|

市場調查報告書

商品編碼

1844369

再生鼓風機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Regenerative Blower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

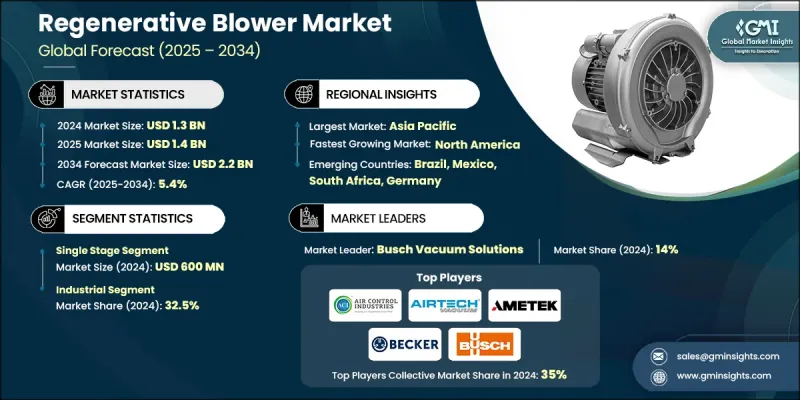

2024 年全球再生鼓風機市場價值為 13 億美元,預計到 2034 年將以 5.4% 的複合年成長率成長至 22 億美元。

需求的成長主要源自於自動化技術的快速發展以及自動化系統在各領域的廣泛應用。再生鼓風機因其在冷卻、物料處理、乾燥和氣力輸送等基本功能中發揮重要作用,已成為這些環境中的關鍵部件。其無油、穩定的氣流和低維護需求使其在高性能工業環境中備受青睞。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 22億美元 |

| 複合年成長率 | 5.4% |

再生鼓風機設計和工程的持續創新顯著提高了效率、性能和多功能性。增強型材料和智慧控制系統已將其應用擴展到成熟和新興領域。清潔能源系統、積層製造和先進氣動處理等新興領域的應用進一步推動了其應用。在這些場景中,再生鼓風機可提供精確的空氣流動、節能和無污染運行,使其成為現代製造業和注重環保的行業的理想選擇。其價值主張不僅在於營運效率,還在於促進永續生產和降低營運風險。

單級鼓風機市場在2024年達到6億美元,這得益於其在重型和輕型工業應用中的廣泛應用。這些鼓風機在需要穩定氣流的系統中至關重要,支援諸如化學品攪拌、燃燒空氣輸送、除塵、抽吸應用和氣刀吹掃等任務。其廣泛應用歸因於其能夠以最低的複雜性提供高可靠性,從而支援正常運行時間並降低營運成本。

2024年,工業應用領域佔了32.5%的市場佔有率,凸顯了再生鼓風機在重工業中的重要性。這些系統專為需要高流量和壓力穩定性的操作而設計。這些鼓風機通常用於廢水管理、氣動輸送和曝氣等領域,在保持無油運轉的同時提供高效的性能,這對於必須避免產品或製程污染的環境至關重要。

隨著美國國內各行各業紛紛採用自動化和節能解決方案,2024年美國再生式鼓風機市場佔了76%的市場。隨著排放、工作場所安全和設備噪音水平的監管力度不斷加強,促使人們轉向更安靜、更智慧的鼓風機技術。美國製造商正透過提供具有更高效率、數位整合和先進變速功能的鼓風機來滿足這一需求。這些發展與智慧製造和工業製程控制領域對精密氣流系統日益成長的需求相契合。

全球再生鼓風機市場的主要參與者包括 Airtech Vacuum Incorporated、Goorui、The Spencer Turbine Company、FPZ SpA、Hitachi Ltd.、Eurus Blowers、Becker Pump Corporation、Gardner Denver Holdings, Inc.、Air Control Industries Ltd.、Buschity SE / Busch Vacuum Solutions、Gast Maners Ltd.、Busch) KNB Corporation。參與再生鼓風機市場競爭的公司正專注於創新、客製化和能源效率,以鞏固其在全球市場的地位。許多公司正在投資整合物聯網功能、遠端診斷和先進控制系統的智慧鼓風機技術。策略合作夥伴關係和收購正在幫助製造商擴大產品組合,同時提高供應鏈的彈性。各公司也強調研發,以開發適用於清潔能源和自動化驅動應用的降噪、無油鼓風機。生產設施的本地化和客製化服務正被用於滿足特定地區的需求。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 工業自動化需求不斷成長

- 促進能源效率的環境法規

- 擴大廢水處理與空氣處理應用

- 產業陷阱與挑戰

- 製造和維護成本壓力大

- 替代解決方案的技術取代

- 機會

- 與智慧監控系統整合

- 新興市場和基礎建設發展

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依階段類型,2021-2034

- 主要趨勢

- 單階段

- 兩階段

- 三階段

第6章:市場估計與預測:依壓力範圍,2021-2034

- 主要趨勢

- 低壓(最高 1 巴)

- 中壓(1至2巴)

- 高壓(超過 2 巴)

第7章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 水和廢水

- 食品和飲料

- 工業的

- 化學

- 石油和天然氣

- 醫療的

第 8 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直銷

- 間接銷售

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Air Control Industries Ltd.

- Airtech Vacuum Incorporated

- Atlantic Blowers

- Ametek Inc.

- Becker Pump Corporation

- Busch SE / Busch Vacuum Solutions

- Eurus Blowers

- FPZ SpA

- Gardner Denver Holdings, Inc.

- Gast Manufacturing, Inc.

- Goorui

- Hitachi Ltd.

- KNB Corporation

- Rietschle Thomas

- The Spencer Turbine Company

The Global Regenerative Blower Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 2.2 billion by 2034.

Rising demand is largely fueled by the rapid advancement of automation and the widespread implementation of automated systems across diverse sectors. Regenerative blowers have become a key component in these environments due to their role in supporting essential functions like cooling, material handling, drying, and pneumatic conveying. Their oil-free, consistent airflow and low maintenance needs make them highly favored in high-performance industrial settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.4% |

Continued innovation in regenerative blower design and engineering has significantly improved efficiency, performance, and versatility. Enhanced materials and intelligent control systems have expanded their use across both established and emerging sectors. Applications in newer fields such as clean energy systems, additive manufacturing, and advanced pneumatic handling are further driving adoption. In these scenarios, regenerative blowers provide precise air movement, energy savings, and contamination-free operation, making them ideal for modern manufacturing and environmentally focused industries. Their value proposition lies not only in operational efficiency but also in contributing to sustainable production and lower operational risks.

The single-stage segment accounted for USD 600 million in 2024 owing to its extensive use in both heavy-duty and light industrial applications. These blowers are essential in systems where consistent airflow is required, supporting tasks like chemical agitation, combustion air delivery, dust removal, suction applications, and air knife blow-offs. Their widespread use is attributed to their ability to deliver high reliability with minimal complexity, which supports uptime and lowers operational costs.

The industrial application segment held a 32.5% share in 2024, highlighting the importance of regenerative blowers in heavy industries. These systems are tailored for operations that demand both high flow rates and pressure stability. Commonly used in sectors such as wastewater management, pneumatic transport, and aeration, these blowers provide efficient performance while maintaining oil-free operation, which is critical for environments where product or process contamination must be avoided.

United States Regenerative Blower Market held a 76% share in 2024 as domestic industries embraced automation and energy-efficient solutions. Increased regulatory scrutiny around emissions, workplace safety, and equipment noise levels has encouraged the shift toward quieter, smarter blower technologies. U.S. manufacturers are addressing this demand by delivering blowers with enhanced efficiency, digital integration, and advanced variable speed capabilities. These developments align with the growing need for precision airflow systems in smart manufacturing and industrial process control.

Key players in the Global Regenerative Blower Market include Airtech Vacuum Incorporated, Goorui, The Spencer Turbine Company, FPZ SpA, Hitachi Ltd., Eurus Blowers, Becker Pump Corporation, Gardner Denver Holdings, Inc., Air Control Industries Ltd., Busch SE / Busch Vacuum Solutions, Gast Manufacturing, Inc., Atlantic Blowers, Rietschle Thomas, Ametek Inc., and KNB Corporation. Companies competing in the Regenerative Blower Market are focusing on innovation, customization, and energy efficiency to solidify their presence across global markets. Many are investing in smart blower technologies that integrate IoT features, remote diagnostics, and advanced control systems. Strategic partnerships and acquisitions are helping manufacturers expand product portfolios while improving supply chain resilience. Firms are also emphasizing R&D to develop noise-reduced, oil-free blowers suitable for clean energy and automation-driven applications. Localization of production facilities and tailored service offerings are being used to address region-specific needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type trends

- 2.2.3 Method trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for industrial automation

- 3.2.1.2 Environmental regulations promoting energy efficiency

- 3.2.1.3 Expansion of wastewater treatment and air handling applications

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Cost pressure due to high manufacturing and maintenance

- 3.2.2.2 Technological displacement by alternative solutions

- 3.2.3 Opportunities

- 3.2.3.1 Integration with smart monitoring systems

- 3.2.3.2 Emerging markets and infrastructure development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Stage Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Single staged

- 5.3 Two-staged

- 5.4 Three-staged

Chapter 6 Market Estimates and Forecast, By Pressure Range, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low pressure (up to 1 bar)

- 6.3 Medium pressure (1 to 2 bar)

- 6.4 High pressure (more than 2 bar)

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Water and wastewater

- 7.3 Food & beverage

- 7.4 Industrial

- 7.5 Chemical

- 7.6 Oil & gas

- 7.7 Medical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Air Control Industries Ltd.

- 10.2 Airtech Vacuum Incorporated

- 10.3 Atlantic Blowers

- 10.4 Ametek Inc.

- 10.5 Becker Pump Corporation

- 10.6 Busch SE / Busch Vacuum Solutions

- 10.7 Eurus Blowers

- 10.8 FPZ SpA

- 10.9 Gardner Denver Holdings, Inc.

- 10.10 Gast Manufacturing, Inc.

- 10.11 Goorui

- 10.12 Hitachi Ltd.

- 10.13 KNB Corporation

- 10.14 Rietschle Thomas

- 10.15 The Spencer Turbine Company

全球再生式鼓風機市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球再生式鼓風機市場規模、佔有率、趨勢和成長分析報告(2026-2034) 渦流鼓風機市場規模、佔有率及成長分析(按產品類型、級數類型、壓力、分佈、最終用戶和地區分類)-產業預測(2026-2033)

渦流鼓風機市場規模、佔有率及成長分析(按產品類型、級數類型、壓力、分佈、最終用戶和地區分類)-產業預測(2026-2033) 渦流鼓風機的全球市場

渦流鼓風機的全球市場