Billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.6 Billion by 2034.

Growing emphasis on industrial safety compliance, coupled with stronger regulatory mandates across petrochemical, refining, and storage sectors, is driving steady market expansion. Increasing construction of fuel and chemical storage facilities in developing economies, along with rising environmental scrutiny related to air emissions, continues to shape the business outlook. A flame arrestor is a critical safety device that prevents the spread of flames in systems containing flammable gas or vapor mixtures by quenching the flame front through a heat-absorbing element, often composed of metal mesh or porous materials. This design cools the flame below its ignition temperature, effectively halting combustion. The surge in hydrogen utilization and blending activities within industrial facilities, driven by stringent explosion prevention and safety standards, is propelling market growth. Continuous advancements in industrial infrastructure, the integration of vapor recovery and emission control technologies, and the rising demand for reliable venting solutions are further enhancing product deployment. Expanding offshore support operations and maritime fueling activities, together with reinforced shipboard safety requirements, are also contributing to global market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5.7% |

The in-line flame arrestor segment held 35.3% share in 2024 and is forecast to grow at a CAGR of 5.5% through 2034. These devices are essential for maintaining process safety in industrial piping networks by preventing flame travel in both upstream and downstream directions. Their growing application across chemical, petrochemical, and process manufacturing facilities is fueled by the need for continuous bidirectional protection in high-risk environments. Their reliability and adaptability to complex process systems make them indispensable components for modern industrial operations focused on explosion prevention and process integrity.

The oil & gas sector held a 33.2% share in 2024 and is expected to grow at a CAGR of 5.5% between 2025 and 2034. Growth in this sector is driven by ongoing expansion across upstream, midstream, and downstream operations, each requiring dependable flame prevention technologies. Applications within production, drilling, and processing operations rely on flame arrestors to safeguard facilities from the ignition of hydrocarbon vapors during routine and emergency scenarios. The continuous focus on operational safety and regulatory compliance across the energy value chain remains a key factor influencing product demand.

United States Flame Arrestors Market generated USD 417 million in 2024. Market growth in the country is supported by the modernization of refining, petrochemical, and power generation assets, accompanied by heightened enforcement of occupational and fire safety regulations. Expanding investments in LNG facilities and hydrogen blending initiatives are further accelerating the deployment of flame arrestors in industrial applications. Additionally, companies are increasingly adopting risk-based maintenance programs and asset integrity management strategies, resulting in proactive replacement of outdated flame protection equipment with advanced, compliant systems.

Prominent players operating in the Global Flame Arrestors Market include Parker Hannifin, Elmac Technologies, Emerson Electric, The Protectoseal Company, PROTEGO, Sunflow Technologies, D-KTC Fluid Control, L&J Technologies, Cashco, Kimray, WITT-GASETECHNIK, Essex Industries, Groth Corporation, Amarama Engineers, Fidicon Devices, BS&B Innovations, Cochin Steel, Paradox IP, Aager, and Mott. Key companies in the Flame Arrestors Market are implementing diverse strategies to strengthen their market position and enhance competitiveness. Leading manufacturers are investing in R&D to develop high-performance arrestors that meet evolving safety standards and can operate under extreme industrial conditions. Strategic mergers, partnerships, and collaborations are being pursued to expand product portfolios and extend geographic reach. Companies are also focusing on production efficiency using advanced materials and automation in manufacturing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Material trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of flame arrestors

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization and IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 In-line flame arrestors

- 5.3 End-of-line flame arrestors

- 5.4 Deflagration arrestors

- 5.5 Detonation arrestors

- 5.6 Others

Chapter 6 Market Size and Forecast, By Material, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Carbon steel

- 6.4 Aluminum

- 6.5 Others

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Chemicals

- 7.4 Pharmaceutical

- 7.5 Refineries

- 7.6 Power plants

- 7.7 Mining

- 7.8 Wastewater treatment

- 7.9 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 PROTEGO

- 9.2 Aager

- 9.3 Amarama Engineers

- 9.4 BS&B Innovations

- 9.5 Cashco

- 9.6 Cochin Steel

- 9.7 D-KTC Fluid Control

- 9.8 Elmac Technologies

- 9.9 Emerson Electric

- 9.10 Essex Industries

- 9.11 Fidicon Devices

- 9.12 Groth Corporation

- 9.13 Kimray

- 9.14 L&J Technologies

- 9.15 Mott

- 9.16 Paradox IP

- 9.17 Parker Hannifin

- 9.18 Sunflow Technologies

- 9.19 The Protectoseal Company

- 9.20 WITT-GASETECHNIK

船用引擎框架減速器市場:按引擎類型、船舶類型、產品類型、材料和銷售管道,全球預測,2026-2032年

船用引擎框架減速器市場:按引擎類型、船舶類型、產品類型、材料和銷售管道,全球預測,2026-2032年 阻火器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按最終用戶、類型、地區和競爭格局分類,2021-2031年)

阻火器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按最終用戶、類型、地區和競爭格局分類,2021-2031年) 阻火器市場規模、佔有率及成長分析(按類型、應用、最終用戶和地區分類)-2026-2033年產業預測

阻火器市場規模、佔有率及成長分析(按類型、應用、最終用戶和地區分類)-2026-2033年產業預測 全球防火防爆設備市場:市場規模、佔有率、趨勢分析(按類型、最終用途和地區)、細分市場預測(2025-2030 年)消焰器市場規模、佔有率和趨勢分析報告:2024-2030 年按類型、應用、最終用途、地區和細分市場進行的預測

全球防火防爆設備市場:市場規模、佔有率、趨勢分析(按類型、最終用途和地區)、細分市場預測(2025-2030 年)消焰器市場規模、佔有率和趨勢分析報告:2024-2030 年按類型、應用、最終用途、地區和細分市場進行的預測