|

市場調查報告書

商品編碼

1844335

皮卡車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Pickup Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

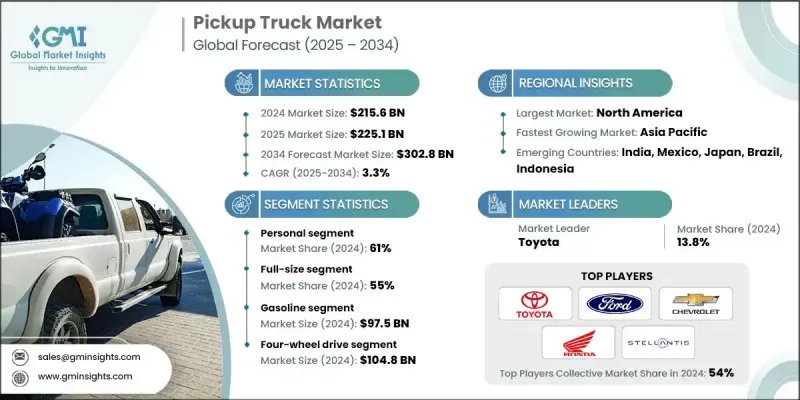

2024 年全球皮卡市場價值為 2,156 億美元,預計將以 3.3% 的複合年成長率成長,到 2034 年達到 3,028 億美元。

作為全球汽車產業的重要細分市場,皮卡在個人、商業、工業和休閒領域持續受到青睞。消費者越來越青睞那些兼具實用性和日常實用性的皮卡,它們集空間、堅固性和舒適性於一身。隨著人們對電動和混合動力車型的興趣日益濃厚,皮卡細分市場也在不斷發展。這些車型的勢頭強勁,不僅是因為環保法規的訂定,還源於創新和日益成長的消費者興趣。汽車製造商正在整合高階舒適性、資訊娛樂和先進的安全系統,同時保持強大的牽引力和有效載荷能力,這使得皮卡對家庭和車隊車主都極具吸引力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2156億美元 |

| 預測值 | 3028億美元 |

| 複合年成長率 | 3.3% |

業界正經歷向電動車的重大轉變,製造商紛紛加大對電動車技術的投入,以應對環保目標和未來的監管要求。為了因應全產業的顛覆性變革,許多公司也建立了合作聯盟,以降低開發成本並簡化供應鏈。這些合作促成了連網技術、電氣化和多功能設計功能的融合,從而提升了客戶參與度,並適應了快速變化的汽車市場格局。

2024年,個人用途皮卡佔據了61%的市場佔有率,並將以3%的複合年成長率持續成長,直至2034年。這一領先地位的驅動力源於市場對能夠輕鬆應對通勤、家庭出行和戶外生活方式的多功能車輛日益成長的需求。買家追求性能卓越且兼顧便捷性的皮卡,這促使製造商在其高階車型中引入豪華內飾、觸控螢幕控制、智慧安全功能和頂級資訊娛樂系統。這些不斷變化的偏好正在重塑皮卡的形象,使其從單純的實用型車輛轉變為功能全面的日常生活方式用車。

全尺寸皮卡市場在2024年佔據了55%的市場佔有率,預計在2025年至2034年期間的複合年成長率將達到2.6%。全尺寸皮卡因其強大的動力、寬敞的空間和強大的牽引力而廣受青睞。製造商正在升級這些車型,為其配備電動車傳動系統和專屬內飾,提供客製化功能、更廣泛的續航里程和更先進的性能套件。全尺寸皮卡豪華內裝的吸引力提升了客戶的期望,促使原始設備製造商開發全面的擁有體驗,包括更便捷的體驗、忠誠度獎勵和數位優先的服務解決方案。

美國皮卡市場佔90%的市場佔有率,2024年市場規模達998億美元。由於消費者普遍偏好全尺寸卡車的文化和功能性,皮卡仍然是美國最暢銷的汽車類別。個人和休閒用途顯著成長,消費者對高規格電動車型的需求持續飆升。汽車製造商正在推出先進的車型和科技含量更高的內飾,以在吸引新客戶的同時留住忠實用戶。

在全球皮卡市場積極競爭的主要公司包括日產、Stellantis(Ram Trucks)、福特、Alpha Motor、豐田、本田、雪佛蘭、GMC、Bollinger 和 Canoo。為了保持和加強其在競爭激烈的皮卡市場中的地位,領先的製造商正在推行多項戰略舉措。他們大力投資電動車平台和電池技術,以符合環境法規和客戶對永續旅行的期望。同時,該公司正在擴展產品線,推出針對特定客戶生活方式的豪華型和性能型裝飾。策略聯盟和合資企業在加速產品開發、最佳化生產和增強供應鏈彈性方面發揮作用。此外,許多參與者正在建立直接面對消費者的數位零售平台並增強售後服務,以提高客戶忠誠度和長期參與度。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 製造商

- 經銷商

- 最終用途

- 成本結構

- 利潤率

- 每個階段的增值

- 影響供應鏈的因素

- 破壞者

- 供應商格局

- 對部隊的影響

- 成長動力

- 基礎設施擴張刺激皮卡需求

- 技術進步提高了皮卡車的效率和安全性

- 政府對交通基礎設施的投資刺激了需求

- 採礦業成長推動皮卡車銷量

- 產業陷阱與挑戰

- 經濟衰退減少了建築和採礦活動

- 嚴格的排放法規增加了製造成本

- 市場機會

- 電動和混合動力皮卡的普及率不斷上升

- 智慧車隊管理和遠端資訊處理整合

- 成長動力

- 技術趨勢與創新生態系統

- 現有技術

- 動力總成技術演變

- 電動皮卡的電池技術

- 自動駕駛整合

- 連接和資訊娛樂系統

- 高級駕駛輔助系統(ADAS)

- 新興技術

- 輕質材料和結構

- 製造技術進步

- 充電基礎設施建設

- 車輛到電網(V2G)技術

- 無線 (OTA) 更新功能

- 現有技術

- 成長潛力分析

- 監管格局

- CAFE燃油經濟性標準

- EPA排放法規

- NHTSA安全標準

- 州級零排放汽車強制規定

- 商用車輛法規

- 未來監理趨勢

- 價格趨勢分析

- 各細分市場的歷史價格演變

- 區域價格差異

- 裝飾級別定價策略

- 電動車與內燃機汽車價格平價時間表

- 車隊與零售定價動態

- 選項和配件定價

- 產銷統計

- 全球產能分析

- 製造工廠利用率

- 各車型銷售趨勢

- 季節性銷售模式

- 庫存管理分析

- 生產彈性評估

- 供應鏈交付週期

- 成本分解分析

- 車輛開發成本

- 製造成本結構

- 材料成本分析

- 勞動成本評估

- 技術整合成本

- 監理合規成本

- 專利與創新分析

- 動力總成技術專利

- 電動車專利

- 自動駕駛專利

- 輕質結構專利

- 製造製程專利

- OEM專利組合分析

- 波特的分析

- PESTEL分析

- 永續性和環境方面

- 環境影響評估與生命週期分析

- 社會影響力和社區關係

- 治理與企業責任

- 永續技術發展

- 投資格局分析

- OEM資本投資模式

- 電動車投資

- 製造設施投資

- 研發投資分配

- 合資和合作投資

- 客戶行為分析

- 購買決策因素

- 品牌忠誠度模式

- 使用模式分析

- 更換週期趨勢

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依規模,2021 - 2034

- 主要趨勢

- 袖珍的

- 中型

- 全尺寸

第6章:市場估計與預測:按動力傳動系統,2021 - 2034 年

- 主要趨勢

- 汽油

- 柴油引擎

- 電的

- 混合

第7章:市場估計與預測:依牽引能力,2021 - 2034 年

- 主要趨勢

- 輕型牽引皮卡車(最高 7,500 磅)

- 中型牽引皮卡車(7,501-12,000磅)

- 重型牽引皮卡車(12,001 磅以上)

第8章:市場估計與預測:按驅動力,2021 - 2034

- 主要趨勢

- 後輪驅動

- 全輪驅動

- 四輪驅動

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 個人的

- 商業的

- 建築和重型設備

- 農業和耕作

- 園藝與戶外服務

- 公用事業和市政用途

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- Ford

- GMC

- Stellantis (Ram Trucks)

- Toyota

- Nissan

- Honda

- Rivian Automotive

- Tesla

- Isuzu Motors

- Mahindra & Mahindra

- Chevrolet

- 區域參與者

- Great Wall Motors

- Canoo

- Alpha Motor

- Bollinger

- SAIC Motor

- Tata Motors

- Volkswagen Commercial Vehicles

- Mitsubishi Motors

- Hyundai Motor Company

- JAC Motors

- Foton Motor

- SsangYong Motor

- Changan Automobile

- 新興企業

- Lordstown Motors

- Atlis Motor Vehicles

- Fisker

- Hercules Electric Vehicles

- Nikola

- Workhorse

- XOS

The Global Pickup Truck Market was valued at USD 215.6 billion in 2024 and is estimated to grow at a CAGR of 3.3% to reach USD 302.8 billion by 2034.

As a critical segment within the global automotive industry, pickup trucks continue to gain traction across personal, commercial, industrial, and recreational applications. Consumers are increasingly drawn to trucks that blend utility and everyday usability, offering space, ruggedness, and comfort in one package. The segment is evolving with rising interest in electric and hybrid-powered options, which are gaining momentum not just because of environmental regulations but also due to innovation and growing buyer interest. Automakers are integrating high-end comfort, infotainment, and advanced safety systems while maintaining strong towing and payload capabilities, making pickups appealing to both families and fleet owners.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $215.6 Billion |

| Forecast Value | $302.8 Billion |

| CAGR | 3.3% |

The industry has seen a major shift toward electric mobility, with manufacturers channeling investments into EV technology to address environmental goals and future regulatory requirements. In response to industry-wide disruptions, many companies also established collaborative alliances to reduce development expenses and streamline supply chains. These partnerships resulted in the integration of connected tech, electrification, and versatile design features, driving customer engagement and adapting to the fast-changing auto landscape.

In 2024, the personal-use category held 61% share and will grow at a CAGR of 3% through 2034. This leadership is driven by rising demand for multipurpose vehicles that can handle commuting, family travel, and outdoor lifestyles with ease. Buyers are looking for performance-driven trucks that don't sacrifice convenience, leading manufacturers to introduce luxury-grade interiors, touchscreen controls, smart safety features, and top-tier infotainment in their higher-end variants. These evolving preferences are reshaping the image of pickup trucks from utilitarian machines to well-rounded, daily-use lifestyle vehicles.

The full-size pickup segment held a 55% share in 2024 and is forecasted to grow at a CAGR of 2.6% between 2025 and 2034. Full-size pickups are widely preferred for their strength, space, and towing capabilities. Manufacturers are upgrading these models with EV drivetrains and exclusive trims offering customized features, expanded range, and sophisticated performance packages. The appeal of luxury trims in full-size pickups has elevated customer expectations, pushing OEMs to develop comprehensive ownership experiences with added convenience, loyalty perks, and digital-first service solutions.

U.S. Pickup Truck Market held 90% share and generated USD 99.8 billion in 2024. The segment remains the country's best-selling vehicle category, due to a widespread cultural and functional preference for full-size trucks. Personal and recreational usage has grown significantly, and consumer appetite for high-spec, electrified models continues to surge. Automakers are launching advanced variants and tech-rich trims to retain loyalty while attracting new audiences.

Major companies actively competing in the Global Pickup Truck Market include Nissan, Stellantis (Ram Trucks), Ford, Alpha Motor, Toyota, Honda, Chevrolet, GMC, Bollinger, and Canoo. To maintain and strengthen their positions in the competitive pickup truck market, leading manufacturers are pursuing multiple strategic initiatives. They are heavily investing in electrified vehicle platforms and battery technology to align with environmental regulations and customer expectations for sustainable mobility. Simultaneously, companies are expanding product lines with luxury-oriented and performance-driven trims tailored for specific customer lifestyles. Strategic alliances and joint ventures are playing a role in accelerating product development, optimizing production, and enhancing supply chain resilience. Additionally, many players are building direct-to-consumer digital retail platforms and enhancing aftersales service offerings to improve customer loyalty and long-term engagement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.6.1.1 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Size

- 2.2.3 Power Train

- 2.2.4 Towing Capability

- 2.2.5 Drive

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Manufacturer

- 3.1.1.3 Distributor

- 3.1.1.4 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure expansion fuels demand for pickup trucks

- 3.2.1.2 Technological advancements enhance pickup truck efficiency and safety

- 3.2.1.3 Government investments in transportation infrastructure spur demand

- 3.2.1.4 Mining sector growth boosts pickup truck sales

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Economic downturns reduce construction and mining activities

- 3.2.2.2 Stringent emissions regulations increase manufacturing costs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of electric and hybrid pickup trucks

- 3.2.3.2 Smart fleet management and telematics integration

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Powertrain technology evolution

- 3.3.1.2 Battery technology for electric pickups

- 3.3.1.3 Autonomous driving integration

- 3.3.1.4 Connectivity & infotainment systems

- 3.3.1.5 Advanced Driver Assistance Systems (ADAS)

- 3.3.2 Emerging technologies

- 3.3.2.1 Lightweight materials & construction

- 3.3.2.2 Manufacturing technology advances

- 3.3.2.3 Charging infrastructure development

- 3.3.2.4 Vehicle-to-Grid (V2G) technology

- 3.3.2.5 Over-the-Air (OTA) update capabilities

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 CAFE fuel economy standards

- 3.5.2 EPA emissions regulations

- 3.5.3 NHTSA safety standards

- 3.5.4 State-Level ZEV mandates

- 3.5.5 Commercial vehicle regulations

- 3.5.6 Future regulatory trends

- 3.6 Price trends analysis

- 3.6.1 Historical price evolution by segment

- 3.6.2 Regional price variations

- 3.6.3 Trim level pricing strategies

- 3.6.4 Electric vs ICE price parity timeline

- 3.6.5 Fleet vs retail pricing dynamics

- 3.6.6 Options & accessories pricing

- 3.7 Production & sales statistics

- 3.7.1 Global production capacity analysis

- 3.7.2 Manufacturing plant utilization

- 3.7.3 Sales volume trends by model

- 3.7.4 Seasonal sales patterns

- 3.7.5 Inventory management analysis

- 3.7.6 Production flexibility assessment

- 3.7.7 Supply chain lead times

- 3.8 Cost breakdown analysis

- 3.8.1 Vehicle development costs

- 3.8.2 Manufacturing cost structure

- 3.8.3 Material cost analysis

- 3.8.4 Labor cost assessment

- 3.8.5 Technology integration costs

- 3.8.6 Regulatory compliance costs

- 3.9 Patent & innovation analysis

- 3.9.1 Powertrain technology patents

- 3.9.2 Electric vehicle patents

- 3.9.3 Autonomous driving patents

- 3.9.4 Lightweight construction patents

- 3.9.5 Manufacturing process patents

- 3.9.6 Patent portfolio analysis by OEM

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Environmental impact assessment & lifecycle analysis

- 3.12.2 Social impact & community relations

- 3.12.3 Governance & corporate responsibility

- 3.12.4 Sustainable technological development

- 3.13 Investment Landscape Analysis

- 3.13.1 OEM capital investment patterns

- 3.13.2 Electric vehicle investment

- 3.13.3 Manufacturing facility investments

- 3.13.4 R&D investment allocation

- 3.13.5 Joint venture & partnership investments

- 3.14 Customer behavior analysis

- 3.14.1 Purchase decision factors

- 3.14.2 Brand loyalty patterns

- 3.14.3 Usage pattern analysis

- 3.14.4 Replacement cycle trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Size, 2021 - 2034 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Compact

- 5.3 Mid-size

- 5.4 Full-size

Chapter 6 Market Estimates & Forecast, By Power Train, 2021 - 2034 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By Towing Capability, 2021 - 2034 ($ Bn & Units)

- 7.1 Key trends

- 7.2 Light towing pickup trucks (Up to 7,500 lbs)

- 7.3 Medium towing pickup trucks (7,501-12,000 lbs)

- 7.4 Heavy towing pickup trucks (12,001+ lbs)

Chapter 8 Market Estimates & Forecast, By Drive, 2021 - 2034 ($ Bn & Units)

- 8.1 Key trends

- 8.2 Rear-wheel drive

- 8.3 All wheel drive

- 8.4 Four-wheel drive

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn & Units)

- 9.1 Key trends

- 9.2 Personal

- 9.3 Commercial

- 9.3.1 Construction and heavy equipment

- 9.3.2 Agriculture and farming

- 9.3.3 Landscaping and outdoor services

- 9.3.4 Utility and municipal use

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn & Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Ford

- 11.1.2 GMC

- 11.1.3 Stellantis (Ram Trucks)

- 11.1.4 Toyota

- 11.1.5 Nissan

- 11.1.6 Honda

- 11.1.7 Rivian Automotive

- 11.1.8 Tesla

- 11.1.9 Isuzu Motors

- 11.1.10 Mahindra & Mahindra

- 11.1.11 Chevrolet

- 11.2 Regional players

- 11.2.1 Great Wall Motors

- 11.2.2 Canoo

- 11.2.3 Alpha Motor

- 11.2.4 Bollinger

- 11.2.5 SAIC Motor

- 11.2.6 Tata Motors

- 11.2.7 Volkswagen Commercial Vehicles

- 11.2.8 Mitsubishi Motors

- 11.2.9 Hyundai Motor Company

- 11.2.10 JAC Motors

- 11.2.11 Foton Motor

- 11.2.12 SsangYong Motor

- 11.2.13 Changan Automobile

- 11.3 Emerging players

- 11.3.1 Lordstown Motors

- 11.3.2 Atlis Motor Vehicles

- 11.3.3 Fisker

- 11.3.4 Hercules Electric Vehicles

- 11.3.5 Nikola

- 11.3.6 Workhorse

- 11.3.7 XOS

美國電動皮卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國電動皮卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 電動皮卡市場:依動力傳動系統、負載容量、車身尺寸及地區分類

電動皮卡市場:依動力傳動系統、負載容量、車身尺寸及地區分類 全球大型皮卡市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球小型皮卡市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球皮卡車附件市場規模、佔有率、趨勢和成長分析報告:2026-2034年皮卡車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

全球大型皮卡市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球小型皮卡市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球皮卡車附件市場規模、佔有率、趨勢和成長分析報告:2026-2034年皮卡車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 皮卡車市場規模、佔有率、趨勢及預測(按燃料類型、車輛類型、應用和地區分類),2026-2034年

皮卡車市場規模、佔有率、趨勢及預測(按燃料類型、車輛類型、應用和地區分類),2026-2034年 皮卡車改裝後蓋市場:按產品類型、材料、價格範圍、表面處理、最終用戶和分銷管道分類的全球預測(2026-2032年)日本皮卡車市場報告(按燃料類型(柴油、汽油、電動及其他)、車輛類型(輕型、重型)、用途(個人用途、商業用途)和地區分類,2026-2034)

皮卡車改裝後蓋市場:按產品類型、材料、價格範圍、表面處理、最終用戶和分銷管道分類的全球預測(2026-2032年)日本皮卡車市場報告(按燃料類型(柴油、汽油、電動及其他)、車輛類型(輕型、重型)、用途(個人用途、商業用途)和地區分類,2026-2034) 皮卡車市場規模、佔有率和成長分析(按車輛類型、燃料類型、應用和地區分類)—產業預測(2026-2033 年)

皮卡車市場規模、佔有率和成長分析(按車輛類型、燃料類型、應用和地區分類)—產業預測(2026-2033 年)