|

市場調查報告書

商品編碼

1844377

重型起重設備市場機會、成長動力、產業趨勢分析及2025-2034年預測Heavy Lifting Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

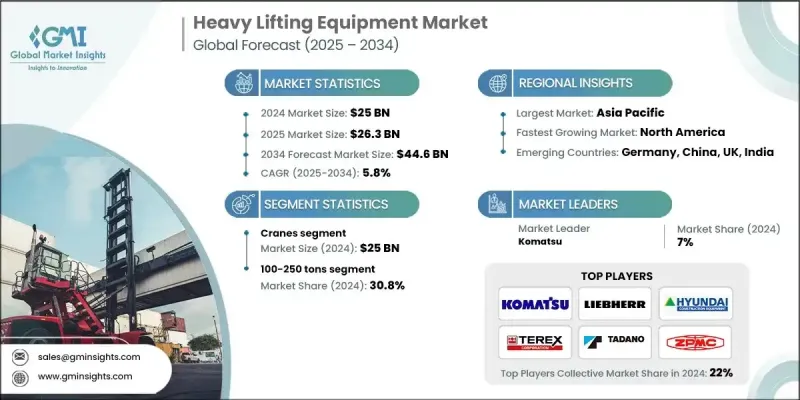

2024 年全球重型起重設備市場價值為 250 億美元,預計到 2034 年將以 5.8% 的複合年成長率成長至 446 億美元。

全球快速的城市化、工業擴張和不斷增加的基礎設施投資推動了市場的成長。重型起重設備在大型專案建設、高效採礦作業、發電以及無縫運輸和物流管理中發揮關鍵作用。由於自動化、電氣化以及物聯網和遠端資訊處理等數位技術的進步,起重機、提昇機和運輸機等重型起重設備的需求顯著成長,這些技術提高了操作安全性、效率和維護性。此外,隨著各行各業致力於減少排放並遵守更嚴格的環境法規,電動和混合動力重型起重設備的採用正在加速。這種轉變在歐洲和北美等製定了積極永續發展目標的地區尤為明顯,這些地區的政府政策和企業的環境、社會和治理 (ESG) 承諾正在推動從柴油驅動機械向柴油驅動機械的轉變。先進的電池系統、再生煞車和節能液壓系統的整合使企業能夠降低營運成本,同時提高環境績效。此外,遠端診斷、預測性維護和遠端資訊處理監控等創新技術使這些機器即使在複雜的工業環境中也能更加安全、高效。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 250億美元 |

| 預測值 | 446億美元 |

| 複合年成長率 | 5.8% |

2024年,100-250噸級起重機市場佔有30.8%的佔有率。此重量級起重機在中型至重型起重應用中發揮至關重要的作用,廣泛應用於基礎設施擴建、採礦作業和大型工業專案。這些起重機在機動性和起重能力之間實現了良好的平衡,非常適合執行諸如橋樑段定位、風力渦輪機安裝以及超大型工業設備運輸等複雜任務。它們既能適應人口稠密的城區,也能適應偏遠地區,這進一步增加了其在各種作業環境中日益成長的需求。

2024年,起重機細分市場產值達250億美元,凸顯了其在重型起重設備領域的重要性。此細分市場涵蓋各種專用機械,例如履帶起重機、塔式起重機、移動式起重機、龍門起重機和橋式起重機,每種機械均經過量身定做,以滿足製造、航運、能源和建築等行業的不同需求。這些機械經過精心設計,可提供精確的起重能力,確保在嚴苛的專案條件下安全高效地處理重物。

到2034年,亞太地區重型起重設備市場的複合年成長率將達到6.5%,這得益於中國、印度和東南亞地區大規模的基礎設施建設項目,以及為解決勞動力短缺問題而日益普及的自動化和半自動化設備。全球和本地企業的參與,加上經濟高效的創新,正在加速該地區的市場滲透。

影響重型起重設備市場的關鍵參與者包括多田野、科尼起重機、上海振華重工(ZPMC)、薩倫斯、帕爾菲格、三一重工、馬尼托瓦克公司、森尼博根、小松、利勃海爾、特雷克斯、卡哥特科、瑪姆特、JASO工業起重機和德馬格起重機及零部件。這些公司正在投資開發更智慧、更安全、更環保的起重解決方案,以滿足全球各行各業不斷變化的需求。隨著數位轉型和環保意識持續影響設備採購決策,重型起重設備市場可望在未來十年實現強勁持續的成長。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 加強基礎建設

- 採礦業和石油天然氣產業的成長

- 風能項目擴張

- 產業陷阱與挑戰

- 初期投資及維護成本高

- 熟練勞動力短缺

- 機會

- 新興經濟體的基礎建設發展

- 自動化及智慧裝備整合

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依設備類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 貿易統計(HS 編碼 - 8428)

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按設備類型,2021 - 2034 年

- 主要趨勢

- 起重機

- 移動式起重機

- 全地面起重機

- 履帶起重機

- 越野輪胎起重機

- 車載起重機

- 固定起重機

- 塔式起重機

- 橋式起重機

- 龍門起重機

- 單軌起重機

- 船舶和港口起重機

- 移動式起重機

- 起重機

- 電動葫蘆

- 油壓提昇機

- 手動葫蘆

- 運輸者

- 自行式模組化運輸車(SPMTS)

- 重型拖車

- 專用運輸車輛

第6章:市場估計與預測:按重量容量,2021 - 2034 年

- 主要趨勢

- 100-250噸

- 251-500噸

- 501-1000噸

- 1000噸以上

第7章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 建造

- 石油和天然氣

- 礦業

- 航運和港口營運

- 海洋與造船業

- 船廠營運

- 海上建築

- 船舶維護和修理

- 海軍建設

- 發電

- 常規電力

- 再生能源

- 製造業

- 其他

第 8 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 直接的

- 間接

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Cargotec

- Demag Cranes & Components

- JASO Industrial Cranes

- Komatsu

- Konecranes

- Liebherr

- Mammoet

- Manitowoc Company

- Palfinger

- SANY

- Sarens

- Sennebogen

- Shanghai Zhenhua Heavy Industries (ZPMC)

- Tadano

- Terex

The Global Heavy Lifting Equipment Market was valued at USD 25 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 44.6 billion by 2034.

Market growth is driven by rapid urbanization, industrial expansion, and increasing infrastructure investments worldwide. Heavy lifting equipment plays a critical role in enabling the construction of large-scale projects, efficient mining operations, power generation, and seamless shipping and logistics management. The demand for heavy lifting equipment such as cranes, hoists, and transporters has seen significant growth due to advances in automation, electrification, and digital technologies like IoT and telematics, which enhance operational safety, efficiency, and maintenance. In addition, the adoption of electric and hybrid-powered heavy lifting equipment is accelerating as industries aim to reduce emissions and comply with stricter environmental regulations. This shift is particularly evident in regions with aggressive sustainability targets, such as Europe and North America, where government policies and corporate ESG commitments are pushing the transition away from diesel-powered machinery. The integration of advanced battery systems, regenerative braking, and energy-efficient hydraulics is enabling companies to lower operational costs while enhancing environmental performance. Furthermore, innovations such as remote diagnostics, predictive maintenance, and telematics-enabled monitoring are making these machines safer and more productive, even in complex industrial settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25 Billion |

| Forecast Value | $44.6 Billion |

| CAGR | 5.8% |

The 100-250 tons crane segment held a 30.8% share in 2024. Cranes in this weight class play a vital role in medium to heavy lifting applications and are widely used in infrastructure expansion, mining operations, and large-scale industrial projects. With their strong balance between mobility and lifting strength, these cranes are ideal for complex tasks such as positioning bridge sections, installing wind turbines, and transporting oversized industrial equipment. Their adaptability to function in both densely populated urban zones and remote locations adds to their growing demand across a wide range of operational environments.

In 2024, the cranes segment generated USD 25 billion, underscoring its significance within the heavy lifting equipment sector. This segment includes a variety of specialized machines, such as crawler cranes, tower cranes, mobile cranes, gantry cranes, and overhead cranes, each tailored to serve distinct needs in industries like manufacturing, shipping, energy, and construction. These machines are engineered to deliver precise lifting capabilities, ensuring safe and efficient handling of heavy loads in demanding project conditions.

Asia-Pacific Heavy Lifting Equipment Market will grow at a CAGR of 6.5% through 2034, attributed to massive infrastructure development projects in China, India, and Southeast Asia, alongside increasing adoption of automation and semi-autonomous equipment to address labor shortages. The presence of both global and local players, combined with cost-efficient innovations, is accelerating market penetration in the region.

Key players shaping the Heavy Lifting Equipment Market include Tadano, Konecranes, Shanghai Zhenhua Heavy Industries (ZPMC), Sarens, Palfinger, SANY, Manitowoc Company, Sennebogen, Komatsu, Liebherr, Terex, Cargotec, Mammoet, JASO Industrial Cranes, and Demag Cranes & Components. These companies are investing in the development of smarter, safer, and greener lifting solutions to meet the evolving demands of industries worldwide. As digital transformation and environmental awareness continue to influence equipment purchasing decisions, the heavy lifting equipment market is poised for robust and sustained growth throughout the next decade.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Weight Capacity

- 2.2.4 End use industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing infrastructure development

- 3.2.1.2 Growth in mining and oil & gas sectors

- 3.2.1.3 Expansion of wind energy projects

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Skilled labour shortage

- 3.2.3 Opportunities

- 3.2.3.1 Infrastructure development in emerging economies

- 3.2.3.2 Automation and smart equipment integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code - 8428)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Cranes

- 5.2.1 Mobile cranes

- 5.2.1.1 All-terrain cranes

- 5.2.1.2 Crawler cranes

- 5.2.1.3 Rough terrain cranes

- 5.2.1.4 Truck-mounted cranes

- 5.2.2 Fixed cranes

- 5.2.2.1 Tower cranes

- 5.2.2.2 Overhead cranes

- 5.2.2.3 Gantry cranes

- 5.2.2.4 Monorail cranes

- 5.2.3 Marine & port cranes

- 5.2.1 Mobile cranes

- 5.3 Hoists

- 5.3.1 Electric hoists

- 5.3.2 Hydraulic hoists

- 5.3.3 Manual hoists

- 5.4 Transporters

- 5.4.1 Self-propelled modular transporters (SPMTS)

- 5.4.2 Heavy haul trailers

- 5.4.3 Specialized transport vehicles

Chapter 6 Market Estimates and Forecast, By Weight Capacity, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 100-250 Tons

- 6.3 251-500 Tons

- 6.4 501-1000 Tons

- 6.5 Above 1000 Tons

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Oil & gas

- 7.4 Mining

- 7.5 Shipping & port operations

- 7.6 Marine and Shipbuilding

- 7.6.1 Shipyard Operations

- 7.6.2 Offshore Construction

- 7.6.3 Vessel Maintenance and Repair

- 7.6.4 Naval Construction

- 7.7 Power generation

- 7.7.1 Conventional power

- 7.7.2 Renewable energy

- 7.8 Manufacturing

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Cargotec

- 10.2 Demag Cranes & Components

- 10.3 JASO Industrial Cranes

- 10.4 Komatsu

- 10.5 Konecranes

- 10.6 Liebherr

- 10.7 Mammoet

- 10.8 Manitowoc Company

- 10.9 Palfinger

- 10.10 SANY

- 10.11 Sarens

- 10.12 Sennebogen

- 10.13 Shanghai Zhenhua Heavy Industries (ZPMC)

- 10.14 Tadano

- 10.15 Terex

2026年全球重型自升式車輛市場報告

2026年全球重型自升式車輛市場報告 工業升降機市場:全球產品類型、動力來源、高度範圍、載重能力和應用預測 - 2026 年至 2032 年

工業升降機市場:全球產品類型、動力來源、高度範圍、載重能力和應用預測 - 2026 年至 2032 年 門升降器市場規模、佔有率和成長分析:按產品類型、負載能力、應用、最終用戶、分銷管道和地區分類 - 2026-2033 年行業預測2026年全球起重設備市場報告工業起重設備市場依產品類型、操作方式、起重能力、移動性、技術及最終用戶產業分類,全球預測(2026-2032)

門升降器市場規模、佔有率和成長分析:按產品類型、負載能力、應用、最終用戶、分銷管道和地區分類 - 2026-2033 年行業預測2026年全球起重設備市場報告工業起重設備市場依產品類型、操作方式、起重能力、移動性、技術及最終用戶產業分類,全球預測(2026-2032) 起重設備市場規模、佔有率和趨勢分析報告:按類型、機制、最終用途、地區和細分市場預測(2025-2033 年)

起重設備市場規模、佔有率和趨勢分析報告:按類型、機制、最終用途、地區和細分市場預測(2025-2033 年) 全球索具及吊索市場展望、詳細分析及至2031年預測

全球索具及吊索市場展望、詳細分析及至2031年預測 重型吊索:全球市場佔有率和排名、總收入和需求預測(2025-2031年)鋼絲繩吊索:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

重型吊索:全球市場佔有率和排名、總收入和需求預測(2025-2031年)鋼絲繩吊索:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 2032 年伸縮式升降機市場預測:按產品類型、機制類型、負載能力、分銷管道、應用、最終用戶和地區進行的全球分析

2032 年伸縮式升降機市場預測:按產品類型、機制類型、負載能力、分銷管道、應用、最終用戶和地區進行的全球分析