|

市場調查報告書

商品編碼

1859010

物流機器人市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Logistics Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

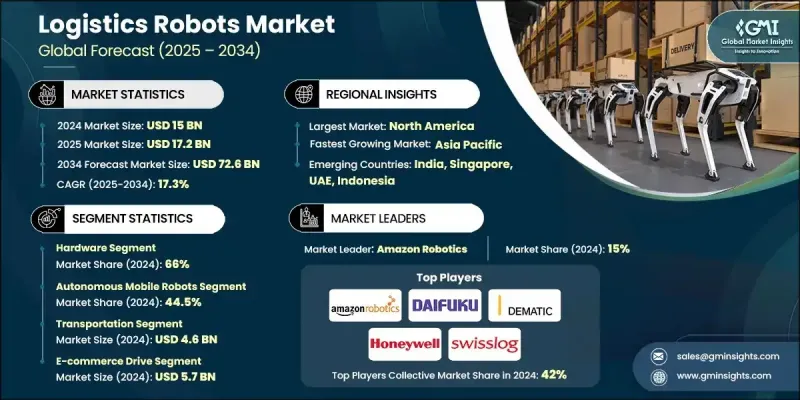

2024 年全球物流機器人市場價值為 150 億美元,預計到 2034 年將以 17.3% 的複合年成長率成長至 726 億美元。

物流行業正經歷快速變革,其發展動力源於對自動化日益成長的需求、更緊迫的交付週期以及先進的供應鏈數位化。該行業的核心在於其錯綜複雜的生態系統,其特點是地域聚集、戰略供應商關係以及強大的垂直整合。隨著機器人技術的日趨成熟,物流企業正逐步向自主系統轉型,以滿足不斷提升的消費者期望並降低營運效率。更快的投資報酬率和更短的投資回收期促使智慧機器人系統在倉庫和配送中心得到更廣泛的部署。這波自動化浪潮正在重塑物流基礎設施,實現更高的吞吐量、更精準的配送以及更少的人力依賴,最終推動已開發市場和新興市場的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 150億美元 |

| 預測值 | 726億美元 |

| 複合年成長率 | 17.3% |

2024年,硬體部分佔據了66%的市場佔有率,預計到2034年將以16.4%的複合年成長率成長。機器人平台、機械組件和移動系統構成了物流機器人解決方案的基礎層,使其能夠在倉庫和最後一公里配送環境中實現無縫運作。儘管人工參與物流營運仍然佔據總成本的很大一部分,但機器人動力系統的技術進步和研究舉措正在重塑硬體成本結構。

2024年,自主移動機器人(AMR)市佔率達到44.5%,預計2025年至2034年間將以17.9%的複合年成長率成長。由於採用了人工智慧、視覺SLAM和自適應感測器技術等先進的導航系統,AMR相比傳統的自動導引車(AGV)具有顯著的效率提升。這些功能使其能夠在複雜、動態的環境中進行即時決策,從而推動該領域從試點階段邁向大規模商業部署。

預計到2024年,美國物流機器人市場將佔據65%的佔有率,市場規模將達到46億美元。儘管與全球平均水平相比,美國物流機器人的滲透率相對較低,但勞動力短缺、技術成熟以及聯邦政府對自動化發展的支持,都為美國物流機器人市場的成長提供了有力支撐。完善的基礎設施和政府資助的創新項目持續鞏固美國在全球機器人領域的地位,為物流領域大規模應用機器人解決方案創造了有利環境。

塑造全球物流機器人市場競爭格局的關鍵產業參與者包括ABB、安川馬達、豐田/Bastian、歐姆龍、大福、亞馬遜機器人、庫卡/Swisslog、凱傲/德馬泰克、霍尼韋爾和AutoStore。為了鞏固自身地位,物流機器人公司正優先發展人工智慧驅動的自動化、即時資料分析以及針對不同物流應用場景量身定做的模組化系統設計。策略併購和合作促進了技術共享和地理擴張,而研發投入則催生了可擴展的多應用平台。領先企業也針對電子商務、第三方物流和零售倉儲環境客製化機器人集群,確保客戶的長期留存並提高營運投資報酬率。全球企業正透過在地化生產、擴展服務網路以及整合數位平台進一步加強其市場地位,這些平台能夠實現無縫的物流協調和預測性維護。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 自主移動機器人製造商

- 自動化儲存和檢索系統提供者

- 機器人軟體和人工智慧平台開發商

- 倉庫基礎設施及物料搬運設備供應商

- 系統整合商和解決方案提供商

- 成本結構

- 利潤率

- 每個階段的價值增加

- 影響供應鏈的因素

- 顛覆者

- 供應商格局

- 對力的影響

- 成長促進因素

- 電子商務領域揀貨應用的發展

- 機器人技術的進步

- 自動化倉庫日益普及

- 物流處理中對永續發展實踐的認知不斷提高

- 產業陷阱與挑戰

- 物流機器人的購置與實施成本高

- 員工缺乏操作和維護先進機器人系統的技能

- 市場機遇

- 人工智慧和物聯網在物流機器人的應用

- 協作機器人的應用

- 成長促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 電腦視覺與物體識別

- 預測分析與維護

- 多功能機器人開發

- 人機協作進展

- 新興技術

- 5G連接與通訊系統

- 數位孿生與仿真技術

- 區塊鏈與供應鏈透明度

- 永續性和綠色技術整合

- 目前技術

- 成長潛力分析

- 監管環境

- 聯邦安全標準框架

- ANSI/RIA R15.06 要求

- ANSI R15.08 移動機器人標準

- ISO 10218 全球協調

- OSHA合規要求

- 一般責任條款適用

- 機械及機械防護標準

- 電氣安全要求

- 行業特定監管要求

- FDA醫療保健法規

- 食品安全與HACCP合規性

- 汽車業標準

- 國際標準協調

- ISO技術委員會299

- 歐洲標準一體化

- 區域適應性要求

- 聯邦安全標準框架

- 成本細分分析

- 硬體成本組成部分

- 軟體及整合費用

- 基礎設施改造要求

- 維護和服務成本

- 波特的分析

- PESTEL 分析

- 永續性和環境方面

- 環境影響評估與生命週期分析

- 社會影響力與社區關係

- 公司治理與企業責任

- 永續技術發展

- 風險評估框架

- 互通性和標準化差距

- 遺留系統相容性挑戰

- 監理與合規風險

- 金融風險緩解策略

- 性能和品質標準

- 風險評估方法

- 準確度和精密度標準

- 行業特定品質要求

- 安全測試要求

- 用例

- 亞馬遜機器人實施模型

- 多SKU處理和排序

- 汽車製造一體化

- 醫療保健和製藥應用

- 第三方物流最佳化

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 機器人平台與底盤

- 感測器和感知系統

- 執行器和操控系統

- 其他

- 軟體

- 機器人作業系統

- 車隊管理軟體

- 倉庫管理整合

- 其他

- 服務

- 專業的

- 管理

第6章:市場估算與預測:依類型分類,2021-2034年

- 主要趨勢

- 自動導引車

- 自主移動機器人

- 機械手臂

- 其他

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 托盤化和拆托盤

- 揀選和放置

- 運輸

- 其他

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 電子商務

- 衛生保健

- 零售

- 食品和飲料

- 汽車

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球參與者

- ABB

- Amazon Robotics

- AutoStore

- Daifuku

- Honeywell

- KION/Dematic

- KUKA/Swisslog

- Omron

- Toyota/Bastian

- Yaskawa Electric

- 區域玩家

- Bastian Solutions

- Geek+

- GreyOrange

- Locus Robotics

- Vecna Robotics

- 新興玩家

- VisionNav Robotics

- Berkshire Grey

- Covariant

- Exotec

- River Systems

The Global Logistics Robots Market was valued at USD 15 billion in 2024 and is estimated to grow at a CAGR of 17.3% to reach USD 72.6 billion by 2034.

This sector is evolving rapidly, shaped by growing demand for automation, tighter delivery timelines, and advanced supply chain digitization. The industry is defined by its intricate ecosystem, which is marked by geographic clustering, strategic supplier relationships, and strong vertical integration. As robotics technologies mature, logistics firms are increasingly transitioning toward autonomous systems to meet rising consumer expectations and reduce operational inefficiencies. Accelerated ROI and shrinking payback windows are prompting broader deployment of intelligent robotics systems across warehouse and distribution centers. This wave of automation is reshaping logistics infrastructure by enabling higher throughput, improved accuracy, and leaner workforce dependencies, ultimately fueling growth across developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 17.3% |

In 2024, the hardware segment held a 66% share and is expected to grow at a CAGR of 16.4% through 2034. Robotic platforms, mechanical components, and mobility systems form the foundational layer of logistics robotics solutions, enabling seamless operation in warehouse and last-mile environments. Technological advancements and research initiatives into robotics power systems are reshaping the hardware cost structures, although human involvement in logistics operations still accounts for a large portion of total expenses.

The autonomous mobile robots (AMRs) segment held a 44.5% share in 2024 and is forecasted to grow at a CAGR of 17.9% between 2025 and 2034. AMRs offer significant efficiency gains over traditional automated guided vehicles due to advanced navigation systems powered by artificial intelligence, visual SLAM, and adaptive sensor technology. These capabilities allow for real-time decision-making in complex, dynamic environments, moving the segment from pilot phases into large-scale commercial deployments.

U.S. Logistics Robots Market held 65% share in 2024, generating USD 4.6 billion. Despite relatively low penetration compared to global benchmarks, growth in the U.S. is underpinned by labor shortages, technological readiness, and federal support for automation. Robust infrastructure and government-funded innovation programs continue to strengthen the country's position in the global robotics landscape, creating a favorable environment for the large-scale implementation of robotic solutions in logistics.

Key industry players shaping the competitive landscape of the Global Logistics Robots Market include ABB, Yaskawa Electric, Toyota/Bastian, Omron, Daifuku, Amazon Robotics, KUKA/Swisslog, KION/Dematic, Honeywell, and AutoStore. To reinforce their position, logistics robotics companies are prioritizing AI-powered automation, real-time data analytics, and modular system designs tailored to various logistics use cases. Strategic mergers and partnerships are enabling technology sharing and geographic expansion, while R&D investments are yielding scalable platforms for multi-application functionality. Leading firms are also customizing robotic fleets to suit e-commerce, third-party logistics, and retail warehouse environments, ensuring long-term client retention and improved operational ROI. Global players are further strengthening their presence through localized production, expanded service networks, and integrated digital platforms that enable seamless logistics orchestration and predictive maintenance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.6.1 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Autonomous mobile robot manufacturers

- 3.1.1.2 Automated storage and retrieval system providers

- 3.1.1.3 Robotics software & AI platform developers

- 3.1.1.4 Warehouse infrastructure & material handling equipment suppliers

- 3.1.1.5 Systems integrators & solution provider

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Developments in e-commerce sector for picking applications

- 3.2.1.2 Advancements in robotics technology

- 3.2.1.3 Increasing popularity of autonomous warehouses

- 3.2.1.4 Growing awareness towards sustainability practices in logistic handling

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of purchasing and implementing logistics robots

- 3.2.2.2 Lack of employee skills to operate and maintain advanced robotic systems

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and IoT in logistics robots

- 3.2.3.2 Adoption of collaborative robots

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Computer vision & object recognition

- 3.3.1.2 Predictive analytics & maintenance

- 3.3.1.3 Polyfunctional robot development

- 3.3.1.4 Human-robot collaboration advancement

- 3.3.2 Emerging technologies

- 3.3.2.1 5G connectivity & communication systems

- 3.3.2.2 Digital twin & simulation technologies

- 3.3.2.3 Blockchain & supply chain transparency

- 3.3.2.4 Sustainability & green technology integration

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 Federal safety standards framework

- 3.5.1.1 ANSI/RIA R15.06 requirements

- 3.5.1.2 ANSI R15.08 mobile robot standards

- 3.5.1.3 ISO 10218 global harmonization

- 3.5.2 OSHA compliance requirements

- 3.5.2.1 General duty clause application

- 3.5.2.2 Machinery & machine guarding standards

- 3.5.2.3 Electrical safety requirements

- 3.5.3 Industry-Specific Regulatory Requirements

- 3.5.3.1 FDA healthcare regulations

- 3.5.3.2 Food safety & HACCP compliance

- 3.5.3.3 Automotive industry standards

- 3.5.4 International standards harmonization

- 3.5.4.1 ISO technical committee 299

- 3.5.4.2 European standards integration

- 3.5.4.3 Regional adaptation requirements

- 3.5.1 Federal safety standards framework

- 3.6 Cost breakdown analysis

- 3.6.1 Hardware cost components

- 3.6.2 Software & integration expenses

- 3.6.3 Infrastructure modification requirements

- 3.6.4 Maintenance & service costs

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Environmental impact assessment & lifecycle analysis

- 3.9.2 Social impact & community relations

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable technological development

- 3.10 Risk assessment framework

- 3.10.1 Interoperability & standardization gaps

- 3.10.2 Legacy system compatibility challenges

- 3.10.3 Regulatory & compliance risks

- 3.10.4 Financial risk mitigation strategies

- 3.11 Performance & quality standards

- 3.11.1 Risk assessment methodologies

- 3.11.2 Accuracy & precision standards

- 3.11.3 Industry-specific quality requirements

- 3.11.4 Safety testing requirements

- 3.12 Use Cases

- 3.12.1 Amazon robotics implementation model

- 3.12.2 Multi-SKU handling & sorting

- 3.12.3 Automotive manufacturing integration

- 3.12.4 Healthcare & pharmaceutical applications

- 3.12.5 Third-party logistics optimization

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Robotic platforms & chassis

- 5.2.2 Sensors & perception systems

- 5.2.3 Actuators & manipulation systems

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Robot operating systems

- 5.3.2 Fleet management software

- 5.3.3 Warehouse management integration

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional

- 5.4.2 Managed

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn & Units)

- 6.1 Key trends

- 6.2 Automated guided vehicles

- 6.3 Autonomous mobile robots

- 6.4 Robot arms

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn & Units)

- 7.1 Key trends

- 7.2 Palletizing & de-palletizing

- 7.3 Pick & place

- 7.4 Transportation

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By End use, 2021 - 2034 ($Bn & Units)

- 8.1 Key trends

- 8.2 E-commerce

- 8.3 Healthcare

- 8.4 Retail

- 8.5 Food & beverages

- 8.6 Automotive

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn & Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 ABB

- 10.1.2 Amazon Robotics

- 10.1.3 AutoStore

- 10.1.4 Daifuku

- 10.1.5 Honeywell

- 10.1.6 KION/Dematic

- 10.1.7 KUKA/Swisslog

- 10.1.8 Omron

- 10.1.9 Toyota/Bastian

- 10.1.10 Yaskawa Electric

- 10.2 Regional players

- 10.2.1 Bastian Solutions

- 10.2.2 Geek+

- 10.2.3 GreyOrange

- 10.2.4 Locus Robotics

- 10.2.5 Vecna Robotics

- 10.3 Emerging players

- 10.3.1 VisionNav Robotics

- 10.3.2 Berkshire Grey

- 10.3.3 Covariant

- 10.3.4 Exotec

- 10.3.5 River Systems

物流機器人市場:機器人類型、功能、負載容量、動力來源、應用及最終用途-2026-2032年全球市場預測托盤轉移模組市場:按類型、應用、終端用戶產業、自動化程度、負載能力和分銷管道分類-全球預測,2026-2032年

物流機器人市場:機器人類型、功能、負載容量、動力來源、應用及最終用途-2026-2032年全球市場預測托盤轉移模組市場:按類型、應用、終端用戶產業、自動化程度、負載能力和分銷管道分類-全球預測,2026-2032年 自動瓦楞紙板組裝機市場機會、成長要素、產業趨勢分析及2026年至2035年預測。

自動瓦楞紙板組裝機市場機會、成長要素、產業趨勢分析及2026年至2035年預測。 全球箱體安裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球自動化瓦楞紙板組裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球箱體安裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球自動化瓦楞紙板組裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034) 物流機器人市場:依組件、產業、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

物流機器人市場:依組件、產業、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 2026年全球自動化紙箱組裝機市場報告2026年全球碼垛機器人市場報告全球自動化紙箱組裝機市場(按控制類型、包裝材料、自動化程度、機器類型、產量和最終用戶產業分類)預測(2026-2032)按有效載荷能力、機器人類型、安裝類型、控制類型、連接方式和應用分類的碼垛機械臂市場,全球預測,2026-2032年

2026年全球自動化紙箱組裝機市場報告2026年全球碼垛機器人市場報告全球自動化紙箱組裝機市場(按控制類型、包裝材料、自動化程度、機器類型、產量和最終用戶產業分類)預測(2026-2032)按有效載荷能力、機器人類型、安裝類型、控制類型、連接方式和應用分類的碼垛機械臂市場,全球預測,2026-2032年