|

市場調查報告書

商品編碼

1858974

罐裝酒精飲料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Canned Alcoholic Beverages Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球罐裝酒精飲料市場價值 712 億美元,預計到 2034 年將以 13.2% 的複合年成長率成長至 2,455 億美元。

罐裝酒精飲料市場成長的驅動力在於其便利性、易攜帶性以及在現代消費者中日益成長的吸引力。這些產品適用於各種場合,包括社交聚會、節日慶典、戶外活動和日常飲酒。罐裝酒精飲料,例如雞尾酒、葡萄酒、啤酒和硬蘇打水,能夠滿足不同消費者的偏好,尤其在玻璃包裝不便或受限的場所,例如海灘、公園和音樂會,更受青睞。電子商務和數位行銷平台的興起也促進了市場成長,使這些產品更容易取得和推廣。隨著口味、品牌和包裝方面的不斷創新,罐裝酒精飲料行業預計將在未來幾年繼續擴張和多元化發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 712億美元 |

| 預測值 | 2455億美元 |

| 複合年成長率 | 13.2% |

2024年,罐裝烈酒飲料市場規模達到467億美元,預計到2034年將達到1,571億美元,複合年成長率(CAGR)為12.9%。此品類已快速崛起,成為全球即飲(RTD)酒精飲料市場中最具活力且高收入的細分市場之一。其成長得益於持續的創新和產品高階化。諸如Tanqueray & Tonic RTD、Cutwater Spirits和On the Rocks等知名品牌,透過便利的罐裝形式,提供複雜而媲美酒吧品質的雞尾酒,提升了消費者的期望值。與麥芽或葡萄酒基飲料不同,即飲烈酒飲料的優點在於能夠完美還原龍舌蘭、伏特加或蘭姆酒等烈酒的真實風味,並以專業調配雞尾酒的真實比例進行混合。

到2024年,非現場銷售管道將佔據50%的市場。這一主導地位源自於該通路的便利性和易得性,尤其是在疫情後消費者行為轉向居家消費和社交活動更加放鬆的情況下。酒類專賣店、連鎖超市和便利商店等零售商透過大包裝折扣和新口味的推出來提升性價比,從而鼓勵消費者嘗試購買和發現新品牌。季節性新品和地區性產品也促進了忠實消費者的重複購買行為。

2024年,美國罐裝酒精飲料市場規模達259億美元,預估年複合成長率(CAGR)為9.9%。美國市場對罐裝酒精飲料的需求居高不下,這主要得益於消費者對即飲型(RTD)飲料的偏好以及美國蓬勃發展的精釀飲料產業。罐裝飲料的便攜性和易飲性使其越來越受歡迎,尤其是在戶外環境中,這進一步推動了市場成長。

全球罐裝酒精飲料市場的主要參與者包括Cutwater Spirits、Boston Beer Company、喜力(Heineken NV)、嘉士伯集團(Carlsberg Group)、星座集團(Constellation Brands)、摩森康勝飲料公司(Molson Coors Beverage Company)、帝亞吉歐(Diage Brand plc. Holdings)和百威英博(Anheuser-Busch InBev)。罐裝酒精飲料市場的企業正致力於創新、高階化和市場擴張,以增強其競爭優勢。帝亞吉歐、Boston Beer Company和星座集團等領先企業正在推出多樣化的口味和以烈酒為主的配方,以滿足不斷變化的消費者口味偏好。與酒吧、餐廳和電商平台建立策略合作夥伴關係有助於擴大分銷管道。此外,對永續包裝、區域產品在地化和數位行銷活動的投資也提升了品牌知名度。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 按酒精含量

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計

- 主要進口國

- 主要出口國

(註:貿易統計僅針對重點國家提供)

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 麥芽罐裝飲料

- 傳統啤酒(拉格啤酒、艾爾啤酒、黑啤酒)

- 風味麥芽飲料(FMBS)

- 麥芽硬蘇打水

- 葡萄酒罐裝飲料

- 罐裝靜止葡萄酒

- 葡萄酒蘇打水和冰鎮飲料

- 水果口味硬蘇打水

- 罐裝烈酒飲料

- 現調雞尾酒

- 罐裝長飲

- 高級罐裝雞尾酒

- 特色罐裝酒精飲料

- 硬茶

- 硬咖啡

- 硬康普茶

第6章:市場估計與預測:依酒精含量分類,2021-2034年

- 主要趨勢

- 無酒精產品(酒精濃度0.05% - 0.5%)

- 低酒精產品(酒精濃度:0.5% - 3.0%)

- 標準酒精飲料(酒精濃度 3.0% - 8.0%)

- 高酒精含量產品(>8.0% ABV)

第7章:市場估計與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 本地通路

- 酒吧和酒館

- 餐廳及餐飲服務

- 娛樂場所

- 飯店及餐飲業

- 非現場管道

- 雜貨店

- 便利商店

- 酒類商店和專賣店

- 啤酒經銷商

- 控制狀態通道

- 直接面對消費者(DTC)

- 電子商務與數位管道

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Anheuser-Busch InBev

- Arbor Brewing Company India

- Asahi Group Holdings

- Barnstormer Brewing & Distilling Co.

- Boston Beer Company

- Carlsberg Group

- Cervejaria Cathedral

- Cervejaria Tarantino

- Cloudburst Brewing

- Constellation Brands

- Cutwater Spirits

- Diageo plc

- Fat Bottom Brewing

- Founders Brewing Co.

- Four Mile Brewing

- Goose Island Beer Company

- Heineken NV

- Lagunitas Brewing Company

- Molson Coors Beverage Company

- Parrotdog

- Purity Brewing Co

- Stone Brewing

- Thorn Brewing Co.

- Truly Hard Seltzer (Boston Beer)

- White Claw (Mark Anthony Brands)

- Others

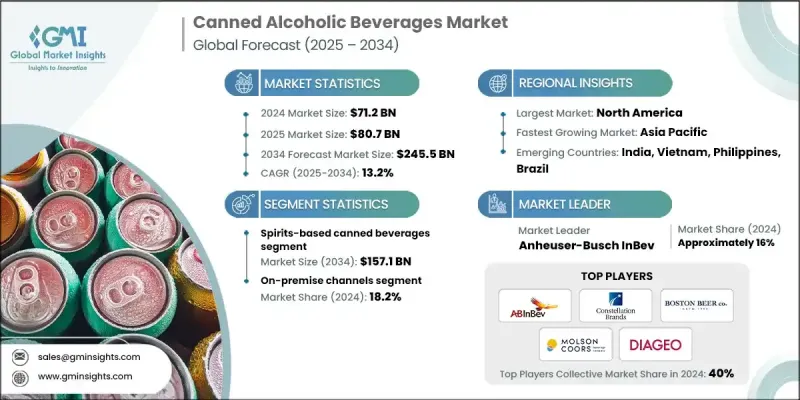

The Global Canned Alcoholic Beverages Market was worth USD 71.2 billion in 2024 and is estimated to grow at a CAGR of 13.2% to reach USD 245.5 billion by 2034.

The market growth is fueled by the convenience, transportability, and rising appeal of canned alcoholic beverages among modern consumers. These products are popular for a wide range of occasions, including social gatherings, festivals, outdoor events, and casual drinking. Canned alcoholic beverages, such as cocktails, wine, beer, and hard seltzers, cater to diverse consumer preferences and are especially favored in places where glass packaging is impractical or restricted, like beaches, parks, and concerts. The rise of e-commerce and digital marketing platforms has also contributed to the market's growth by making these products more accessible and easier to promote. With ongoing innovations in flavors, branding, and packaging, the canned alcoholic beverages industry is poised for continued expansion and diversification in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $71.2 Billion |

| Forecast Value | $245.5 Billion |

| CAGR | 13.2% |

The spirits-based canned beverages segment generated USD 46.7 billion in 2024 and is estimated to reach USD 157.1 billion by 2034, at a CAGR of 12.9%. This category has rapidly emerged as one of the most dynamic and high-revenue segments in the global ready-to-drink (RTD) alcoholic beverages landscape. Its growth is fueled by continued innovation and the premiumization of products. Major brands such as Tanqueray & Tonic RTD, Cutwater Spirits, and On the Rocks have elevated consumer expectations by delivering complex, bar-quality cocktails in convenient canned formats. Unlike malt- or wine-based alternatives, spirit-based RTD beverages stand out for their ability to replicate true spirit flavor profiles, such as tequila, vodka, or rum, mixed in authentic proportions that mirror professionally crafted cocktails.

The off-premise channel held a 50% share in 2024. This dominance stems from the channel's accessibility and convenience, especially as consumer behaviors shifted post-pandemic toward at-home consumption and relaxed social settings. Retailers like liquor stores, grocery chains, and convenience shops offer value through bulk-pack discounts and new flavor availability, which has encouraged trial purchases and brand discovery. Seasonal releases and region-specific product variations also drive repeat buying behavior among loyal consumers.

U.S. Canned Alcoholic Beverages Market reached USD 25.9 billion in 2024 and is projected to grow at a CAGR of 9.9%. The U.S. market leads in demand for canned alcoholic drinks, driven by consumer preferences for ready-to-drink (RTD) beverages and the country's robust craft beverage scene. The portability and ease of consumption of canned formats make them increasingly popular, particularly in outdoor environments, further fueling the market's growth.

Key players in the Global Canned Alcoholic Beverages Market are Cutwater Spirits, Boston Beer Company, Heineken N.V., Carlsberg Group, Constellation Brands, Molson Coors Beverage Company, Diageo plc, White Claw (Mark Anthony Brands), Asahi Group Holdings, and Anheuser-Busch InBev. Companies in the Canned Alcoholic Beverages Market are focusing on innovation, premiumization, and market expansion to strengthen their competitive edge. Leading players such as Diageo plc, Boston Beer Company, and Constellation Brands are introducing diverse flavor profiles and spirit-forward formulations to cater to evolving taste preferences. Strategic partnerships with bars, restaurants, and e-commerce platforms are helping boost distribution. Additionally, investments in sustainable packaging, regional product localization, and digital marketing campaigns are enhancing brand visibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Alcohol content

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.7.3 By alcohol content

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

( Note: the trade statistics will be provided for key countries only)

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Liters)

- 5.1 Key trends

- 5.2 Malt-based canned beverages

- 5.2.1 Traditional beer (lagers, ales, stouts)

- 5.2.2 Flavored malt beverages (FMBS)

- 5.2.3 Malt-based hard seltzers

- 5.3 Wine-based canned beverages

- 5.3.1 Canned still wine

- 5.3.2 Wine spritzers & coolers

- 5.3.3 Fruit-based hard seltzers

- 5.4 Spirits-based canned beverages

- 5.4.1 Rtd cocktails

- 5.4.2 Canned long drinks

- 5.4.3 Premium canned cocktails

- 5.5 Specialty canned alcoholic beverages

- 5.5.1 Hard tea

- 5.5.2 Hard coffee

- 5.5.3 Hard kombucha

Chapter 6 Market Estimates and Forecast, By Alcohol Content, 2021 - 2034 (USD Billion) (Liters)

- 6.1 Key trends

- 6.2 No-alcohol products (0.05% - 0.5% ABV)

- 6.3 Low-alcohol products (>0.5% - 3.0% ABV)

- 6.4 Standard-alcohol products (3.0% - 8.0% ABV)

- 6.5 High-alcohol products (>8.0% ABV)

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Liters)

- 7.1 Key trends

- 7.2 On-premise channels

- 7.2.1 Bars & taverns

- 7.2.2 Restaurants & food service

- 7.2.3 Entertainment venues

- 7.2.4 Hotels & hospitality

- 7.3 Off-premise channels

- 7.3.1 Grocery stores

- 7.3.2 Convenience stores

- 7.3.3 Liquor stores & specialty retail

- 7.3.4 Beer distributors

- 7.4 Control state channels

- 7.5 Direct-to-consumer (DTC)

- 7.6 E-commerce & digital channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Liters)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Anheuser-Busch InBev

- 9.2 Arbor Brewing Company India

- 9.3 Asahi Group Holdings

- 9.4 Barnstormer Brewing & Distilling Co.

- 9.5 Boston Beer Company

- 9.6 Carlsberg Group

- 9.7 Cervejaria Cathedral

- 9.8 Cervejaria Tarantino

- 9.9 Cloudburst Brewing

- 9.10 Constellation Brands

- 9.11 Cutwater Spirits

- 9.12 Diageo plc

- 9.13 Fat Bottom Brewing

- 9.14 Founders Brewing Co.

- 9.15 Four Mile Brewing

- 9.16 Goose Island Beer Company

- 9.17 Heineken N.V.

- 9.18 Lagunitas Brewing Company

- 9.19 Molson Coors Beverage Company

- 9.20 Parrotdog

- 9.21 Purity Brewing Co

- 9.22 Stone Brewing

- 9.23 Thorn Brewing Co.

- 9.24 Truly Hard Seltzer (Boston Beer)

- 9.25 White Claw (Mark Anthony Brands)

- 9.26 Others

罐裝酒精飲料市場報告:趨勢、預測和競爭分析(至2035年)

罐裝酒精飲料市場報告:趨勢、預測和競爭分析(至2035年) 罐裝酒精飲料市場分析及預測(至2035年):依類型、產品類型、應用、最終用戶、包裝、形式、通路、技術、材料類型及口味概況分類

罐裝酒精飲料市場分析及預測(至2035年):依類型、產品類型、應用、最終用戶、包裝、形式、通路、技術、材料類型及口味概況分類 罐裝酒精飲料市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測全球罐裝酒精飲料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

罐裝酒精飲料市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測全球罐裝酒精飲料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 瓶裝雞尾酒市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、主要成分、分銷管道、地區和競爭格局分類,2021-2031年

瓶裝雞尾酒市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、主要成分、分銷管道、地區和競爭格局分類,2021-2031年 罐裝酒精飲料市場規模、佔有率及成長分析(依產品類型、包裝類型、通路、口味及地區分類)-2026-2033年產業預測

罐裝酒精飲料市場規模、佔有率及成長分析(依產品類型、包裝類型、通路、口味及地區分類)-2026-2033年產業預測 全球罐裝酒精飲料市場全球瓶裝雞尾酒市場

全球罐裝酒精飲料市場全球瓶裝雞尾酒市場 罐裝酒精飲料市場(按產品、通路和地區分類)罐裝酒精飲料市場:2033 年市場分析與預測 - 按類型、產品、技術、成分、應用、形式、材料類型、最終用戶、功能

罐裝酒精飲料市場(按產品、通路和地區分類)罐裝酒精飲料市場:2033 年市場分析與預測 - 按類型、產品、技術、成分、應用、形式、材料類型、最終用戶、功能