|

市場調查報告書

商品編碼

1844341

注塑機市場機會、成長動力、產業趨勢分析及2025-2034年預測Injection Molding Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

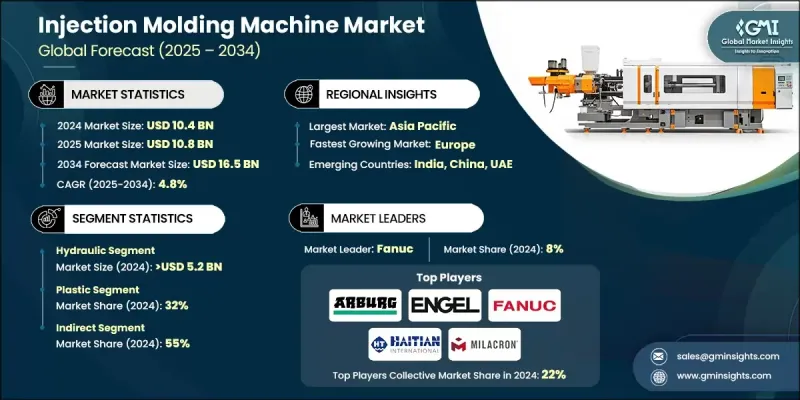

2024 年全球注塑機市場價值為 104 億美元,預計到 2034 年將以 4.8% 的複合年成長率成長至 165 億美元。

市場成長的動力來自於各主要製造業對輕量化和高性能塑膠零件日益成長的需求。各行各業正在轉向能夠提高效率和降低營運成本的材料。例如,在運輸和航太,更輕的零件意味著更好的燃油經濟性並減少排放。注塑機在這裡發揮著至關重要的作用,它在生產既耐用又輕便的複雜零件時提供精確度和可重複性。隨著最終用途應用的設計密集度越來越高,製造商正在轉向提供更高精度、更快循環時間以及與新型聚合物相容的機器。對完美產出和快速交付的日益重視使得新一代機器成為必不可少的升級。該公司現在正在投資能夠處理複雜模具和各種材料的先進技術,確保可靠的性能和最大限度地減少缺陷。使用複雜輕質材料的趨勢繼續塑造對尖端注塑機的需求,使其成為現代製造策略的基本組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 104億美元 |

| 預測值 | 165億美元 |

| 複合年成長率 | 4.8% |

2024年,液壓注塑機市場規模達到52億美元,預計2034年將以4.8%的複合年成長率成長。由於可靠性高且初始成本較低,這類機器仍受到生產更大、更重部件的青睞。儘管成長速度適中,但由於應用廣泛,它們仍佔據著強勁地位。然而,電動注塑機正日益受到青睞,其優勢包括更高的能源效率、更高的精度、更低的噪音水平和更低的維護要求,這些優勢吸引了注重永續性和營運效率的製造商。

2024年,塑膠材料市場佔據32%的市場佔有率,預計2025年至2034年的複合年成長率為4.4%。塑膠持續佔據主導地位,得益於其多功能性、易成型性以及在消費品、包裝和汽車零件等應用領域日益成長的需求。塑膠的輕量化和成本效益使其成為產品設計和量產對獲利能力至關重要的行業的首選。

美國注塑機市場佔76%的市場佔有率,2024年市場規模達21.5億美元。該地區的成長與醫療保健、汽車和包裝等行業密切相關,這些行業正轉向輕量化、精密的塑膠零件。越來越多的企業正在用現代化的機器替換老舊設備,以提高生產力和產品品質。電動和混合動力機器的普及率激增,反映了自動化和效率在該地區製造業中日益重要的角色。

推動全球注塑機產業進步的關鍵參與者包括米拉克龍、海天國際、恩格爾、JSW、克勞斯瑪菲、伊之密、發那科、日精樹脂工業、住友、芝浦機械、東洋機械金屬、威猛巴頓菲爾、阿博格、赫斯基注塑系統和震雄控股。這些公司始終專注於創新、自動化和系統整合。注塑機市場的頂尖公司專注於採用智慧製造技術和自動化來提高生產效率。對節能和全電動車型的投資大幅成長,滿足了對永續解決方案日益成長的需求。企業正在不斷擴展其產品線以支援複雜的應用,特別是在醫療設備和電子產品等高精度領域。策略夥伴關係和協作有助於企業針對特定區域需求開發在地化解決方案。關鍵參與者還在升級數位介面、整合物聯網並提供遠端監控功能,以提供更好的機器診斷並減少停機時間。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 對輕量複雜塑膠零件的需求

- 對更快生產和效率的需求日益成長

- 產業陷阱與挑戰

- 初期投資和營運成本高

- 熟練勞動力短缺

- 機會

- 採用工業4.0和智慧製造

- 電動和混合動力注塑機的成長

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按機器類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依機器類型,2021 - 2034 年

- 主要趨勢

- 油壓

- 電的

- 混合

第6章:市場估計與預測:按材料類型,2021 - 2034 年

- 主要趨勢

- 塑膠

- 橡皮

- 金屬

- 陶瓷製品

第7章:市場估計與預測:按營運,2021 - 2034

- 主要趨勢

- 自動的

- 半自動

- 手動的

第8章:市場估計與預測:按注射壓力,2021 - 2034 年

- 主要趨勢

- 低於 1000 巴

- 1000-2500巴之間

- 2500巴以上

第9章:市場估計與預測:依產能,2021 - 2034

- 主要趨勢

- 500噸以下

- 500-1000噸之間

- 1000噸以上

第 10 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 汽車與運輸

- 建造

- 消費品

- 包裝

- 電氣和電子產品

第 11 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 直銷

- 間接銷售

第 12 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- Arburg

- Chen Hsong Holdings

- ENGEL

- Fanuc

- Haitian International

- Husky Injection Molding Systems

- JSW

- KraussMaffei

- Milacron

- Nissei Plastic Industrial

- Shibaura Machine

- Sumitomo

- Toyo Machinery & Metal

- Wittmann Battenfeld

- Yizumi

The Global Injection Molding Machine Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 16.5 billion by 2034.

Market growth is propelled by the increasing demand for lightweight and high-performance plastic components across key manufacturing sectors. Industries are shifting toward materials that enhance efficiency and cut down on operational costs. In transportation and aerospace, for instance, lighter parts translate into better fuel economy and reduced emissions. Injection molding machines play a critical role here, offering precision and repeatability in producing complex parts that are both durable and lightweight. As end-use applications become more design-intensive, manufacturers are turning to machines that offer higher precision, faster cycle times, and compatibility with newer polymers. The growing emphasis on flawless output and rapid delivery has made newer-generation machines an essential upgrade. Companies are now investing in advanced technologies that can handle intricate molds and varied materials, ensuring reliable performance and minimized defects. The trend toward using complex, lightweight materials continues to shape the demand for cutting-edge injection molding machinery, making it a fundamental part of modern manufacturing strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $16.5 Billion |

| CAGR | 4.8% |

The hydraulic injection molding machines segment reached USD 5.2 billion in 2024 and is expected to grow at a CAGR of 4.8% through 2034. These machines remain favored for producing larger and heavier components due to their reliability and lower initial cost. Although their growth is moderate, they still hold a strong position due to widespread usage. However, electric injection molding machines are gaining traction, offering benefits like improved energy efficiency, higher accuracy, reduced noise levels, and lower maintenance requirements, which appeal to manufacturers focused on sustainability and operational efficiency.

The plastic materials segment held a 32% share in 2024 and is forecast to grow at a CAGR of 4.4% from 2025 to 2034. The continued dominance of plastic is tied to its versatility, ease of molding, and rising demand across applications like consumer goods, packaging, and automotive components. Its lightweight nature and cost-effectiveness make it the go-to choice in industries where product design and mass production play a critical role in profitability.

U.S. Injection Molding Machine Market held a 76% share and generated USD 2.15 billion in 2024. The growth in this region is closely linked to industries such as healthcare, automotive, and packaging that are shifting toward lightweight, precision plastic parts. Companies are increasingly replacing older equipment with modern machines that improve productivity and output quality. The surge in adoption of electric and hybrid machines reflects the expanding role of automation and efficiency in manufacturing across the region.

Key players driving advancements in the Global Injection Molding Machine Industry include Milacron, Haitian International, ENGEL, JSW, KraussMaffei, Yizumi, Fanuc, Nissei Plastic Industrial, Sumitomo, Shibaura Machine, Toyo Machinery & Metal, Wittmann Battenfeld, Arburg, Husky Injection Molding Systems, and Chen Hsong Holdings. These companies are consistently focused on innovation, automation, and system integration. Top companies in the injection molding machine market are focused on adopting smart manufacturing technologies and automation to improve production efficiency. Investment in energy-efficient and all-electric models has grown significantly, meeting increasing demand for sustainable solutions. Firms are continuously expanding their product lines to support complex applications, especially in high-precision sectors like medical devices and electronics. Strategic partnerships and collaborations help companies develop localized solutions for specific regional demands. Key players are also upgrading digital interfaces, integrating IoT, and offering remote monitoring capabilities to provide better machine diagnostics and reduce downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machine type

- 2.2.3 Material type

- 2.2.4 Operation

- 2.2.5 Injection pressure

- 2.2.6 Capacity

- 2.2.7 End use

- 2.2.8 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for lightweight and complex plastic parts

- 3.2.1.2 Growing need for faster production and efficiency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and operational costs

- 3.2.2.2 Skilled labor shortage

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of industry 4.0 and smart manufacturing

- 3.2.3.2 Growth in electric and hybrid injection molding machines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By machine type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade Statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Hydraulic

- 5.3 Electric

- 5.4 Hybrid

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Rubber

- 6.4 Metal

- 6.5 Ceramic

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

- 7.4 Manual

Chapter 8 Market Estimates & Forecast, By Injection Pressure, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Below 1000 Bar

- 8.3 Between 1000-2500 Bar

- 8.4 Above 2500 Bar

Chapter 9 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Below 500 tons

- 9.3 Between 500-1,000 tons

- 9.4 Above 1,000 tons

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Automotive & Transportation

- 10.3 Construction

- 10.4 Consumer Goods

- 10.5 Packaging

- 10.6 Electrical & electronics

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Arburg

- 13.2 Chen Hsong Holdings

- 13.3 ENGEL

- 13.4 Fanuc

- 13.5 Haitian International

- 13.6 Husky Injection Molding Systems

- 13.7 JSW

- 13.8 KraussMaffei

- 13.9 Milacron

- 13.10 Nissei Plastic Industrial

- 13.11 Shibaura Machine

- 13.12 Sumitomo

- 13.13 Toyo Machinery & Metal

- 13.14 Wittmann Battenfeld

- 13.15 Yizumi

微型射出成型機市場:2026-2032年全球市場預測(夾緊力、機器類型、加工材料、成型方向、自動化程度、注射量、模腔數、應用及使用者類型分類)射出成型機市場:依型號、產品類型、機械零件、最終用戶和銷售管道分類-2026年至2032年全球市場預測外行程肘射出成型成型機市場:按機器類型、扣夾力、驅動系統、材料、注塑單元類型和最終用途行業分類,全球預測,2026-2032年PVC管件射出成型機市場:依機器類型、扣夾力、螺桿直徑、自動化程度、應用、終端用戶產業分類,全球預測,2026-2032年塑膠射出成型機械臂市場:按機器人類型、驅動類型、軸配置、有效載荷能力、應用、最終用戶產業分類,全球預測(2026-2032年)射出成型機市場:依應用、機器類型、扣夾力、加工材料、驅動系統、控制系統、螺桿直徑分類,全球預測,2026-2032年雙片式射出成型成型機市場:按驅動系統、扣夾力、材料類型、螺桿類型和應用分類-全球預測,2026-2032年

微型射出成型機市場:2026-2032年全球市場預測(夾緊力、機器類型、加工材料、成型方向、自動化程度、注射量、模腔數、應用及使用者類型分類)射出成型機市場:依型號、產品類型、機械零件、最終用戶和銷售管道分類-2026年至2032年全球市場預測外行程肘射出成型成型機市場:按機器類型、扣夾力、驅動系統、材料、注塑單元類型和最終用途行業分類,全球預測,2026-2032年PVC管件射出成型機市場:依機器類型、扣夾力、螺桿直徑、自動化程度、應用、終端用戶產業分類,全球預測,2026-2032年塑膠射出成型機械臂市場:按機器人類型、驅動類型、軸配置、有效載荷能力、應用、最終用戶產業分類,全球預測(2026-2032年)射出成型機市場:依應用、機器類型、扣夾力、加工材料、驅動系統、控制系統、螺桿直徑分類,全球預測,2026-2032年雙片式射出成型成型機市場:按驅動系統、扣夾力、材料類型、螺桿類型和應用分類-全球預測,2026-2032年 微型射出成型機市場分析及預測(至2035年):依類型、產品類型、應用、技術、材料類型、製程、最終用戶、組件及功能分類

微型射出成型機市場分析及預測(至2035年):依類型、產品類型、應用、技術、材料類型、製程、最終用戶、組件及功能分類 全球射出成型機市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球立式射出成型機市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球射出成型機市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球立式射出成型機市場規模、佔有率、趨勢及成長分析報告(2026-2034年)