|

市場調查報告書

商品編碼

1858970

神經刺激設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Neurostimulation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

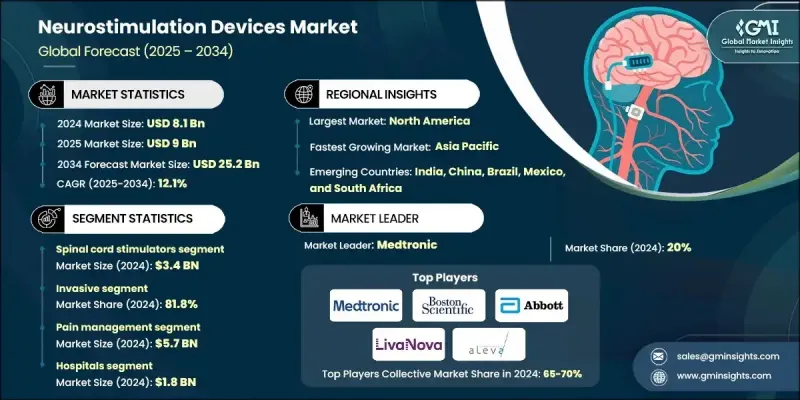

2024 年全球神經刺激設備市場價值為 81 億美元,預計到 2034 年將以 12.1% 的複合年成長率成長至 252 億美元。

受微創手術需求不斷成長(尤其是在已開發地區)以及神經系統疾病盛行率日益上升的推動,該市場正快速發展。帕金森氏症、癲癇、慢性疼痛和其他神經系統疾病老年患者數量的激增,顯著推動了對神經刺激設備的需求。這些技術為傳統療法提供了標靶性強且對患者友好的替代方案,符合人們對可擴展且高效療法的日益成長的需求。神經刺激技術的進步也提高了植入式和非侵入式設備的安全性、有效性和精確性,使其備受醫療服務提供者和患者的青睞。研發投入的增加和數位平台的整合進一步推動了市場發展,實現了即時資料追蹤和治療方案的個人化客製化。隨著醫療系統不斷優先考慮慢性神經系統疾病的個人化和長期管理,神經刺激設備正成為現代臨床實踐的重要組成部分,也是醫療器材領域的關鍵成長驅動力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 81億美元 |

| 預測值 | 252億美元 |

| 複合年成長率 | 12.1% |

神經刺激裝置是一種專門設計的系統,旨在向特定神經或神經系統區域發送電訊號。這些訊號有助於控制症狀,改善多種疾病患者的治療效果,包括憂鬱症、運動障礙和難治性慢性疼痛。根據所治療的疾病,神經刺激裝置可以戴在身上,也可以透過手術植入。

2024年,脊髓刺激器市場規模達34億美元。這些植入式設備透過向脊髓輸送微弱的電脈衝來阻斷疼痛訊號,對那些對標準療法無效的慢性疼痛患者非常有效。深部腦部刺激也發揮著至關重要的作用,它利用策略性地植入腦電極來調節異常的神經活動。

2024年,侵入性治療市佔率達81.8%。迷走神經刺激器、脊髓刺激器和深部腦部刺激器等侵入性設備因其在治療慢性神經系統疾病方面的高效性而持續受到關注。基於臨床成功和長期安全性資料,這些設備通常被認為是目前最可靠的治療選擇。其日益普及反映了臨床醫師在治療難治性神經系統疾病時,更傾向於選擇經過驗證、實證有效的技術。

預計到2024年,北美神經刺激設備市佔率將達到41.2%。神經系統疾病盛行率的上升以及人口老化,鞏固了該地區強勁的市場地位。憑藉日益普及的先進醫療保健服務、對醫療技術的大力投資以及對創新療法的早期應用,北美已成為全球神經刺激設備研發和應用的中心。

推動全球神經刺激設備市場發展的關鍵企業包括雅培實驗室、美敦力、Innovative Health Solutions、Laborie、Aleva Neurotherapeutics、Synapse Biomedical、LivaNova、BioControl Medical、Endostim、ElectroCore、MicroTransponder、Neuronetics、RS Medical、tVNS Technologies Technologies Technologies (Cerbomed)、波士頓和波士頓 (Helb)、科學和波士頓 (Cerlingmedas)。這些企業正積極實施一系列策略以鞏固其市場地位。大多數企業都在大力投資研發,以開發精度更高、體積更小、電池續航力更長的設備。透過策略性併購以及與醫療機構和研究機構建立合作關係,這些企業正在拓展其全球業務,並加速產品創新。各公司致力於推出以患者為中心的設備,這些設備整合了數位平台,可實現遠端監測和即時調整。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 已開發國家對微創手術的需求日益成長

- 神經系統疾病盛行率不斷上升

- 神經刺激裝置的技術進步

- 患有神經系統疾病的老年患者數量不斷增加

- 全球各地公司和組織的投資

- 產業陷阱與挑戰

- 神經刺激裝置相關併發症

- 缺乏熟練的醫護人員

- 市場機遇

- 與數位醫療和人工智慧的融合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 技術格局

- 未來市場趨勢

- 差距分析

- 定價分析

- 報銷方案

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略儀錶板

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- 脊髓刺激器

- 深部腦部刺激器

- 薦神經刺激器

- 迷走神經刺激器

- 胃電刺激器

- 經皮神經電刺激(TENS)

- 其他產品

第6章:市場估算與預測:依類型分類,2021-2034年

- 主要趨勢

- 入侵性

- 非侵入性

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 疼痛管理

- 尿失禁和糞便失禁

- 帕金森氏症

- 癲癇

- 原發性震顫

- 胃輕癱

- 沮喪

- 肌張力失調

- 其他應用

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院

- 門診手術中心

- 專科診所

- 其他用途

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abbott Laboratories

- Aleva Neurotherapeutics

- BioControl Medical

- Boston Scientific

- ElectroCore

- Endostim

- Helbling Holding

- Innovative Health Solutions

- Laborie

- LivaNova

- Medtronic

- MicroTransponder

- Neuronetics

- Parasym

- RS Medical

- Synapse Biomedical

- tVNS Technologies (Cerbomed)

The Global Neurostimulation Devices Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 12.1% to reach USD 25.2 billion by 2034.

This market is advancing rapidly, fueled by the rising need for minimally invasive procedures, especially in developed regions, and the increasing prevalence of neurological disorders. A surge in elderly patients suffering from Parkinson's disease, epilepsy, chronic pain, and other neurological conditions is significantly driving demand for neurostimulation devices. These technologies provide targeted and patient-friendly alternatives to traditional treatments, aligning with the growing demand for scalable and effective therapies. Advancements in neurostimulation technology have also enhanced the safety, efficacy, and precision of both implantable and non-invasive devices, making them highly desirable for both healthcare providers and patients. The market is further supported by increased R&D efforts and the integration of digital platforms, enabling real-time data tracking and therapy customization. As healthcare systems continue prioritizing personalized and long-term management of chronic neurological conditions, neurostimulation devices are becoming a vital part of modern clinical practice and a key growth driver in the medical device landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $25.2 Billion |

| CAGR | 12.1% |

Neurostimulation devices are specialized systems designed to send electrical signals to specific nerves or regions of the nervous system. These signals help control symptoms and improve patient outcomes across a range of conditions, including depression, movement disorders, and treatment-resistant chronic pain. They are either externally worn or surgically implanted, depending on the condition being treated.

The spinal cord stimulators segment generated USD 3.4 billion in 2024. These implantable devices block pain signals by delivering mild electrical pulses to the spinal cord, proving highly effective in patients with chronic pain who do not respond to standard treatments. Deep brain stimulation also plays a crucial role by regulating abnormal neural activity using strategically placed brain electrodes.

The invasive segment held an 81.8% share in 2024. Invasive devices such as vagus nerve stimulators, spinal cord stimulators, and deep brain stimulators continue to gain traction due to their high efficacy in treating chronic neurological conditions. These devices are often regarded as the most reliable therapeutic option based on clinical success and long-standing safety data. Their growing adoption reflects a preference among clinicians for proven, evidence-based technologies in managing refractory neurological diseases.

North America Neurostimulation Devices Market held a 41.2% share in 2024. Rising neurological disease prevalence, coupled with an aging population, underpins the region's strong market position. With increased access to advanced healthcare, robust investment in medical technology, and early adoption of innovative therapies, North America is positioned as a global hub for neurostimulation device development and adoption.

Key companies driving the Global Neurostimulation Devices Market include Abbott Laboratories, Medtronic, Innovative Health Solutions, Laborie, Aleva Neurotherapeutics, Synapse Biomedical, LivaNova, BioControl Medical, Endostim, ElectroCore, MicroTransponder, Neuronetics, RS Medical, tVNS Technologies (Cerbomed), Helbling Holding, Boston Scientific, and Parasym. Companies operating in the Neurostimulation Devices Market are implementing a range of strategies to strengthen their market position. Most are heavily investing in R&D to develop devices with enhanced precision, smaller form factors, and improved battery life. Strategic mergers, acquisitions, and partnerships with healthcare providers and research institutions are expanding their global reach and accelerating product innovation. Firms are focusing on launching patient-centric devices with integrated digital platforms that allow remote monitoring and real-time adjustments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Type

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgery in developed countries

- 3.2.1.2 Increasing prevalence of neurological disorders

- 3.2.1.3 Technological advancements in neurostimulation devices

- 3.2.1.4 Increasing number of elderly patients with neurological disorders

- 3.2.1.5 Investments by companies and organizations across the globe

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications associated with neurostimulation devices

- 3.2.2.2 Lack of skilled healthcare practitioners

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with digital health and AI

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Pricing analysis

- 3.9 Reimbursement scenario

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spinal cord stimulator

- 5.3 Deep brain stimulator

- 5.4 Sacral nerve stimulator

- 5.5 Vagus nerve stimulator

- 5.6 Gastric electric stimulator

- 5.7 Transcutaneous electrical nerve stimulation (tens)

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Invasive

- 6.3 Non-invasive

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pain management

- 7.3 Urinary and fecal incontinence

- 7.4 Parkinson's disease

- 7.5 Epilepsy

- 7.6 Essential tremor

- 7.7 Gastroparesis

- 7.8 Depression

- 7.9 Dystonia

- 7.10 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgery centers

- 8.4 Specialty clinics

- 8.5 Other End uses

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 1.1.1 U.S.

- 1.1.2 Canada

- 9.3 Europe

- 1.1.3 Germany

- 1.1.4 UK

- 1.1.5 France

- 1.1.6 Spain

- 1.1.7 Italy

- 1.1.8 Netherlands

- 9.4 Asia Pacific

- 1.1.9 China

- 1.1.10 Japan

- 1.1.11 India

- 1.1.12 Australia

- 1.1.13 South Korea

- 9.5 Latin America

- 1.1.14 Brazil

- 1.1.15 Mexico

- 1.1.16 Argentina

- 9.6 Middle East and Africa

- 1.1.17 South Africa

- 1.1.18 Saudi Arabia

- 1.1.19 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Aleva Neurotherapeutics

- 10.3 BioControl Medical

- 10.4 Boston Scientific

- 10.5 ElectroCore

- 10.6 Endostim

- 10.7 Helbling Holding

- 10.8 Innovative Health Solutions

- 10.9 Laborie

- 10.10 LivaNova

- 10.11 Medtronic

- 10.12 MicroTransponder

- 10.13 Neuronetics

- 10.14 Parasym

- 10.15 RS Medical

- 10.16 Synapse Biomedical

- 10.17 tVNS Technologies (Cerbomed)

皮膚切口器械市場:按器械類型、應用領域和使用方式分類的全球市場預測,2026-2032年神經刺激設備市場:2026-2032年全球市場預測(依產品類型、材料類型、電源、技術、年齡層、應用、最終用戶和通路分類)

皮膚切口器械市場:按器械類型、應用領域和使用方式分類的全球市場預測,2026-2032年神經刺激設備市場:2026-2032年全球市場預測(依產品類型、材料類型、電源、技術、年齡層、應用、最終用戶和通路分類) 2026年全球神經刺激設備市場報告2026年全球閉合迴路調控處理設備市場報告2026年全球非侵入式神經刺激設備市場報告

2026年全球神經刺激設備市場報告2026年全球閉合迴路調控處理設備市場報告2026年全球非侵入式神經刺激設備市場報告 全球皮膚切口器械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球神經刺激設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球皮膚切口器械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球神經刺激設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 神經刺激設備市場報告:按刺激類型、設備類型、應用、最終用戶和地區分類(2026-2034 年)

神經刺激設備市場報告:按刺激類型、設備類型、應用、最終用戶和地區分類(2026-2034 年) 2026-2030年全球神經刺激設備市場氣動皮膚刀市場按產品類型、價格範圍、刀片尺寸、應用、最終用戶和分銷管道分類-2026-2032年全球預測

2026-2030年全球神經刺激設備市場氣動皮膚刀市場按產品類型、價格範圍、刀片尺寸、應用、最終用戶和分銷管道分類-2026-2032年全球預測