|

市場調查報告書

商品編碼

1844375

汽車駕駛監控系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Driver Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

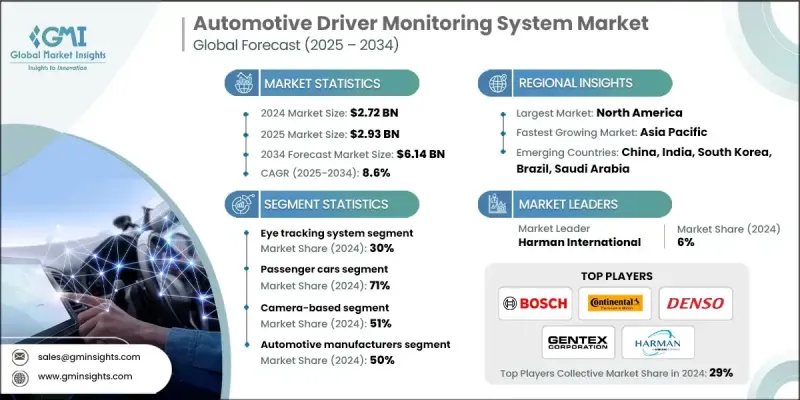

2024 年全球汽車駕駛監控系統市場價值為 27.2 億美元,預計到 2034 年將以 8.6% 的複合年成長率成長至 61.4 億美元。

隨著道路安全的日益重要以及半自動駕駛技術的快速發展,駕駛員監控系統 (DMS) 在現代車輛中的應用正在加速。這些系統透過分析頭部方向、眼球運動、眨眼速度和臉部表情等因素來評估駕駛者的行為和注意力。隨著全球安全標準的日益嚴格,DMS 正逐漸成為乘用車的關鍵功能,它不僅是一種可選的豪華配置,也是下一代車輛安全架構的核心要素。即時眼動追蹤、邊緣 AI 處理和紅外線夜視技術的進步正在增強系統功能,使其在不同的光照條件和使用者場景下都能獲得更佳的效能。開發人員也正在使用大型附註釋的資料集來改進 AI 模型,以提高檢測疲勞、分心或注意力不集中的準確性。除了私家車之外,DMS 技術也正在大力進軍商業車隊,在這些領域,管理駕駛員的警覺性在減少事故和提高對新興安全法規的合規性方面發揮著關鍵作用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 27.2億美元 |

| 預測值 | 61.4億美元 |

| 複合年成長率 | 8.6% |

眼動追蹤技術在2024年佔據了30%的市場佔有率,預計到2034年將以7.6%的複合年成長率成長。這些系統旨在監測眨眼時長、注視方向和瞳孔擴張等視覺線索,以評估駕駛員疲勞或注意力不集中的跡象。眼動追蹤仍然是識別注意力分散早期指標的最有效的生物辨識技術之一。研究模擬表明,該系統能夠捕捉眼球運動的細微變化,在低光源環境下或駕駛員佩戴眼鏡或遮光眼鏡時也能提供高精度檢測。

2024年,乘用車市場佔了71%的市場佔有率,預計2025年至2034年期間的複合年成長率將達到9%。這種主導地位的驅動力源自於不斷發展的安全協議和更嚴格的合規要求。全球市場(尤其是亞洲和歐洲)的監管變化正促使製造商將DMS納入其標準安全功能。這些框架強調疲勞檢測和行為監控,促使原始設備製造商將DMS嵌入其最新的乘用車車型中,以滿足最新的安全評分基準。

北美汽車駕駛監控系統市場佔33%的市場佔有率,2024年市場規模達8.939億美元。該地區的領先地位源於地方政府、原始設備製造商和運輸車隊對整合智慧駕駛輔助系統的大力推動。雖然DMS整合尚未強制要求所有車型都整合,但美國和加拿大的國家級項目和試點項目已積極推動其應用。這些努力旨在提高駕駛員意識,減少分心事故,並支持向更安全、更聰明的出行解決方案過渡。

全球汽車駕駛監控系統市場的主要參與者包括大陸集團、麥格納、電裝、哈曼、鏡泰、安波福、Tobii、博世和法雷奧。在汽車駕駛員監控系統市場中運作的公司正在利用策略合作夥伴關係,大力投資人工智慧和感測器技術,並將產品創新與監管框架相結合。許多公司正在與汽車製造商合作,共同開發將駕駛員監控系統 (DMS) 與高級駕駛輔助系統結合的整合安全平台。其他公司則透過即時眼動追蹤、邊緣運算和紅外線感測器功能增強其硬體產品,以提高各種駕駛條件下的可靠性。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預報

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 嚴格的政府安全法規

- 對 ADAS 和半自動駕駛汽車的需求不斷成長

- 分心駕駛和疲勞駕駛事件增多

- 消費者對車內安全功能的認知不斷提高

- 人工智慧和電腦視覺在汽車系統中的整合

- 商業車隊駕駛員監控規定

- 產業陷阱與挑戰

- DMS軟硬體整合成本高

- 用戶對隱私和生物特徵資料問題的擔憂

- 市場機會

- Euro NCAP 2026 和 GSR 第二階段強制使用 DMS

- 專為車內監控設計的人工智慧晶片組的出現

- 與居住者監測和健康分析整合

- 商業和共享出行車隊對 DMS 的需求不斷成長

- 成長動力

- 成長潛力分析

- 專利分析

- 波特的分析

- PESTEL分析

- 成本分解分析

- 技術和創新格局

- 當前的技術趨勢

- 電腦視覺演算法的演變

- 眼動追蹤技術進步

- 人工智慧和機器學習整合

- 多模態感測器融合

- 即時處理能力

- 新興技術

- 當前的技術趨勢

- 監管格局

- NHTSA 駕駛員監控要求

- Euro NCAP 安全評估協議

- 歐盟通用安全法規的影響

- ISO 26262 功能安全合規性

- GDPR 生物特徵資料保護

- 價格趨勢

- 按地區

- 按系統

- 永續性和 ESG 影響分析

- 生命週期環境評估

- 製造業永續性

- 臨終管理

- 減少碳足跡

- 投資與融資趨勢分析

- 安全和性能標準

- 汽車安全完整性等級(ASIL)

- 檢測精度要求

- 反應時間標準

- 環境測試協議

- 電磁相容性(EMC)

- 自動駕駛汽車整合

- SAE 特定等級要求

- 切換場景管理

- 駕駛員準備狀況評估

- 數位轉型的影響

- 連網汽車整合

- 無線更新功能

- 基於雲端的分析平台

- 巨量資料與人工智慧融合

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按系統,2021 - 2034

- 主要趨勢

- 眼動追蹤系統

- 臉部辨識系統

- 轉向行為監測系統

- 心率監測系統

- 其他

第6章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車

- 輕型商用車(LCV)

- 重型商用車(HCV)

- 中型商用車(MCV)

第7章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 基於攝影機

- 基於感測器

- 混合

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 汽車製造商

- OEM(原始設備製造商)

- 一級供應商

- 2/3級零件供應商

- 售後市場製造商

- 政府

- 交通運輸及安全機構

- 政府車隊

- 個人

- 車隊營運商

- 運輸與物流

- 行程服務

- 行業專用車隊

- 商業運輸

- 其他

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 菲律賓

- 泰國

- 韓國

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球參與者

- Aptiv

- Bosch

- Continental

- Denso

- Gentex

- Harman

- Magna

- Tobii

- Valeo

- 區域參與者

- Aisin

- Eyesight Technologies

- Ficosa

- Hyundai Mobis

- Panasonic

- Veoneer

- Visteon

- ZF Friedrichshafen

- 新興參與者/顛覆者

- Affectiva

- Cipia

- Eyeris Technologies

- Guardian Optical Technologies

- Jungo Connectivity

- Nauto

- StradVision

- Xperi Corporation

The Global Automotive Driver Monitoring System Market was valued at USD 2.72 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 6.14 billion by 2034.

The growing emphasis on road safety and the rapid advancement of semi-autonomous driving technologies are accelerating the adoption of driver monitoring systems (DMS) in modern vehicles. These systems evaluate driver behavior and attentiveness by analyzing factors such as head orientation, eye movement, blinking speed, and facial expressions. As safety standards tighten worldwide, DMS is emerging as a critical feature in passenger vehicles, not just as an optional luxury but as a core element of next-generation vehicle safety architecture. Advancements in real-time eye tracking, edge AI processing, and infrared-based night vision are enhancing system capabilities, allowing better performance across different lighting conditions and user scenarios. Developers are also refining AI models using large annotated datasets to increase the accuracy of detecting fatigue, distraction, or inattention. Beyond private vehicles, DMS technology is making significant inroads into commercial fleets, where managing driver alertness plays a pivotal role in reducing accidents and improving compliance with emerging safety regulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.72 Billion |

| Forecast Value | $6.14 Billion |

| CAGR | 8.6% |

The eye tracking technology segment held a 30% share in 2024 and is projected to grow at a CAGR of 7.6% through 2034. These systems are designed to monitor visual cues like blink duration, gaze direction, and pupil dilation to assess signs of driver fatigue or loss of focus. Eye tracking remains one of the most effective biometric techniques for identifying early indicators of distraction. Research simulations have demonstrated the system's ability to capture even subtle variations in eye movement, delivering high detection accuracy in low-light environments or when drivers wear glasses or obstructive eyewear.

The passenger cars segment held a 71% share in 2024 and is expected to grow at a 9% CAGR from 2025 to 2034. This dominance is driven by evolving safety protocols and tighter compliance requirements. Regulatory changes across global markets, especially in Asia and Europe, are pushing manufacturers to incorporate DMS as part of their standard safety features. These frameworks emphasize fatigue detection and behavioral monitoring, prompting OEMs to embed DMS into their latest passenger models to meet updated safety scoring benchmarks.

North America Automotive Driver Monitoring System Market held a 33% share and generated USD 893.9 million in 2024. The region's leadership stems from a strong push by regional authorities, OEMs, and transportation fleets seeking to integrate intelligent driver-assist systems. While DMS integration is not yet mandatory across all vehicle categories, national programs and pilot initiatives in both the US and Canada have actively promoted its adoption. These efforts focus on enhancing driver awareness, reducing distraction-related accidents, and supporting the transition to safer, smarter mobility solutions.

Key players in the Global Automotive Driver Monitoring System Market include Continental, Magna, Denso, Harman, Gentex, Aptiv, Tobii, Bosch, and Valeo. Companies operating in the automotive driver monitoring system market are leveraging strategic partnerships, investing heavily in AI and sensor technology, and aligning product innovation with regulatory frameworks. Many are forming collaborations with automakers to co-develop integrated safety platforms that combine DMS with advanced driver-assistance systems. Others are enhancing their hardware offerings with real-time eye tracking, edge-based computing, and infrared sensor capabilities to improve reliability across driving conditions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 End Use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent government safety regulations

- 3.2.1.2 Rising demand for ADAS and semi-autonomous vehicles

- 3.2.1.3 Increasing incidents of distracted and drowsy driving

- 3.2.1.4 Growing consumer awareness of in-cabin safety features

- 3.2.1.5 Integration of AI and computer vision in automotive systems

- 3.2.1.6 Mandates for commercial fleet driver monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of DMS hardware and software integration

- 3.2.2.2 Privacy and biometric data concerns among users

- 3.2.3 Market opportunities

- 3.2.3.1 Mandatory DMS for Euro NCAP 2026 and GSR Phase II

- 3.2.3.2 Emergence of AI chipsets tailored for in-cabin monitoring

- 3.2.3.3 Integration with occupant monitoring and health analytics

- 3.2.3.4 Growing demand for DMS in commercial and shared mobility fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 Computer vision algorithm evolution

- 3.8.1.2 Eye tracking technology advances

- 3.8.1.3 AI and machine learning integration

- 3.8.1.4 Multi-modal sensor fusion

- 3.8.1.5 Real-time processing capabilities

- 3.8.2 Emerging technologies

- 3.8.1 Current technological trends

- 3.9 Regulatory landscape

- 3.9.1 NHTSA driver monitoring requirements

- 3.9.2 Euro NCAP safety assessment protocols

- 3.9.3 EU general safety regulation impact

- 3.9.4 ISO 26262 functional safety compliance

- 3.9.5 GDPR biometric data protection

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By system

- 3.11 Sustainability & ESG impact analysis

- 3.11.1 Lifecycle environmental assessment

- 3.11.2 Manufacturing sustainability

- 3.11.3 End-of-life management

- 3.11.4 Carbon footprint reduction

- 3.12 Investment & funding trends analysis

- 3.13 Safety and performance standards

- 3.13.1 Automotive safety integrity levels (ASIL)

- 3.13.2 Detection accuracy requirements

- 3.13.3 Response time standards

- 3.13.4 Environmental testing protocols

- 3.13.5 Electromagnetic compatibility (EMC)

- 3.14 Autonomous vehicle integration

- 3.14.1 SAE level-specific requirements

- 3.14.2 Handover scenario management

- 3.14.3 Driver readiness assessment

- 3.15 Digital transformation impact

- 3.15.1 Connected vehicle integration

- 3.15.2 Over-the-air update capabilities

- 3.15.3 Cloud-based analytics platforms

- 3.15.4 Big data and AI integration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2021 - 2034 (USD Bn)

- 5.1 Key trends

- 5.2 Eye tracking system

- 5.3 Facial recognition system

- 5.4 Steering behavior monitoring system

- 5.5 Heart rate monitoring system

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Heavy commercial vehicles (HCV)

- 6.3.3 Medium commercial vehicles (MCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Bn)

- 7.1 Key trends

- 7.2 Camera-based

- 7.3 Sensor-based

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Bn)

- 8.1 Key trends

- 8.2 Automotive manufacturers

- 8.2.1 OEMs (Original Equipment Manufacturers)

- 8.2.2 Tier 1 suppliers

- 8.2.3 Tier 2/3 component suppliers

- 8.2.4 Aftermarket manufacturers

- 8.3 Government

- 8.3.1 Transportation & safety agencies

- 8.3.2 Government vehicle fleets

- 8.4 Individuals

- 8.5 Fleet operators

- 8.5.1 Transportation & logistics

- 8.5.2 Mobility services

- 8.5.3 Industry-specific fleets

- 8.5.4 Commercial transportation

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 Philippines

- 9.4.7 Thailand

- 9.4.8 South Korea

- 9.4.9 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aptiv

- 10.1.2 Bosch

- 10.1.3 Continental

- 10.1.4 Denso

- 10.1.5 Gentex

- 10.1.6 Harman

- 10.1.7 Magna

- 10.1.8 Tobii

- 10.1.9 Valeo

- 10.2 Regional Players

- 10.2.1 Aisin

- 10.2.2 Eyesight Technologies

- 10.2.3 Ficosa

- 10.2.4 Hyundai Mobis

- 10.2.5 Panasonic

- 10.2.6 Veoneer

- 10.2.7 Visteon

- 10.2.8 ZF Friedrichshafen

- 10.3 Emerging Players / Disruptors

- 10.3.1 Affectiva

- 10.3.2 Cipia

- 10.3.3 Eyeris Technologies

- 10.3.4 Guardian Optical Technologies

- 10.3.5 Jungo Connectivity

- 10.3.6 Nauto

- 10.3.7 StradVision

- 10.3.8 Xperi Corporation

汽車駕駛監控系統市場:按技術、組件、最終用戶、應用和車輛類型分類-2026-2032年全球市場預測

汽車駕駛監控系統市場:按技術、組件、最終用戶、應用和車輛類型分類-2026-2032年全球市場預測 2026年全球汽車固體硬碟市場報告2026年全球駕駛員監控系統市場報告困倦檢測設備市場:按類型、技術、最終用戶、應用和銷售管道- 全球預測 2026-2032 年

2026年全球汽車固體硬碟市場報告2026年全球駕駛員監控系統市場報告困倦檢測設備市場:按類型、技術、最終用戶、應用和銷售管道- 全球預測 2026-2032 年 駕駛員監控系統(DMS)市場:策略洞察與預測(2026-2031年)駕駛員和乘客監控系統市場:按組件、技術、車輛類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)全球汽車駕駛員監控系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球人員監控系統市場報告

駕駛員監控系統(DMS)市場:策略洞察與預測(2026-2031年)駕駛員和乘客監控系統市場:按組件、技術、車輛類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)全球汽車駕駛員監控系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球人員監控系統市場報告 乘員監控系統 (OMS) 市場規模、佔有率及預測:依感測器類型(攝影機、雷達、熱成像)、人工智慧演算法(兒童存在檢測、乘員體型檢測)、安全應用及車輛細分市場劃分-全球預測至 2036 年駕駛員監控系統(DMS)(人工智慧賦能)市場規模、佔有率及預測:依感測器類型(近紅外線攝影機、雷達)、人工智慧演算法(疲勞駕駛偵測、分心駕駛偵測、駕駛能力受損偵測)、監管狀態及OEM整合度劃分-全球預測至2036年

乘員監控系統 (OMS) 市場規模、佔有率及預測:依感測器類型(攝影機、雷達、熱成像)、人工智慧演算法(兒童存在檢測、乘員體型檢測)、安全應用及車輛細分市場劃分-全球預測至 2036 年駕駛員監控系統(DMS)(人工智慧賦能)市場規模、佔有率及預測:依感測器類型(近紅外線攝影機、雷達)、人工智慧演算法(疲勞駕駛偵測、分心駕駛偵測、駕駛能力受損偵測)、監管狀態及OEM整合度劃分-全球預測至2036年