|

市場調查報告書

商品編碼

1844331

氣道清除設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Airway Clearance Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

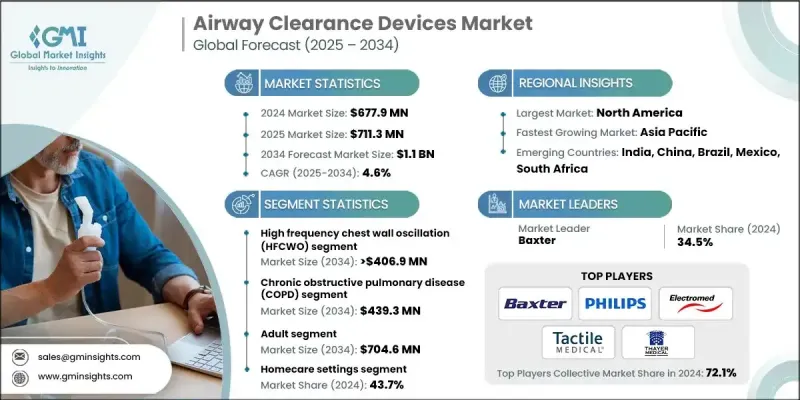

2024 年全球氣道清理設備市場價值為 6.779 億美元,預計將以 4.6% 的複合年成長率成長,到 2034 年達到 11 億美元。

呼吸系統疾病盛行率的上升、科技的進步、人口老化以及人們對氣道治療的認知的提高,都是推動該市場成長的關鍵因素。醫療保健提供者、付款人和生命科學公司擴大採用氣道清除解決方案,以改善治療效果、簡化護理流程並增強合規性。高頻胸壁振盪 (HFCWO) 背心、振盪呼氣正壓 (OPEP) 系統以及互聯數位健康解決方案的引入,正在重塑患者管理慢性肺部疾病的方式。這些創新技術能夠實現個人化治療調整和遠端監控,使護理更加高效,更加以患者為中心。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6.779億美元 |

| 預測值 | 11億美元 |

| 複合年成長率 | 4.6% |

病患教育計畫和認知計畫有助於促進早期診斷和呼吸系統疾病治療的依從性。同時,全球醫療保健支出的不斷成長、支持性報銷框架以及針對慢性肺部疾病管理的公共衛生舉措,正在鼓勵各地區更多地採用呼吸道清除療法。隨著門診和家庭護理模式的推進,預計在預測期內,對緊湊、方便用戶使用且非侵入性的呼吸設備的需求將持續成長。

2024年,撲動黏液清除設備市場規模達到1.52億美元,預計2034年將以5.3%的複合年成長率成長。這類設備因其緊湊的設計、易用性和成本效益而日益普及。它們特別適合呼吸系統疾病較輕的患者,並且通常是自我照護的首選。其價格實惠的特性也使其在資源匱乏的地區和各種醫療保健系統中都能普及。隨著人們的注意力轉向預防和遠端護理,這類設備為在非醫院環境中維持呼吸健康提供了一種便捷的選擇。

慢性阻塞性肺病 (COPD) 市場佔 42%,預計到 2034 年將達到 4.393 億美元。 COPD 仍然是全球最常見的呼吸系統疾病之一,環境和生活方式因素(例如污染、吸煙和職業危害)是其盛行率上升的主要原因。 COPD 患者經常出現黏液積聚和呼吸道阻塞的症狀,因此迫切需要有效的呼吸道清除技術來改善呼吸、減少住院率並增強日常功能。

2024年,北美氣道清除設備市場佔38.7%的市佔率。該地區受益於完善的醫療基礎設施、耐用醫療設備的普及率以及有利的監管框架。在旨在促進獨立護理和改善生活品質的舉措的推動下,振盪式和氣動脈衝設備在住宅環境中的使用日益增多。該地區專注於個人化治療,並將先進技術融入家庭護理,這正在加速氣道清除解決方案的普及。

影響全球氣道清除設備市場的關鍵參與者包括 ICU Medical、Monaghan Medical Corporation、VYAIRE MEDICAL、Baxter、Dymedso、ABM Respiratory Care、Mercury Medical、Pari Medical、Thayer Medical、Sentec、Dima Italia、Electromed、Tactile Medical、Philips、Phayer Medical、Sentec、Dima Italia、Electromed、Tactile Medical、PhilipRTs、Pne Medical Health Health 和 VORTliRT 和 VORT Technology。氣道清除設備市場的領先公司正在追求產品創新、數位整合和策略合作,以加強其市場地位。透過整合智慧連接、遠端監控和個人化治療功能,他們讓設備更加直覺,更能滿足患者的需求。企業還在全球擴展其分銷網路,並進入新的地理市場,以挖掘未滿足的需求。一些參與者正在投資臨床研究,以驗證設備的有效性並滿足不斷發展的監管標準。與呼吸照護提供者、醫院和遠距醫療平台的合併和合作使得住院和家庭護理環境中的採用率更高。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 呼吸系統疾病發生率上升

- 提高患者意識和產品發布

- 非侵入性治療方案的採用率不斷提高

- 政府大力推行控制呼吸道疾病的舉措

- 產業陷阱與挑戰

- 設備成本高且監管要求嚴格

- 市場機會

- 數位健康與遠端監控的整合

- 產品創新與客製化

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 攜帶式和家用氣道清除設備的成長

- 支援遠端監控的數位健康平台

- 患者友善的振盪 PEP 和 HFCWO 系統

- 新興技術

- 人工智慧呼吸監測和預測分析

- 穿戴式連接氣道清除設備

- 具有自適應治療模式的智慧型設備

- 當前的技術趨勢

- 差距分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 人工智慧、數位健康和連網設備的融合

- 擴展慢性呼吸道照護的居家照護解決方案

- 基礎建設改善的新興市場實現成長

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 夥伴關係與合作

- 推出新服務類型

- 擴張計劃

第5章:市場估計與預測:按設備類型,2021 - 2034 年

- 主要趨勢

- 高頻胸壁振盪(HFCWO)

- 撲動式黏液清除裝置

- 肺內衝擊通氣(IPV)

- 機械性咳嗽輔助裝置

- 呼氣正壓(PEP)

- 其他設備類型

第6章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 慢性阻塞性肺病(COPD)

- 支氣管擴張

- 囊腫纖維化

- 神經肌肉

- 其他應用

第7章:市場估計與預測:按年齡層,2021 - 2034 年

- 主要趨勢

- 成人

- 兒科

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 居家照護環境

- 醫院

- 門診手術中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ABM Respiratory Care

- Baxter

- Dima Italia

- Dymedso

- Electromed

- ICU Medical

- Philips

- Mercury Medical

- Monaghan Medical Corporation

- Pari Medical

- Pneumo Care Health

- Sentec

- Tactile Medical

- Thayer Medical

- VORTRAN Medical Technology

- VYAIRE MEDICAL

The Global Airway Clearance Devices Market was valued at USD 677.9 million in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 1.1 billion by 2034.

The rising prevalence of respiratory illnesses, advancements in technology, an aging population, and greater awareness of airway therapy are all key contributors to this market's growth. Healthcare providers, payers, and life sciences companies are increasingly adopting airway clearance solutions to improve outcomes, streamline care delivery, and enhance regulatory compliance. The introduction of high-frequency chest wall oscillation (HFCWO) vests, oscillatory positive expiratory pressure (OPEP) systems, and connected digital health solutions is reshaping how patients manage chronic pulmonary conditions. These innovations enable personalized therapy adjustments and remote monitoring, making care more efficient and patient-centric.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $677.9 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 4.6% |

Patient education initiatives and awareness programs are helping boost early diagnosis and adherence to respiratory treatments. At the same time, rising global healthcare expenditure, supportive reimbursement frameworks, and public health initiatives for managing chronic lung diseases are encouraging higher adoption of airway clearance therapies across regions. With the push toward outpatient and home care models, the demand for compact, user-friendly, and non-invasive respiratory devices is expected to rise consistently over the forecast period.

In 2024, the flutter mucus clearance device segment reached USD 152 million and is forecast to grow at a CAGR of 5.3% through 2034. These devices are becoming increasingly popular due to their compact design, ease of use, and cost-efficiency. They are particularly well-suited for individuals with less severe respiratory issues and are often preferred for self-administered care. Their affordability also makes them accessible in low-resource settings and across a wide range of healthcare systems. As the focus shifts toward prevention and remote care, these devices offer a convenient option for maintaining respiratory health in non-hospital environments.

The chronic obstructive pulmonary disease (COPD) segment held a 42% share and is expected to reach USD 439.3 million by 2034. COPD remains one of the most widespread respiratory conditions globally, with environmental and lifestyle factors such as pollution, smoking, and occupational hazards driving its prevalence. Patients with COPD frequently suffer from mucus build-up and obstructed airways, creating a strong need for effective airway clearance to improve breathing, reduce hospitalizations, and enhance daily function.

North America Airway Clearance Devices Market held a 38.7% share in 2024. The region benefits from well-established healthcare infrastructure, high adoption of durable medical equipment, and favorable regulatory frameworks. There's growing use of oscillatory and air-pulse devices in residential settings, driven by initiatives aimed at promoting independent care and improving quality of life. The region's focus on personalized treatment and integration of advanced technologies into home care is accelerating the uptake of airway clearance solutions.

Key players shaping the Global Airway Clearance Devices Market include ICU Medical, Monaghan Medical Corporation, VYAIRE MEDICAL, Baxter, Dymedso, ABM Respiratory Care, Mercury Medical, Pari Medical, Thayer Medical, Sentec, Dima Italia, Electromed, Tactile Medical, Philips, Pneumo Care Health, and VORTRAN Medical Technology. Leading companies in the airway clearance devices market are pursuing product innovation, digital integration, and strategic collaborations to reinforce their market presence. By incorporating smart connectivity, remote monitoring, and personalized therapy features, they're making devices more intuitive and responsive to patient needs. Firms are also expanding their distribution networks globally and entering new geographic markets to tap into unmet demand. Several players are investing in clinical research to validate device efficacy and meet evolving regulatory standards. Mergers and partnerships with respiratory care providers, hospitals, and telehealth platforms allow for greater adoption in both inpatient and home care environments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Device type trends

- 2.2.3 Application trends

- 2.2.4 Age group trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in incidence of respiratory conditions

- 3.2.1.2 Growing patient awareness and product launches

- 3.2.1.3 Increasing adoption of non-invasive treatment options

- 3.2.1.4 Surge in government initiatives towards controlling respiratory disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device cost and stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of digital health and remote monitoring

- 3.2.3.2 Product innovation and customization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Growth of portable and home-based airway clearance devices

- 3.5.1.2 Digital health platforms enabling remote monitoring

- 3.5.1.3 Patient-friendly oscillatory PEP and HFCWO systems

- 3.5.2 Emerging technologies

- 3.5.2.1 AI-powered respiratory monitoring and predictive analytics

- 3.5.2.2 Wearable connected airway clearance devices

- 3.5.2.3 Smart devices with adaptive therapy modes

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Convergence of AI, digital health, and connected devices

- 3.9.2 Expansion of homecare solutions for chronic respiratory care

- 3.9.3 Growth in emerging markets with improved infrastructure

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 High frequency chest wall oscillation (HFCWO)

- 5.3 Flutter mucus clearance device

- 5.4 Intrapulmonary percussive ventilation (IPV)

- 5.5 Mechanical cough assist devices

- 5.6 Positive expiratory pressure (PEP)

- 5.7 Other device types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chronic obstructive pulmonary disease (COPD)

- 6.3 Bronchiectasis

- 6.4 Cystic fibrosis

- 6.5 Neuromuscular

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Homecare settings

- 8.3 Hospital

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABM Respiratory Care

- 10.2 Baxter

- 10.3 Dima Italia

- 10.4 Dymedso

- 10.5 Electromed

- 10.6 ICU Medical

- 10.7 Philips

- 10.8 Mercury Medical

- 10.9 Monaghan Medical Corporation

- 10.10 Pari Medical

- 10.11 Pneumo Care Health

- 10.12 Sentec

- 10.13 Tactile Medical

- 10.14 Thayer Medical

- 10.15 VORTRAN Medical Technology

- 10.16 VYAIRE MEDICAL

呼吸道清潔系統市場:按設備類型、適應症、最終用戶和分銷管道分類的全球市場預測,2026-2032 年呼吸道管理設備市場:2026-2032年全球市場預測(依產品類型、材料、插入方式、最終用戶、應用和尺寸分類)

呼吸道清潔系統市場:按設備類型、適應症、最終用戶和分銷管道分類的全球市場預測,2026-2032 年呼吸道管理設備市場:2026-2032年全球市場預測(依產品類型、材料、插入方式、最終用戶、應用和尺寸分類) 呼吸道管理設備市場報告:按產品類型、患者類型、應用、最終用途和地區分類(2026-2034 年)喉罩市場:2026-2032年全球市場預測(按產品類型、材料、尺寸、應用、最終用戶和分銷管道分類)

呼吸道管理設備市場報告:按產品類型、患者類型、應用、最終用途和地區分類(2026-2034 年)喉罩市場:2026-2032年全球市場預測(按產品類型、材料、尺寸、應用、最終用戶和分銷管道分類) 呼吸道管理設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測困難呼吸道管理模擬器市場:按模擬器類型、保真度、應用類型、最終用戶和部署模式分類,全球預測,2026-2032年

呼吸道管理設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測困難呼吸道管理模擬器市場:按模擬器類型、保真度、應用類型、最終用戶和部署模式分類,全球預測,2026-2032年 2026年全球喉罩市場報告2026年囊腫纖維化氣道清除裝置全球市場報告全球喉罩市場規模、佔有率、趨勢和成長分析報告(2026-2034)

2026年全球喉罩市場報告2026年囊腫纖維化氣道清除裝置全球市場報告全球喉罩市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2025-2029年全球喉罩氣道市場

2025-2029年全球喉罩氣道市場