|

市場調查報告書

商品編碼

1858851

離子液體在電池應用領域的市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Ionic Liquids for Battery Applications Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

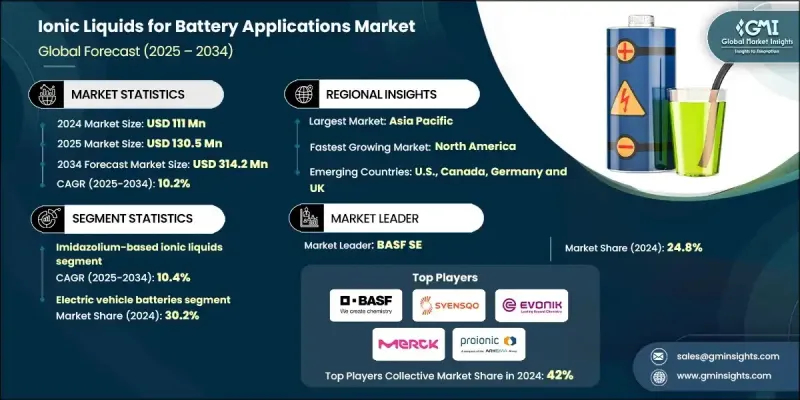

2024 年全球電池應用離子液體市場價值為 1.11 億美元,預計到 2034 年將以 10.2% 的複合年成長率成長至 3.142 億美元。

對先進儲能系統日益成長的需求正在推動市場擴張。離子液體,即低溫下呈液態的有機鹽,以其卓越的離子電導率、高熱穩定性、低揮發性和寬廣的電化學窗口而聞名。這些特性使其成為各種電池類型(包括鋰離子電池、鈉離子電池和固態電池)的理想電解質。離子液體能夠在高壓下運作並在寬溫度範圍內保持性能,使其在電動車、再生能源儲存和攜帶式電子產品領域具有獨特的價值。電動車的日益普及和電網中再生能源使用量的不斷成長,推動了對更安全、更長壽命電池的需求,進一步提升了離子液體電解質的重要性。持續的創新致力於提高電導率和降低製造成本,這將繼續促進市場加速發展。隨著越來越多的行業尋求可靠、高性能的電池技術,離子液體因其能夠延長電池壽命並提高各種應用場景下的安全性而備受關注。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.11億美元 |

| 預測值 | 3.142億美元 |

| 複合年成長率 | 10.2% |

2024年,咪唑基離子液體佔了高達45.2%的市場。其廣泛的商業化應用和可擴展的生產能力使其在維持成本效益和穩定供應方面具有顯著優勢。這些因素,加上持續的研發投入,正助力咪唑化合物在多種電池化學系統中保持其主導地位。預計在持續的研發支援下,該領域將獲得進一步發展動力,旨在提升儲能系統的效率和多功能性。

預計到2024年,電動車電池市佔率將達到30.2%。這一成長主要得益於汽車產業持續向電動出行轉型以及消費者對安全性的日益成長的需求。電動車產量的擴大、監管框架的日益嚴格以及消費者對更高性能電池的偏好,都推動了該細分市場的成長。隨著新一代電池技術的研發,許多汽車製造商正投入大量資源,致力於採用離子液體電解質來提升電池的安全性和功能性。

預計到2024年,北美電池用離子液體市場佔有率將達到28.2%,這主要得益於該地區對電池相關離子液體的需求持續成長。電動車的廣泛普及、清潔能源的併網以及對電網穩定性的日益重視,都推動了這一成長。此外,技術創新以及政府支持先進儲能基礎設施的舉措,也促進了離子液體應用的持續成長。該地區對新能源技術的積極響應,為市場的永續發展創造了有利條件。

積極推動全球電池應用離子液體市場發展的關鍵企業包括:Solvionic SA、Merck KGaA、Richman Chemical Inc.、Syensqo、NOHMs Technologies, Inc.、Evonik Industries AG、BASF SE、Proionic GmbH - Arkema Group、東京化學工業株式會社以及IoLiSF SE、Proionic GmbH - Arkema Group、東京化學工業株式會社以及IoLiTec Technologies* IHonic LiquiTec - IHonic。為鞏固市場地位,各企業正致力於拓展產品組合,例如開發針對不同電池化學體系定製配方的離子液體。許多企業優先考慮透過製程創新和擴大生產規模來降低成本,從而提高商業可行性。此外,各企業也積極與電池開發商和原始設備製造商 (OEM) 合作研發,以加速離子液體在新興電池技術中的應用。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 透過申請

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼說明:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依離子液體類型分類,2021-2034年

- 主要趨勢

- 咪唑基離子液體

- 吡咯烷基離子液體

- 鏻基離子液體

- 季銨鹽基離子液體

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 電動汽車電池

- 汽車牽引電池

- 油電混合車系統

- 快速充電應用

- 電網儲能

- 公用事業規模儲能系統

- 頻率調節應用

- 長期儲存解決方案

- 消費性電子產品

- 智慧型手機應用程式

- 筆記型電腦和攜帶式設備

- 穿戴式科技

- 航太與國防

- 衛星電池系統

- 軍事應用

第7章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第8章:公司簡介

- BASF SE

- Syensqo

- Evonik Industries AG

- Merck KGaA

- Proionic GmbH - Arkema Group

- Solvionic SA

- IoLiTec - Ionic Liquids Technologies GmbH

- Tokyo Chemical Industry Co., Ltd.

- NOHMs Technologies, Inc.

- Richman Chemical Inc.

The Global Ionic Liquids for Battery Applications Market was valued at USD 111 million in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 314.2 million by 2034.

Rising demand for advanced energy storage systems is fueling market expansion. Ionic liquids, known as organic salts in liquid form at low temperatures, are recognized for their outstanding ionic conductivity, high thermal stability, low volatility, and broad electrochemical windows. These properties make them highly suitable as electrolytes in various battery types, including lithium-ion, sodium-ion, and solid-state formats. Their ability to enable high-voltage operation and maintain performance across wide temperature ranges makes them especially valuable in electric vehicles, renewable energy storage, and portable electronics. Growing adoption of electric mobility and the increasing use of renewables in the power grid are driving the need for safer, longer-lasting batteries further elevating the relevance of ionic liquid electrolytes. Ongoing innovations are focusing on improving conductivity and reducing manufacturing costs, which continues to support market acceleration. As more industries seek reliable, high-performance battery technologies, ionic liquids are gaining significant traction for their ability to extend battery lifespan and enhance safety across diverse use cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $111 Million |

| Forecast Value | $314.2 Million |

| CAGR | 10.2% |

The imidazolium-based ionic liquids segment held a substantial 45.2% share in 2024. Their widespread commercial availability and production scalability give them a distinct edge in maintaining cost efficiency and reliable supply. These factors, along with ongoing research investments, are helping imidazolium compounds maintain their dominance across multiple battery chemistries. The segment is expected to receive further momentum through consistent R&D support aimed at unlocking even greater efficiency and versatility in energy storage systems.

The electric vehicle batteries segment held a 30.2% share in 2024. This share is driven by the continued transition to e-mobility and heightened safety expectations within the automotive sector. The expansion of EV production, stricter regulatory frameworks, and consumer preferences for better battery performance are all contributing to growth in this segment. With next-generation battery technologies under development, many automotive manufacturers are allocating significant resources toward adopting ionic liquid electrolytes to improve battery safety and functionality.

North America Ionic Liquids for Battery Applications Market held a 28.2% share in 2024, as demand for battery-related ionic liquids continues to rise across the region. This growth is being propelled by the widespread adoption of electric vehicles, integration of clean energy sources, and an increasing emphasis on grid stability. Technological innovation, alongside government initiatives to support advanced energy storage infrastructure, is contributing to the rising use of ionic liquids. The region remains highly responsive to new energy technologies, creating favorable conditions for sustained market development.

Key companies actively shaping the Global Ionic Liquids for Battery Applications Market include Solvionic SA, Merck KGaA, Richman Chemical Inc., Syensqo, NOHMs Technologies, Inc., Evonik Industries AG, BASF SE, Proionic GmbH - Arkema Group, Tokyo Chemical Industry Co., Ltd., and IoLiTec - Ionic Liquids Technologies GmbH. To strengthen their position, companies are focusing on key strategies such as expanding their product portfolios with custom-formulated ionic liquids tailored to different battery chemistries. Many are prioritizing cost reduction through process innovation and scaling production to improve commercial viability. Collaborative R&D initiatives with battery developers and OEMs are also being pursued to speed up the integration of ionic liquids into emerging battery technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Ionic liquids type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By application

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Ionic Liquids Type, 2021-2034 (USD Million & Tons)

- 5.1 Key trends

- 5.2 Imidazolium-based ionic liquids

- 5.3 Pyrrolidinium-based ionic liquids

- 5.4 Phosphonium-based ionic liquids

- 5.5 Quaternary ammonium-based ionic liquids

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Tons)

- 6.1 Key trends

- 6.2 Electric vehicle batteries

- 6.2.1 Automotive traction batteries

- 6.2.2 Hybrid vehicle systems

- 6.2.3 Fast charging applications

- 6.3 Grid energy storage

- 6.3.1 Utility-scale storage systems

- 6.3.2 Frequency regulation applications

- 6.3.3 Long-duration storage solutions

- 6.4 Consumer electronics

- 6.4.1 Smartphone applications

- 6.4.2 Laptop & portable devices

- 6.4.3 Wearable technology

- 6.5 Aerospace & defense

- 6.5.1 Satellite battery systems

- 6.5.2 Military applications

Chapter 7 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Syensqo

- 8.3 Evonik Industries AG

- 8.4 Merck KGaA

- 8.5 Proionic GmbH - Arkema Group

- 8.6 Solvionic SA

- 8.7 IoLiTec - Ionic Liquids Technologies GmbH

- 8.8 Tokyo Chemical Industry Co., Ltd.

- 8.9 NOHMs Technologies, Inc.

- 8.10 Richman Chemical Inc.

離子液體市場分析及預測(至2035年):依類型、產品類型、應用、技術、最終用戶、材料類型、形態、製程及功能分類

離子液體市場分析及預測(至2035年):依類型、產品類型、應用、技術、最終用戶、材料類型、形態、製程及功能分類 全球離子液體市場:產業分析、市場規模、佔有率及按類型、應用、最終用途、國家和地區分類的預測(2025-2032 年)

全球離子液體市場:產業分析、市場規模、佔有率及按類型、應用、最終用途、國家和地區分類的預測(2025-2032 年) 離子液體市場規模、佔有率和成長分析(按產品類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測

離子液體市場規模、佔有率和成長分析(按產品類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測 離子液體市場:按類型、形態、應用和地區分類

離子液體市場:按類型、形態、應用和地區分類 離子液體的全球市場:各純度類型,各用途類型,各地區,產業趨勢,預測

離子液體的全球市場:各純度類型,各用途類型,各地區,產業趨勢,預測 離子液體市場-全球產業規模、佔有率、趨勢、機會與預測,依應用(溶劑與催化劑、萃取與分離、生物精煉、儲能等)細分,按地區與競爭情況,2020-2030 年預測全球離子液體市場:展望、競爭策略、應用和地區預測 (~2034年)

離子液體市場-全球產業規模、佔有率、趨勢、機會與預測,依應用(溶劑與催化劑、萃取與分離、生物精煉、儲能等)細分,按地區與競爭情況,2020-2030 年預測全球離子液體市場:展望、競爭策略、應用和地區預測 (~2034年) 2024 年至 2031 年離子液體市場(按類型、最終用戶、純度和地區劃分)

2024 年至 2031 年離子液體市場(按類型、最終用戶、純度和地區劃分) 全球離子液體市場規模研究,按應用(催化/合成、食品、造紙和紙漿、電子、生物技術、汽車、製藥等)和 2022-2032 年區域預測

全球離子液體市場規模研究,按應用(催化/合成、食品、造紙和紙漿、電子、生物技術、汽車、製藥等)和 2022-2032 年區域預測 離子液體市場 - 按應用(催化、合成、食品、造紙和紙漿、電子、生物技術、汽車、製藥)和預測,2024-2032 年

離子液體市場 - 按應用(催化、合成、食品、造紙和紙漿、電子、生物技術、汽車、製藥)和預測,2024-2032 年