|

市場調查報告書

商品編碼

1858803

特種纖維作物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Specialty Fiber Crops Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

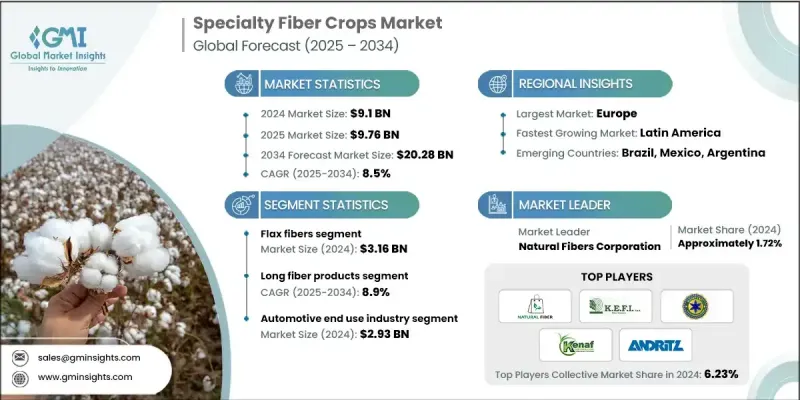

2024 年全球特種纖維作物市場價值為 91 億美元,預計到 2034 年將以 8.5% 的複合年成長率成長至 202.8 億美元。

全球各行各業對環保再生原料的需求不斷成長,推動了這個市場的穩定擴張。隨著環保意識的日益增強,製造商和消費者都開始轉向黃麻、亞麻、劍麻和麻等天然纖維,因為它們具有可生物分解、可再生和環境影響小的優點。此外,多個地區的監管機構鼓勵永續農業發展,同時限制合成材料的使用,進一步加速了更環保替代品的轉變。這些監管措施持續推動特種纖維作物產業的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 91億美元 |

| 預測值 | 202.8億美元 |

| 複合年成長率 | 8.5% |

為了吸引日益成長的注重永續發展的消費者群體,紡織服裝製造商正擴大將有機纖維融入其產品線。加工和纖維混紡技術的進步也提升了這些天然纖維的品質和應用範圍,使其在耐用性、強度和質感方面更具競爭力,足以與合成纖維相媲美。除了時尚領域,特種纖維的應用也擴展到了汽車、建築和複合材料等非傳統產業,顯著擴大了其市場佔有率。

2024年,亞麻纖維市場規模達31.6億美元,預計2025年至2034年將以8.2%的複合年成長率成長。亞麻和麻纖維需求的激增源於其強度高、使用壽命長且環境影響小,使其在複合材料、紡織品和建築材料領域日益受到青睞。棉花和洋麻等特殊纖維也因其可生物分解的特性以及在包裝、造紙和高階紡織品領域的應用而得到更廣泛的應用。此外,椰殼纖維、香蕉纖維和劍麻纖維等葉類和果類纖維因其永續性和廣泛的可用性,正成為環保包裝、家用紡織品和地工織物的理想材料。

2024年,汽車終端應用領域市場規模達到29.3億美元,預計在2025年至2034年期間將以8.7%的複合年成長率成長,佔32.2%的市場。這些天然纖維擴大應用於汽車內裝和複合材料中,為合成材料提供了一種輕質高強的替代方案。建築業也因其強度高和環保特性,將這些纖維應用於保溫板和增強構件中。

2024年,北美特種纖維作物市場規模預計將達22.4億美元。隨著建築、汽車和紡織等行業轉向使用永續材料,該地區的需求正在穩步成長。環保意識的增強、消費者對永續產品需求的不斷成長以及政府鼓勵環保耕作方式的激勵措施,都進一步推動了這一轉變。此外,纖維加工和複合材料開發領域的持續創新也促進了北美市場的擴張,這些創新正在為特種纖維開闢新的應用領域。

全球特種纖維作物市場的主要參與者包括Natural Fibers Corporation、Kenaf Partners USA、KEFISpA(義大利)、ANDRITZ Group和Hemp Inc.等。為了鞏固自身地位,全球特種纖維作物市場的各公司正採取多種策略措施。許多公司正在擴大產能,以滿足全球對永續材料日益成長的需求。研發投入的重點在於透過混紡、加工和複合材料工程的創新來提高纖維品質並拓展其應用範圍。與建築、汽車和紡織公司的合作,有助於製造商更順暢地將特種纖維整合到終端產品中。此外,企業也正在探索垂直整合模式,以確保穩定的供應鏈並提高成本效益。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 供應鏈的複雜性

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 大麻纖維

- 韌皮纖維製品

- 赫德和核心產品

- 亞麻纖維

- 洋麻纖維

- 棉特種纖維

- 葉和果實纖維

- 劍麻和蕉麻製品

- 椰殼纖維及乳草製品

- 其他纖維

第6章:市場估算與預測:依加工形式分類,2021-2034年

- 主要趨勢

- 長纖維產品

- 短纖維產品

- 核心和障礙產品

- 纖維粉末和細粉

第7章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 汽車

- 室內面板應用

- 行李箱襯墊和複合材料部件

- 建築施工

- 絕緣材料

- 生物複合材料應用

- 紙張和包裝

- 特種紙應用

- 證券和貨幣紙

- 香菸紙

- 包裝材料

- 紡織服裝

- 技術紡織品

- 消費服裝

- 家用紡織品

- 奢華和高級紡織品

- 環境與農業

- 侵蝕控制應用

- 動物墊料

- 園藝產品

- 其他終端用戶產業

- 化妝品和個人護理

- 工業過濾

- 海軍陸戰隊和國防部門

- 其他

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- KEFISpA (Italy)

- Natural Fibers Corporation

- Mississippi Delta Fiber Cooperative

- Kenaf Partners USA

- ANDRITZ Group

- Formation AG

- Hempflax Group

- Canadian Greenfield Technologies

- Hemp Inc.

- Others

The Global Specialty Fiber Crops Market was valued at USD 9.10 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 20.28 billion by 2034.

This steady market expansion is driven by rising global demand for eco-conscious and renewable raw materials across a range of industries. With increasing environmental concerns, both manufacturers and consumers are turning toward natural fibers such as jute, flax, sisal, and hemp due to their biodegradability, renewability, and reduced environmental impact. In addition, regulatory bodies in multiple regions are encouraging sustainable agriculture while imposing restrictions on synthetic materials, further accelerating the shift toward greener alternatives. This regulatory push continues to support the growth trajectory of the specialty fiber crops sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.10 Billion |

| Forecast Value | $20.28 Billion |

| CAGR | 8.5% |

Textile and apparel manufacturers are increasingly incorporating organic fibers into their product lines to appeal to a growing segment of sustainability-focused consumers. Advances in processing and fiber blending technologies have also elevated the quality and application range of these natural fibers, making them more competitive with synthetic counterparts in terms of durability, strength, and texture. Beyond fashion, the adoption of specialty fibers has grown in non-traditional industries, including automotive, construction, and composites, expanding their market footprint significantly.

The flax fiber segment was valued at USD 3.16 billion in 2024 and is projected to grow at a CAGR of 8.2% from 2025 to 2034. The surge in demand for both flax and hemp fibers stems from their strength, longevity, and low environmental impact, making them increasingly preferred for use in composites, textiles, and building materials. Specialty fibers derived from cotton and kenaf are also witnessing greater usage due to their biodegradable properties and application across packaging, paper, and premium textile segments. Additionally, leaf and fruit-based fibers such as coir, banana, and sisal are becoming viable materials for eco-friendly packaging, domestic textiles, and geotextile uses due to their sustainability and wide availability.

In 2024, the automotive end-use segment reached USD 2.93 billion in value and is expected to grow at an 8.7% CAGR, representing a 32.2% share during the 2025-2034 period. These natural fibers are increasingly used in vehicle interiors and composite materials, offering a lightweight and strong alternative to synthetics. The building and construction sector is also integrating these fibers in insulation panels and reinforcement components, owing to their strength and green credentials.

North America Specialty Fiber Crops Market generated USD 2.24 billion in 2024. The demand across this region is rising steadily as industries such as construction, automotive, and textiles move toward integrating sustainable materials. The shift is further supported by greater environmental awareness, growing consumer demand for sustainable products, and government incentives promoting eco-friendly farming practices. The expansion of the North American market is also facilitated by ongoing innovations in fiber processing and composite development, which are unlocking new applications for specialty fibers.

Prominent players leading the Global Specialty Fiber Crops Market include Natural Fibers Corporation, Kenaf Partners USA, and K.E.F.I. S.p.A. (Italy), ANDRITZ Group, and Hemp Inc., among others. To strengthen their presence, companies in the Global Specialty Fiber Crops Market are adopting a variety of strategic approaches. Many are expanding their production capacities to meet growing global demand for sustainable materials. R&D investments are focused on enhancing fiber quality and broadening applications through innovations in blending, processing, and composite engineering. Partnerships with construction, automotive, and textile companies are helping manufacturers integrate specialty fibers into end-use products more seamlessly. In addition, businesses are exploring vertical integration models to secure consistent supply chains and improve cost efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Processing Form

- 2.2.4 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Patent Landscape

- 3.10 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable Practices

- 3.11.2 Waste Reduction Strategies

- 3.11.3 Energy Efficiency in Production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021- 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Hemp fibers

- 5.2.1 Bast fiber products

- 5.2.2 Hurd and core products

- 5.3 Flax fibers

- 5.4 Kenaf fibers

- 5.5 Cotton specialty fibers

- 5.6 Leaf and fruit fibers

- 5.6.1 Sisal and abaca products

- 5.6.2 Coir and milkweed products

- 5.7 Other fibers

Chapter 6 Market Estimates and Forecast, By Processing Form, 2021 - 2034 (USD Billion, , Kilo Tons)

- 6.1 Key trends

- 6.2 Long fiber products

- 6.3 Short fiber products

- 6.4 Core and hurd products

- 6.5 Fiber powders and fines

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.2.1 Interior panel applications

- 7.2.2 Trunk liners and composite parts

- 7.3 Construction and building

- 7.3.1 Insulation materials

- 7.3.2 Biocomposite applications

- 7.4 Paper and packaging

- 7.4.1 Specialty paper applications

- 7.4.2 Security and currency paper

- 7.4.3 Cigarette paper

- 7.4.4 Packaging material

- 7.5 Textile and fashion

- 7.5.1 Technical textiles

- 7.5.2 Consumer apparel

- 7.5.3 Home textiles

- 7.5.4 Luxury and premium textiles

- 7.6 Environmental and agricultural

- 7.6.1 Erosion control applications

- 7.6.2 Animal bedding

- 7.6.3 Horticultural products

- 7.7 Other End use industries

- 7.7.1 Cosmetics and personal care

- 7.7.2 Industrial filtration

- 7.7.3 Marine and defense

- 7.7.4 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 K.E.F.I. S.p.A. (Italy)

- 9.2 Natural Fibers Corporation

- 9.3 Mississippi Delta Fiber Cooperative

- 9.4 Kenaf Partners USA

- 9.5 ANDRITZ Group

- 9.6 Formation AG

- 9.7 Hempflax Group

- 9.8 Canadian Greenfield Technologies

- 9.9 Hemp Inc.

- 9.10 Others