|

市場調查報告書

商品編碼

1858983

腦磁圖市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Magnetoencephalography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

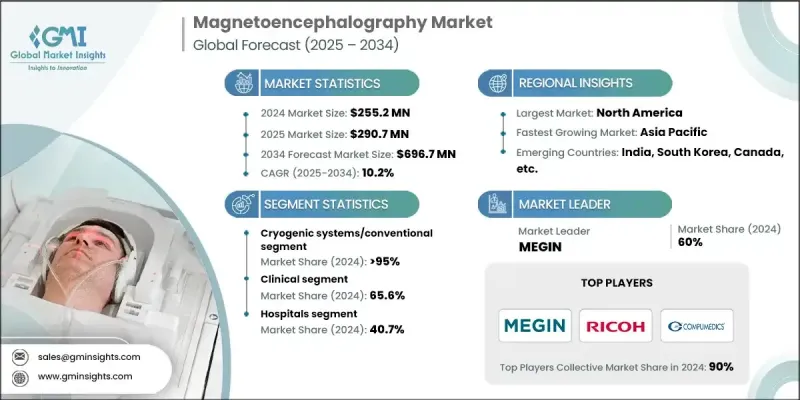

2024 年全球腦磁圖市場價值為 2.552 億美元,預計到 2034 年將以 10.2% 的複合年成長率成長至 6.967 億美元。

由於神經系統疾病發病率上升、人口老化以及對先進診斷工具的依賴性增強,腦磁圖(MEG)的需求正在加速成長。臨床和研究機構擴大採用MEG來提高神經系統評估的精確度和速度。該技術能夠即時追蹤腦部活動,這在癲癇、阿茲海默症和帕金森氏症等疾病的診斷和治療中發揮著至關重要的作用。除了臨床應用外,MEG系統在腦功能研究、精神病學評估和神經發育研究等領域也得到了更廣泛的應用。技術進步和對腦部網路連結的更深入理解不斷推動醫療保健生態系統的創新和整合。由於醫療基礎設施的完善和對神經科學計畫的資金支持,已開發地區的MEG應用尤為顯著。製造商正致力於透過改進分銷策略和降低成本來擴大MEG系統的普及範圍,尤其是在新興市場。個人化治療和早期診斷的趨勢預計將進一步推動全球對腦磁圖系統的長期市場需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.552億美元 |

| 預測值 | 6.967億美元 |

| 複合年成長率 | 10.2% |

到2034年,光泵磁力計(OPM)系統市場將以24.9%的複合年成長率成長,成為神經影像領域的變革性進步。這些系統採用光泵磁力計,可在室溫下高效運行,無需複雜的低溫組件。其緊湊的穿戴式設計允許感測器直接放置在頭皮上,從而提高空間解析度並實現自然運動過程中的資料收集。基於OPM的腦磁圖(MEG)系統具有靈活性、更低的營運成本和更強的實際應用適應性,使其在兒科和動態監測領域特別引人注目。其可擴展性和便攜性正日益受到臨床和神經科學研究中心的青睞。

2024年,臨床應用領域佔了65.6%的市佔率。神經系統疾病患者群體的不斷成長,以及對早期診斷日益重視,共同促成了該領域的領先地位。 MEG透過精確定位異常腦活動,在術前定位和疾病管理中發揮關鍵作用。其非侵入性和高解析度的特性使其在癲癇、腫瘤和神經退化性疾病的治療中特別有用,因為在這些疾病中,精確定位對於手術計劃和患者預後至關重要。

2024年,北美腦磁圖(MEG)市佔率達39.5%。該地區受益於強大的醫學研究基礎、廣泛的醫療保健服務以及腦部疾病患者數量的不斷成長。 MEG早期在臨床上的應用以及與醫院實踐的整合,促進了其在診斷領域的應用。區域政府也發揮了重要作用,資助神經科學計畫並支持腦圖譜研究計畫。這些因素使北美在MEG系統的技術部署和臨床應用方面均處於領先地位。

全球腦磁圖(MEG)市場的主要活躍企業包括FieldLine Inc.、理光(Ricoh)、Cerca Magnetics Limited、Compumedics Limited、MAG4Health、MEGIN和CTF MEG NEURO INNOVATIONS, INC.。腦磁圖領域的企業正透過對研發的策略投資和全球擴張來鞏固其市場地位。創新仍然是核心,重點在於開發下一代MEG系統,例如基於光功率管理(OPM)的解決方案,以增強移動性和可及性。各公司正透過瞄準新興市場並改善服務基礎設施來拓展地理範圍。與研究機構和醫院的合作有助於加速臨床驗證和產品應用。此外,各公司也在努力簡化系統整合並降低操作複雜性,使MEG更適用於常規臨床應用。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 神經系統疾病盛行率不斷上升

- 腦磁圖領域的技術快速發展

- 在臨床診斷和研究領域的應用日益廣泛

- 產業陷阱與挑戰

- 替代神經影像技術的可用性

- 腦磁圖系統成本高昂

- 機會

- 攜帶式和穿戴式式腦磁圖系統

- 人工智慧整合與自動化分析

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 技術路線圖與創新格局

- SQUID技術演進

- OPM技術進步

- 量子感測器開發

- AI/ML整合時間表

- 2024年各地區定價分析

- MEG 相對於 fMRI 和 EEG 的優勢

- 管道分析

- 全球MEG裝置數量,按地區和國家分類

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 亞太地區

- 中國

- 日本

- 北美洲

- 品牌分析

- 報銷方案

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀錶板

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 低溫系統/常規

- OPM系統

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 臨床

- 癲癇

- 自閉症

- 失智

- 中風

- 創傷性腦損傷(TBI)

- 其他應用

- 研究

第7章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院

- 影像中心

- 學術和研究機構

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 亞太地區

- 中國

- 日本

- 世界其他地區(RoW)

第9章:公司簡介

- Cerca Magnetics Limited

- Compumedics Limited

- CTF MEG NEURO INNOVATIONS, INC.

- FieldLine Inc.

- MAG4Health

- MEGIN

- Ricoh

The Global Magnetoencephalography Market was valued at USD 255.2 million in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 696.7 million by 2034.

The demand for magnetoencephalography (MEG) is accelerating due to rising incidences of neurological disorders, an aging population, and increased reliance on advanced diagnostic tools. Clinical and research institutions are increasingly adopting MEG to enhance the precision and speed of neurological assessments. The technology's ability to deliver real-time tracking of brain activity is proving vital in the diagnosis and management of conditions like epilepsy, Alzheimer's disease, and Parkinson's disease. In addition to clinical use, MEG systems are seeing broader application in brain function research, psychiatric evaluation, and neurodevelopmental studies. Technological progress and a deeper understanding of brain network connectivity continue to drive innovation and integration across healthcare ecosystems. Strong adoption is especially noted in developed regions due to improved healthcare infrastructure and supportive funding for neuroscience initiatives. Manufacturers are working on expanding access to MEG systems through enhanced distribution strategies and lower-cost models, particularly in emerging markets. The rising trend toward personalized treatment and early-stage diagnosis is further expected to fuel long-term market demand for magnetoencephalography systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $255.2 Million |

| Forecast Value | $696.7 Million |

| CAGR | 10.2% |

The OPM systems segment will grow at a CAGR of 24.9% through 2034, establishing itself as a transformative advancement in neuroimaging. These systems are built using optically pumped magnetometers, which operate efficiently at room temperature, eliminating the need for complex cryogenic components. Their compact, wearable format allows sensors to be positioned directly on the scalp, enhancing spatial resolution and enabling data capture during natural movements. The flexibility, lower operational costs, and real-world adaptability of OPM-based MEG systems have made them especially attractive for pediatric use and ambulatory monitoring. Their scalability and portability continue to gain traction across both clinical settings and neuroscience research centers.

In 2024, the clinical segment held a 65.6% share. The growing patient base suffering from neurological disorders, combined with increasing emphasis on early-stage diagnostics, is contributing to the segment's dominance. MEG plays a key role in presurgical mapping and disease management by precisely localizing abnormal brain activity. Its non-invasive and high-resolution capability makes it particularly useful in treating epilepsy, tumors, and degenerative neurological diseases, where accurate mapping is crucial for surgical planning and patient outcomes.

North America Magnetoencephalography Market held 39.5% share in 2024. The region benefits from a strong foundation in medical research, widespread healthcare access, and increasing patient numbers diagnosed with brain-related conditions. Early clinical adoption and integration of MEG into hospital practices have helped expand its application in diagnostics. Regional governments have also played a significant role by funding neuroscience projects and supporting brain mapping research initiatives. These factors have positioned North America as a frontrunner in both technology deployment and clinical outcomes using MEG systems.

Key companies active in the Global Magnetoencephalography Market include FieldLine Inc., Ricoh, Cerca Magnetics Limited, Compumedics Limited, MAG4Health, MEGIN, and CTF MEG NEURO INNOVATIONS, INC. Companies in the magnetoencephalography space are strengthening their market positions through strategic investments in R&D and global expansion. Innovation remains central, with a focus on next-generation MEG systems like OPM-based solutions that enhance mobility and accessibility. Firms are expanding geographically by targeting installations in emerging markets and improving service infrastructure. Collaborations with research institutions and hospitals are helping accelerate clinical validation and product adoption. Additionally, efforts are being made to simplify system integration and reduce operational complexity, making MEG more viable for routine clinical use.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of neurological disorders

- 3.2.1.2 Rapid technology advancements in the field of magnetoencephalography

- 3.2.1.3 Growing applications in clinical diagnosis and research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative neuroimaging technologies

- 3.2.2.2 High cost of magnetoencephalography systems

- 3.2.3 Opportunities

- 3.2.3.1 Portable & wearable MEG systems

- 3.2.3.2 AI integration & automated analysis

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology roadmap & innovation landscape

- 3.5.1 SQUID technology evolution

- 3.5.2 OPM technology advancement

- 3.5.3 Quantum sensor development

- 3.5.4 AI/ML integration timeline

- 3.6 Pricing analysis, by region, 2024

- 3.7 Advantages of MEG over fMRI and EEG

- 3.8 Pipeline analysis

- 3.9 Worldwide MEG installations, by region and country

- 3.9.1 North America

- 3.9.1.1 U.S.

- 3.9.1.2 Canada

- 3.9.2 Europe

- 3.9.2.1 Germany

- 3.9.2.2 UK

- 3.9.2.3 France

- 3.9.3 Asia Pacific

- 3.9.3.1 China

- 3.9.3.2 Japan

- 3.9.1 North America

- 3.10 Brand analysis

- 3.11 Reimbursement scenario

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Future market trends

- 3.15 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Cryogenic systems/Conventional

- 5.3 OPM systems

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical

- 6.2.1 Epilepsy

- 6.2.2 Autism

- 6.2.3 Dementia

- 6.2.4 Stroke

- 6.2.5 Traumatic brain injury (TBI)

- 6.2.6 Other applications

- 6.3 Research

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Imaging centres

- 7.4 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.5 Rest of the world (RoW)

Chapter 9 Company Profiles

- 9.1 Cerca Magnetics Limited

- 9.2 Compumedics Limited

- 9.3 CTF MEG NEURO INNOVATIONS, INC.

- 9.4 FieldLine Inc.

- 9.5 MAG4Health

- 9.6 MEGIN

- 9.7 Ricoh