|

市場調查報告書

商品編碼

1858863

電動曝氣系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Electric Aeration Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

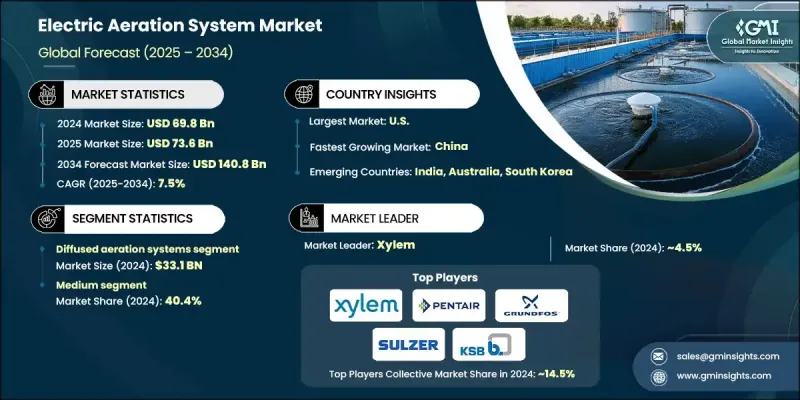

2024 年全球電動曝氣系統市場價值為 698 億美元,預計到 2034 年將以 7.5% 的複合年成長率成長至 1,408 億美元。

曝氣製程能耗的不斷增加顯著提升了對節能系統的需求。工業營運商和公用事業公司正優先考慮採用智慧曝氣技術,以降低能源成本和碳排放。隨著營運效率成為首要關注點,業界正轉向利用即時監測和自動化技術的精準曝氣方法。這些進步有助於根據進水量和處理需求最佳化氧氣輸送,從而確保更有效率的系統性能。變頻驅動器、人工智慧控制、基於模型的策略和計算流體動力學等創新技術正得到日益廣泛的應用。此外,歐洲更完善的監管框架和標準化的氧氣傳輸測量方法也促使製造商提升產品性能和可比性。這些趨勢,加上為實現永續發展目標而進行的更廣泛的污水處理基礎設施現代化改造,正在改變全球電動曝氣系統的格局。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 698億美元 |

| 預測值 | 1408億美元 |

| 複合年成長率 | 7.5% |

2024年,擴散曝氣系統市場規模達到331億美元,預計2034年將以7.2%的複合年成長率成長。其市場主導地位源自於其節能高效和高效的氧氣傳輸。這些系統的核心部件—微氣泡擴散器,能夠最大限度地增加空氣與水的接觸面積,使其成為市政和工業環境的理想選擇。其可擴展性和對各種水箱設計的適應性,也促進了其廣泛應用,尤其是在節能和性能至關重要的領域。

2024年,中價位系統市場規模達到281億美元,佔40.4%的市佔率。這些系統提供全面的解決方案,兼顧性能、現代化功能和成本效益。憑藉整合的數位控制、模組化設計和節能技術,這些系統深受注重成本的行業青睞,例如中型工業設施、農業和地方市政部門。它們在廢水處理和水產養殖等多種應用領域的靈活性,使其成為追求性價比和可靠性的用戶的熱門選擇。

2024年美國電動曝氣系統市場規模達194億美元,預計2025年至2034年間將以6.8%的複合年成長率成長。老化的污水處理基礎設施、日益嚴格的環境合規要求以及聯邦和州政府的大量資金投入,都在推動全美範圍內的升級改造。支持清潔水計畫的各項計畫正在加速向電動曝氣系統的轉型,這類系統具有控制性更強、能耗更低、可靠性更高的優點。對現代化解決方案的需求,使得這些系統成為水利基礎設施專案的重點。

全球電動曝氣系統市場的主要參與者包括 Danner Manufacturing、蘇伊士水務技術公司 (SUEZ Water Technologies)、開利全球 (Carrier Global)、Aqua-Aerobic Systems、特靈科技 (Trane Technologies)、蘇爾壽利有限公司 (Sulzer Ltd)、江森自控 (Johnson Controls)、KSBt Technologies pixt. Industries)、威立雅水務科技公司 (Veolia Water Technologies)、賽萊默公司 (Xylem Inc.)、霍尼韋爾 (Honeywell)、格蘭富 (Grundfos) 和 Sanitaire。電動曝氣系統市場的領導者正致力於整合人工智慧、即時感測器和SCADA系統等智慧技術,以提高系統效率和監控能力。產品創新是受到市場對能夠適應不同負荷條件並降低能耗的系統的需求所驅動。各公司正在擴大研發預算,以開發模組化、可擴展的系統,從而滿足更廣泛的客戶群。許多公司也與市政和工業客戶建立合作關係,進行長期基礎設施專案。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 2024年定價分析

- 按地區和產品

- 原料成本

- 未來市場趨勢

- 風險評估與緩解

- 監理合規風險

- 產能限制影響分析

- 技術轉型風險

- 價格波動和成本上漲風險

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- 擴散曝氣系統

- 表面曝氣系統

- 地下曝氣系統

- 文丘里曝氣系統

- 壓縮空氣系統

- 混合曝氣系統

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 機械曝氣技術

- 氣動充氣技術

- 電化學曝氣

- 混合技術系統

- 智慧/物聯網系統

第7章:市場估計與預測:依價格區間分類,2021-2034年

- 主要趨勢

- 低的

- 中等的

- 高的

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 市政污水處理

- 大型設施(>5000萬加侖/天)

- 中型設施(5-50 MGD)

- 小型/分散式系統(<5 MGD)

- 工業製程水處理

- 製造業

- 化學加工

- 食品飲料業

- 製藥

- 其他

- 住宅

- 商業的

第9章:市場估算與預測:依營運模式分類,2021-2034年

- 主要趨勢

- 自動的

- 半自動

- 手動的

第10章:市場估價與預測:依配銷通路,2021-2034年

- 主要趨勢

- 直銷

- 間接銷售

第11章:市場估計與預測:按地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第12章:公司簡介

- Carrier Global

- Daikin Industries

- Danner Manufacturing

- Evoqua Water Technologies

- Grundfos

- Honeywell

- Johnson Controls

- KSB Group

- Pentair plc

- Sanitaire

- SUEZ Water Technologies

- Sulzer Ltd

- Trane Technologies

- Veolia Water Technologies

- Xylem Inc.

The Global Electric Aeration Systems Market was valued at USD 69.8 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 140.8 billion by 2034.

Increasing energy consumption in aeration processes has significantly boosted demand for energy-efficient systems. Industrial operators and utilities are prioritizing smart aeration technologies to reduce energy expenses and lower their carbon footprint. As operational efficiency becomes a top concern, the industry is pivoting toward precision aeration methods that utilize real-time monitoring and automation. These advancements help optimize oxygen delivery based on inflow and treatment needs, ensuring more efficient system performance. Innovations such as variable frequency drives, AI-powered controls, model-based strategies, and computational fluid dynamics are being increasingly implemented. Additionally, enhanced regulatory frameworks and standardized oxygen transfer measurements in Europe have pushed manufacturers to improve product performance and comparability. These trends, combined with broader efforts to modernize outdated wastewater infrastructure and meet sustainability goals, are transforming the electric aeration systems landscape worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $69.8 Billion |

| Forecast Value | $140.8 Billion |

| CAGR | 7.5% |

The diffused aeration systems segment generated USD 33.1 billion in 2024, with an anticipated CAGR of 7.2% through 2034. Their dominance stems from their energy-efficient operation and effective oxygen transfer. Fine bubble diffusers, which are integral to these systems, maximize air-to-water contact, making them ideal for both municipal and industrial settings. Their scalability and ability to fit various tank designs support their widespread application, especially where energy savings and performance are key priorities.

The medium-priced systems segment reached USD 28.1 billion in 2024, holding a 40.4% share. These systems offer a well-rounded package that balances performance, modern features, and cost-effectiveness. With integrated digital controls, modular capabilities, and energy-saving technologies, these systems appeal to cost-conscious sectors such as mid-sized industrial facilities, agriculture, and local municipalities. Their flexibility across multiple applications, including wastewater treatment and aquaculture, makes them a popular choice among users looking for value and reliability.

U.S. Electric Aeration Systems Market generated USD 19.4 billion in 2024 and is projected to grow at a CAGR of 6.8% between 2025 and 2034. Aging treatment infrastructure, rising environmental compliance demands, and significant federal and state funding are all fueling upgrades across the country. Programs that support clean water initiatives are accelerating the shift toward electric aeration systems that offer enhanced control, reduced energy use, and better reliability. The push for modernized solutions has placed these systems at the forefront of water infrastructure projects.

Key players in the Global Electric Aeration Systems Market include Danner Manufacturing, SUEZ Water Technologies, Carrier Global, Aqua-Aerobic Systems, Trane Technologies, Sulzer Ltd, Johnson Controls, KSB Group, Pentair plc, Evoqua Water Technologies, Daikin Industries, Veolia Water Technologies, Xylem Inc., Honeywell, Grundfos, and Sanitaire. Leading companies in the Electric Aeration Systems Market are focusing on integrating smart technologies such as AI, real-time sensors, and SCADA systems to boost system efficiency and monitoring capabilities. Product innovation is being driven by demand for systems that adapt to variable load conditions and reduce energy consumption. Firms are expanding R&D budgets to develop modular, scalable systems that cater to a wider customer base. Many are also forming partnerships with municipal and industrial clients for long-term infrastructure projects.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Technology trends

- 2.2.3 Price range trends

- 2.2.4 Application trends

- 2.2.5 Operation mode trends

- 2.2.6 Distribution channel trends

- 2.2.7 Regional trends

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

- 2.5 Strategic recommendations

- 2.5.1 Supply chain diversification strategy

- 2.5.2 Product portfolio enhancement

- 2.5.3 Partnership and alliance opportunities

- 2.5.4 Cost management and pricing strategy

- 2.6 Decision framework

- 2.6.1 Investment priority matrix

- 2.6.2 Risk-adjusted ROI analysis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.4.1 By region and product

- 3.4.2 Raw material cost

- 3.5 Future market trends

- 3.6 Risk assessment and mitigation

- 3.6.1 Regulatory compliance risks

- 3.6.2 Capacity constraint impact analysis

- 3.6.3 Technology transition risks

- 3.6.4 Pricing volatility and cost escalation risks

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Diffused Aeration Systems

- 5.3 Surface Aeration Systems

- 5.4 Subsurface Aeration Systems

- 5.5 Venturi Aeration Systems

- 5.6 Compressed Air Systems

- 5.7 Hybrid Aeration Systems

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Mechanical Aeration Technology

- 6.3 Pneumatic Aeration Technology

- 6.4 Electrochemical Aeration

- 6.5 Hybrid Technology Systems

- 6.6 Smart/IoT-Enabled Systems

Chapter 7 Market Estimates & Forecast, By Price Range, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Municipal Wastewater Treatment

- 8.2.1 Large-Scale Facilities (>50 MGD)

- 8.2.2 Medium-Scale Facilities (5-50 MGD)

- 8.2.3 Small/Decentralized Systems (<5 MGD)

- 8.3 Industrial Process Water Treatment

- 8.3.1 Manufacturing

- 8.3.2 Chemical Processing

- 8.3.3 Food & Beverage Industry

- 8.3.4 Pharmaceutical

- 8.3.5 Others

- 8.4 Residential

- 8.5 Commercial

Chapter 9 Market Estimates & Forecast, By Operation Mode, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Automatic

- 9.3 Semi-automatic

- 9.4 Manual

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 U.K.

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 12.1 Carrier Global

- 12.2 Daikin Industries

- 12.3 Danner Manufacturing

- 12.4 Evoqua Water Technologies

- 12.5 Grundfos

- 12.6 Honeywell

- 12.7 Johnson Controls

- 12.8 KSB Group

- 12.9 Pentair plc

- 12.10 Sanitaire

- 12.11 SUEZ Water Technologies

- 12.12 Sulzer Ltd

- 12.13 Trane Technologies

- 12.14 Veolia Water Technologies

- 12.15 Xylem Inc.