|

市場調查報告書

商品編碼

1858866

用於熱療的磁性奈米粒子市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Magnetic Nanoparticles for Hyperthermia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

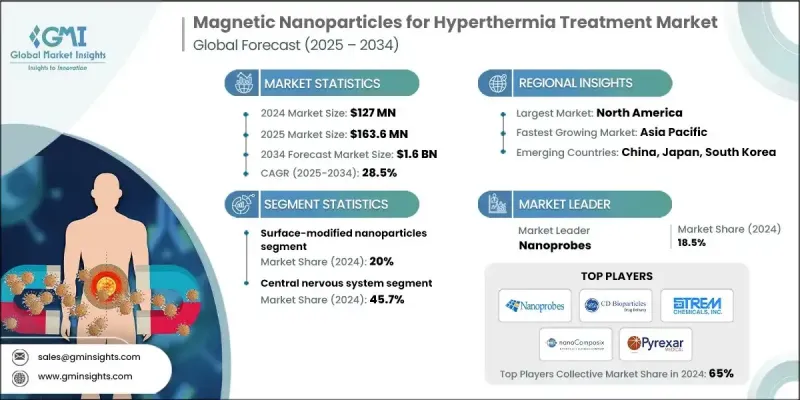

2024 年全球用於熱療的磁性奈米粒子市場價值為 1.27 億美元,預計到 2034 年將以 28.5% 的複合年成長率成長至 16 億美元。

磁熱療利用超順磁性氧化鐵奈米顆粒(SPIONs)和其他工程顆粒,這些顆粒在交變磁場作用下會產生熱。這種可控的熱能用於破壞腫瘤組織,同時保護健康細胞,使其成為傳統腫瘤治療的強效替代或輔助療法。抗藥性癌症類型的日益增加以及對標靶、非侵入性療法的需求不斷成長是推動該技術發展的關鍵因素。隨著全球醫學界尋求精準干預,研究力度不斷增加,尤其是在具有挑戰性的腫瘤治療應用方面。磁性奈米顆粒能夠穿過生物屏障並到達腫瘤深層部位,這引起了臨床醫生的極大興趣。儘管複雜的生產流程和監管障礙仍然存在,但表面功能化、雙藥聯合療法和試驗設計方面的進展正推動該技術走向更廣泛的臨床應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.27億美元 |

| 預測值 | 16億美元 |

| 複合年成長率 | 28.5% |

2024年,磁熱療市佔率達45.7%。這一主導地位與神經腫瘤學領域對非侵入性治療方法的需求密切相關。基於磁性奈米顆粒的系統可透過磁振造影相容的遞送方式實現高度局部化的加熱,從而能夠更精準地制定腦腫瘤治療方案。均勻加熱和神經保護策略的創新正引領著目前的研究,並保持著該領域的高關注度。針對侵襲性和復發性腫瘤的治療方案不斷推動中樞神經系統相關技術的投資和應用。

由於其安全性高、磁性能可重複且與醫學成像相容,超順磁性氧化鐵奈米顆粒(SPIONs)在2024年佔據了70.1%的市場佔有率。這些奈米顆粒因其可預測的加熱能力和穩定的比吸收率(SAR)而被廣泛應用於臨床和研究領域。小型化、均勻磁芯和增強磁化特性等方面的進展顯著改善了臨床療效。 SPIONs,特別是尺寸在10至15奈米之間的最佳化尺寸,因其良好的生物分佈和熱控制效率而備受青睞,使其成為大多數早期應用的首選。

2024年,歐洲用於熱療的磁性奈米顆粒市佔率將達到35%,其中德國、法國、英國、西班牙和義大利等國在應用方面處於領先地位。這一區域成長得益於成熟的精準腫瘤學體系和有利的醫療政策,這些因素促進了新興療法的順利整合。歐洲各地的腫瘤中心已開始採用導管引導系統和磁振造影相容的熱療平台。協調的臨床試驗網路和採購系統有助於縮短臨床驗證和廣泛應用之間的時間,為醫院系統更廣泛地接受該技術奠定了基礎。

全球用於熱療的磁性奈米顆粒產業的主要企業包括nanoComposix、Spherotech、Nanoprobes、Strem Chemicals、BSD Medical Corporation、Pyrexar Medical和CD Bioparticles。為了鞏固市場地位,這些主要企業正大力投資研發,以提高奈米顆粒的效率、磁響應性和生物相容性。各公司致力於改進顆粒合成方法、降低批次差異,並改進表面修飾以支持聯合療法。與學術機構和臨床中心的策略合作正在推動方案製定和試驗驗證。此外,各公司也正在努力整合即時成像功能和患者個人化治療方案。同時,各公司也積極與衛生監管機構進行早期溝通,以簡化法規核准流程。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場規模及預測:依奈米顆粒類型分類,2021-2034年

- 主要趨勢

- 超順磁性氧化鐵奈米粒子(SPIONS)

- 磁鐵礦(Fe3O4)芯材配方

- 磁赤鐵礦(γ-Fe2O3)基體系

- 核殼型氧化鐵結構

- 表面改質奈米粒子

- 工程奈米顆粒系統

- 用於組織穿透的尺寸最佳化顆粒(10-100 nm)

- 具有成像功能的多功能奈米粒子

- 採用可生物分解配方,提高安全性

第6章:市場規模及預測:依癌症應用領域分類,2021-2034年

- 主要趨勢

- 中樞神經系統癌症

- 多形性膠質母細胞瘤(GBM)治療

- 復發性腦腫瘤 CE 標誌先例

- 泌尿生殖系統癌症

- 攝護腺癌局部熱療

- 子宮頸癌合併放射治療

- 乳癌和婦科癌症

- 表淺性乳癌

- 卵巢癌腹膜

- 其他

第7章:市場規模及預測:依治療方式分類,2021-2034年

- 主要趨勢

- 獨立式磁熱療

- 聯合放射療法

- 合併化療

第8章:市場規模及預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Nanoprobes

- CD Bioparticles

- Strem Chemicals

- BSD Medical Corporation

- Pyrexar Medical

- nanoComposix

- Spherotech

The Global Magnetic Nanoparticles for Hyperthermia Treatment Market was valued at USD 127 million in 2024 and is estimated to grow at a CAGR of 28.5% to reach USD 1.6 billion by 2034.

Magnetic hyperthermia therapy uses superparamagnetic iron oxide nanoparticles (SPIONs) and other engineered particles that generate heat when exposed to alternating magnetic fields. This controlled thermal energy is used to damage tumor tissue while preserving healthy cells, positioning this approach as a powerful alternative or adjunct to conventional oncology treatments. The increasing prevalence of resistant cancer types and the rising demand for targeted, non-invasive therapies are key growth drivers. Research efforts have intensified, particularly in challenging oncologic applications, as the global medical community seeks precision-based interventions. The ability of magnetic nanoparticles to navigate biological barriers and reach deep tumor sites has sparked significant clinical interest. Although complex manufacturing processes and regulatory barriers persist, developments in surface functionalization, dual-therapy combinations, and trial design are pushing the technology toward broader clinical readiness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $127 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 28.5% |

In 2024, the magnetic hyperthermia segment held a 45.7% share. This dominance is tied to the need for non-invasive approaches in neuro-oncology. Magnetic nanoparticle-based systems offer highly localized heating through MR-compatible delivery methods, allowing for more accurate therapeutic planning in brain tumors. Innovations in homogeneous heating and neuroprotection strategies are guiding ongoing research and maintaining high interest in this segment. Treatment protocols for aggressive and recurrent tumors continue to drive investment and adoption in CNS-focused technologies.

The SPIONs segment held 70.1% share in 2024, owing to their well-established safety, repeatable magnetic performance, and compatibility with medical imaging. These nanoparticles are widely used in clinical and research settings due to their predictable heating capabilities and stable specific absorption rates (SAR). Progress in smaller engineering, uniform cores and enhancing magnetization profiles has significantly improved clinical outcomes. SPIONs, particularly with optimized sizes between 10 and 15 nm, are known for their biodistribution and thermal control efficiency, which has made them the preferred choice in most early-stage deployments.

Europe Magnetic Nanoparticles for Hyperthermia Treatment Market held 35% share in 2024, with countries such as Germany, France, the UK, Spain, and Italy leading in adoption. This regional growth is supported by established precision oncology frameworks and favorable health policies that enable smoother integration of emerging treatments. Oncology centers across Europe have begun adopting catheter-guided systems and MR-compatible hyperthermia platforms. Coordinated trial networks and procurement systems help shorten the time between clinical validation and widespread availability, setting the stage for broader acceptance across hospital systems.

Key companies operating in the Global Magnetic Nanoparticles for Hyperthermia Treatment Industry include nanoComposix, Spherotech, Nanoprobes, Strem Chemicals, BSD Medical Corporation, Pyrexar Medical, and CD Bioparticles. To strengthen their presence, key players in the magnetic nanoparticles for hyperthermia treatment market are investing heavily in R&D to enhance nanoparticle efficiency, magnetic responsiveness, and biocompatibility. Companies are focused on refining particle synthesis methods, reducing batch variability, and improving surface modification to support combination therapies. Strategic collaborations with academic institutions and clinical centers are helping drive protocol development and trial validation. Firms are also working to integrate real-time imaging compatibility and patient-specific treatment planning. In parallel, efforts to streamline regulatory approval processes are underway through early engagement with health authorities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Nanoparticle Type

- 2.2.2 Cancer Application

- 2.2.3 Treatment Modality

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Nanoparticle Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Superparamagnetic iron oxide nanoparticles (SPIONS)

- 5.2.1 Magnetite (fe3o4) core formulations

- 5.2.2 Maghemite (γ-fe2o3) based systems

- 5.2.3 Core-shell iron oxide structures

- 5.3 Surface-modified nanoparticles

- 5.4 Engineered nanoparticle systems

- 5.4.1 Size-optimized particles (10-100 nm) for tissue penetration

- 5.4.2 Multi-functional nanoparticles with imaging capabilities

- 5.4.3 Biodegradable formulations for enhanced safety

Chapter 6 Market Size and Forecast, By Cancer Application, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Central nervous system cancers

- 6.2.1 Glioblastoma multiforme (GBM) treatment

- 6.2.2 Recurrent brain tumor CE marking precedent

- 6.3 Genitourinary cancers

- 6.3.1 Prostate cancer localized hyperthermia

- 6.3.2 Cervical carcinoma with radiation therapy combinations

- 6.4 Breast & gynecological cancers

- 6.4.1 Superficial breast cancer

- 6.4.2 Ovarian cancer peritoneal

- 6.5 Others

Chapter 7 Market Size and Forecast, By Treatment Modality, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Standalone magnetic hyperthermia

- 7.3 Combination with radiation therapy

- 7.4 Combination with chemotherapy

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Nanoprobes

- 9.2 CD Bioparticles

- 9.3 Strem Chemicals

- 9.4 BSD Medical Corporation

- 9.5 Pyrexar Medical

- 9.6 nanoComposix

- 9.7 Spherotech