|

市場調查報告書

商品編碼

1858865

V2X通訊晶片市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)V2X Communication Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

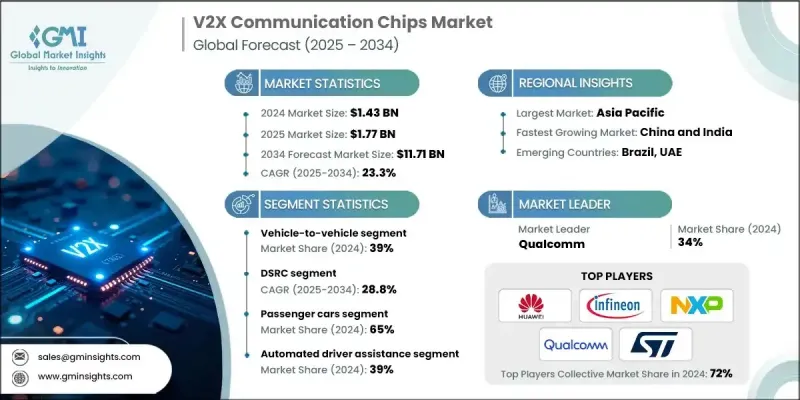

2024 年全球 V2X 通訊晶片市值為 14.3 億美元,預計到 2034 年將以 23.3% 的複合年成長率成長至 117.1 億美元。

車聯網技術在汽車和基礎設施生態系統中的日益整合推動了這一成長。 V2X 通訊晶片實現了車輛、交通基礎設施、行人以及蜂窩網路以外的網路之間的直接交互,確保了即時通訊,從而支援道路安全、交通效率、緊急應變和協同移動出行。隨著汽車原始設備製造商 (OEM)、政府機構和技術提供者朝著互聯和自動駕駛方向發展,對這些晶片的需求持續成長。半導體公司正在積極開發可擴展、安全且低延遲的 V2X 晶片組,以滿足城市和高速公路環境的需求。汽車製造商、晶片開發商和電信營運商之間的合作正在加速這些系統的部署。由於不同地區的偏好存在差異,主要廠商正在開發支援 DSRC 和 C-V2X 的雙相容解決方案。隨著應用規模的擴大,產業關注點正轉向降低單位成本和建立彈性供應鏈,以支援 V2X 技術的大規模市場推廣。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14.3億美元 |

| 預測值 | 117.1億美元 |

| 複合年成長率 | 23.3% |

到2024年,車對車(V2V)通訊領域將佔據39%的市場佔有率,這反映了其在核心V2X應用中的關鍵作用。這些晶片能夠實現車輛之間的直接資訊交換,這對於實現盲點監測、碰撞避免和車道變換輔助等功能至關重要。為了符合安全法規並支援自動駕駛功能,原始設備製造商(OEM)正在將V2V通訊功能嵌入到商用車和乘用車中。隨著監管機構不斷提高車輛安全標準,預計該領域將持續快速成長。

預計到2034年,專用短程通訊(DSRC)市場將以28.8%的複合年成長率成長。 DSRC工作在5.9 GHz頻段,可在車輛與周邊基礎設施之間提供短距離、低延遲的通訊。它廣泛應用於安全關鍵型應用,例如緊急煞車、事故警報和交通場景中的車輛優先順序。 DSRC在北美和歐洲部分地區已開始初步應用,並在區域監管框架的支援下,繼續在初始V2X基礎設施部署中發揮重要作用。

預計到2024年,中國V2X通訊晶片市場規模將達4.17億美元。中國汽車產量的快速成長(預計到2024年將達到3,130萬輛,年均成長率達4%)正在推動V2X晶片的應用。政府主導的智慧交通、自動駕駛和數位基礎設施建設等措施正在加速V2X系統的部署。國家政策、試點計畫以及對智慧交通解決方案日益成長的需求,預計將進一步鞏固中國在該地區的領先地位。

全球V2X通訊晶片市場的主要參與者包括高通、恩智浦半導體、英飛凌科技、義法半導體、博世、電裝、華為、哈曼和大陸集團。為了鞏固市場地位,V2X通訊晶片市場的企業正專注於幾項核心策略。這些策略包括開發支援DSRC和蜂窩V2X標準的雙模晶片組,以滿足全球不同的監管環境。領先企業也優先考慮超低延遲和高能源效率架構,以滿足即時安全需求並延長電動車平台的電池壽命。與汽車製造商和網路供應商的策略合作有助於使晶片設計與車輛開發時間表和基礎設施準備保持一致。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預報

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 連網和自動駕駛車輛的部署日益增多

- 政府強制要求道路安全和智慧交通系統基礎設施

- 向具備 5G 相容性的 C-V2X 過渡

- OEM半導體合作夥伴關係以實現可擴展性

- 產業陷阱與挑戰

- 高昂的整合和測試成本

- DSRC 和 C-V2X 標準之間的差異

- 市場機遇

- 智慧城市基礎設施擴建與5G網路部署

- 與ADAS和自動駕駛系統的整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 用例和應用

- 最佳情況

- 區域基礎設施準備狀況

- 5G網路滲透率

- 智慧城市發展現狀

- V2 X 測試的道路基礎設施

- 基準化分析與關鍵績效指標

- 晶片性能指標(延遲、範圍、可靠性)

- 關鍵參與者的基準化分析

- 行業標準和認證

- 市場採納情景

- 短期(1-3年)採用率預測

- 中期(4-7年)採用率預測

- 長期(8-10年)採用率預測

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依通訊方式分類,2021-2034年

- 主要趨勢

- 車對車

- 車路協同

- 車輛與行人

- 車聯網

- 其他

第6章:市場估算與預測:以連結方式分類,2021-2034年

- 主要趨勢

- DSRC

- C-V2X

第7章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車輛(HCV)

- 搭乘用車

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 自動駕駛輔助

- 交通管理

- 緊急車輛通知

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球參與者

- Qualcomm

- NXP Semiconductors

- Huawei Technologies

- Infineon Technologies

- STMicroelectronics

- Continental

- Robert Bosch

- Denso Corporation

- Harman

- Intel Corporation

- 區域玩家

- Autotalks

- Commsignia

- Cohda Wireless

- Savari

- Panasonic Automotive

- 新興參與者/顛覆者

- Veoneer

- Excelfore

- Visteon Corporation

- NXP Labs Startup Ventures

- KT Corporation Automotive Solutions

The Global V2X Communication Chips Market was valued at USD 1.43 billion in 2024 and is estimated to grow at a CAGR of 23.3% to reach USD 11.71 billion by 2034.

The growth is fueled by the rising integration of connected vehicle technologies across automotive and infrastructure ecosystems. V2X communication chips enable direct interaction between vehicles, traffic infrastructure, pedestrians, and networks beyond cellular connectivity, ensuring real-time communication that supports road safety, traffic efficiency, emergency response, and cooperative mobility. As automotive OEMs, government agencies, and tech providers move toward connected and autonomous driving, demand for these chips continues to grow. Semiconductor firms are actively developing scalable, secure, and low-latency V2X chipsets tailored for both urban and highway environments. Collaborations between automakers, chip developers, and telecom providers are accelerating the deployment of these systems. With regional preferences differing, major players are creating dual-compatible solutions supporting both DSRC and C-V2X. As adoption scales up, industry focus is shifting toward reducing unit costs and building resilient supply chains to support mass-market rollouts of V2X technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.43 Billion |

| Forecast Value | $11.71 Billion |

| CAGR | 23.3% |

The vehicle-to-vehicle (V2V) communication segment held a 39% share in 2024, reflecting its pivotal role in core V2X applications. These chips facilitate the direct exchange of information between vehicles, which is vital for enabling features like blind spot monitoring, collision avoidance, and lane-change assistance. OEMs are embedding V2V communication functions in both commercial and passenger vehicles to comply with safety regulations and support autonomous driving functionalities. As regulatory bodies push for higher standards in vehicle safety, this segment is expected to witness continued acceleration.

In 2024, the DSRC (Dedicated Short-Range Communications) segment will grow at a CAGR of 28.8% through 2034. Operating in the 5.9 GHz spectrum, DSRC provides short-range, low-latency communication between vehicles and surrounding infrastructure. It is widely used for safety-critical applications, including emergency braking, accident alerts, and vehicle prioritization in traffic scenarios. With early-stage adoption already visible in North America and certain parts of Europe, DSRC continues to play a strong role in initial V2X infrastructure deployments supported by regional regulatory frameworks.

China V2X Communication Chips Market generated USD 417 million in 2024. The country's rapid expansion in vehicle production, totaling 31.3 million units in 2024 with a 4% annual increase, is bolstering V2X chip adoption. Government-led initiatives focused on smart transportation, autonomous mobility, and digital infrastructure are accelerating the deployment of V2X systems. National policies, pilot projects, and the growing need for intelligent traffic solutions are expected to strengthen the country's leadership position in the region.

Key players in the Global V2X Communication Chips Market include Qualcomm, NXP Semiconductors, Infineon Technologies, STMicroelectronics, Robert Bosch, Denso, Huawei Technologies, Harman, and Continental. To solidify their presence, companies in the V2X Communication Chips Market are focusing on several core strategies. These include developing dual-mode chipsets that support both DSRC and cellular V2X standards to cater to varied global regulatory environments. Leaders are also prioritizing ultra-low-latency and power-efficient architectures to meet real-time safety demands and extend battery life in EV platforms. Strategic collaborations with automakers and network providers help align chip designs with vehicle development timelines and infrastructure readiness.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Communication

- 2.2.3 Connectivity

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing deployment of connected and autonomous vehicles

- 3.2.1.2 Government mandates road safety and ITS infrastructure

- 3.2.1.3 Transition toward C-V2X with 5G compatibility

- 3.2.1.4 OEM-semiconductor partnerships for scalability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High integration and testing costs

- 3.2.2.2 Fragmentation between DSRC and C-V2X standards

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of smart city infrastructure and 5G rollout

- 3.2.3.2 Integration with ADAS and autonomous driving systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability & environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and applications

- 3.11 Best-case scenario

- 3.12 Regional Infrastructure Readiness

- 3.12.1. 5 G network penetration

- 3.12.2 Smart city development status

- 3.12.3. Road infrastructure for V2 X testing

- 3.13 Benchmarking & KPIs

- 3.13.1 Performance metrics for chips (latency, range, reliability)

- 3.13.2 Benchmarking of key players

- 3.13.3 Industry standards and certifications

- 3.14 Market Adoption Scenarios

- 3.14.1 Short-term (1-3 years) adoption forecast

- 3.14.2 Mid-term (4-7 years) adoption forecast

- 3.14.3 Long-term (8-10 years) adoption forecast

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Communication, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Vehicle-to-Vehicle

- 5.3 Vehicle-to-Infrastructure

- 5.4 Vehicle-to-Pedestrian

- 5.5 Vehicle-to-Network

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 DSRC

- 6.3 C-V2X

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.1.1 Passenger Vehicles

- 7.1.1.1 Hatchback

- 7.1.1.2 Sedan

- 7.1.1.3 SUV

- 7.1.2 Commercial Vehicles

- 7.1.2.1 Light Commercial Vehicles (LCV)

- 7.1.2.2 Medium Commercial Vehicles (MCV)

- 7.1.2.3 Heavy Commercial Vehicles (HCV)

- 7.1.1 Passenger Vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Automated Driver Assistance

- 8.3 Traffic Management

- 8.4 Emergency Vehicle Notification

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Qualcomm

- 10.1.2 NXP Semiconductors

- 10.1.3 Huawei Technologies

- 10.1.4 Infineon Technologies

- 10.1.5 STMicroelectronics

- 10.1.6 Continental

- 10.1.7 Robert Bosch

- 10.1.8 Denso Corporation

- 10.1.9 Harman

- 10.1.10 Intel Corporation

- 10.2 Regional Players

- 10.2.1 Autotalks

- 10.2.2 Commsignia

- 10.2.3 Cohda Wireless

- 10.2.4 Savari

- 10.2.5 Panasonic Automotive

- 10.3 Emerging Players / Disruptors

- 10.3.1 Veoneer

- 10.3.2 Excelfore

- 10.3.3 Visteon Corporation

- 10.3.4 NXP Labs Startup Ventures

- 10.3.5 KT Corporation Automotive Solutions

汽車V2X市場(至2035年):依連接類型、通訊類型、車輛類型、推進類型、技術類型、地區、產業趨勢及預測

汽車V2X市場(至2035年):依連接類型、通訊類型、車輛類型、推進類型、技術類型、地區、產業趨勢及預測 2025年全球V2X訊息顯示面板市場報告

2025年全球V2X訊息顯示面板市場報告 5G V2X通訊:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

5G V2X通訊:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) V2L(車輛到貨物)市場:按產量、應用、最終用戶和地區分類

V2L(車輛到貨物)市場:按產量、應用、最終用戶和地區分類 車聯網(V2X)通訊模組市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

車聯網(V2X)通訊模組市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) V2X (Vehicle to Everything) 市場:連接類型 (蜂巢式·非蜂巢式)·通訊類型 (V2v·V2I·V2P)·車輛自規則性層級、安全性·各商用用途 (2025年~2030年)

V2X (Vehicle to Everything) 市場:連接類型 (蜂巢式·非蜂巢式)·通訊類型 (V2v·V2I·V2P)·車輛自規則性層級、安全性·各商用用途 (2025年~2030年) 全球汽車超寬頻 (UWB) 市場:市場佔有率和排名、總收入和需求預測(2025-2031 年)汽車V2X:全球市場佔有率和排名、總銷量和需求預測(2025-2031年)

全球汽車超寬頻 (UWB) 市場:市場佔有率和排名、總收入和需求預測(2025-2031 年)汽車V2X:全球市場佔有率和排名、總銷量和需求預測(2025-2031年) 汽車V2X市場按通訊技術、組件類型、應用、車輛類型和最終用戶分類-2025-2032年全球預測車對車通訊市場按通訊類型、應用、組件、車輛類型和最終用戶分類-全球預測,2025-2032年

汽車V2X市場按通訊技術、組件類型、應用、車輛類型和最終用戶分類-2025-2032年全球預測車對車通訊市場按通訊類型、應用、組件、車輛類型和最終用戶分類-全球預測,2025-2032年