|

市場調查報告書

商品編碼

1844300

越野車煞車系統市場機會、成長動力、產業趨勢分析及2025-2034年預測Off-road Vehicle Braking System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

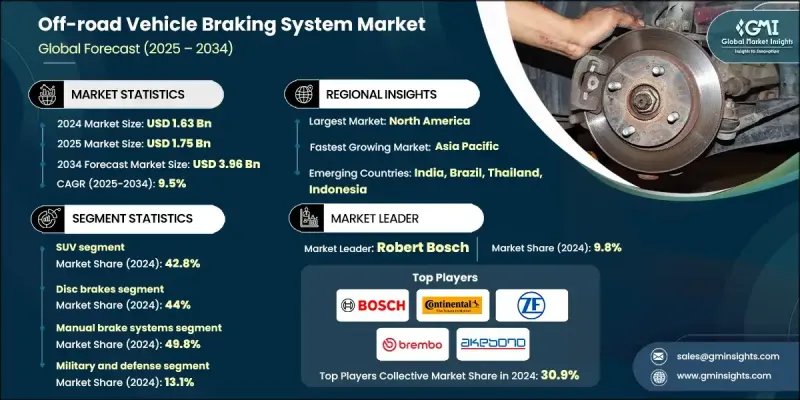

2024 年全球越野車煞車系統市場價值為 16.3 億美元,預計到 2034 年將以 9.5% 的複合年成長率成長至 39.6 億美元。

由於越野車會遇到各種地形,包括陡坡、鬆散的岩石、沙地和泥地,因此對越野車高性能煞車系統的需求持續成長。與傳統煞車系統不同,越野煞車機制必須對不同的路面狀況做出自適應反應,同時保持牽引力和控制。駕駛員依靠煞車系統進行精確調節,尤其是在崎嶇地形或承載重物時。由於越野車經常搭載額外的設備或乘客,其煞車系統必須處理重量分佈變化,同時有效散熱和調節油液溫度。這些系統還必須防止煞車衰退,確保在極端條件和長時間運行下的可靠性。煞車技術的進步繼續致力於提高穩定性、控制力和響應能力,使車輛即使在滿載或在惡劣、不可預測的環境中行駛時也能保持最佳制動力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16.3億美元 |

| 預測值 | 39.6億美元 |

| 複合年成長率 | 9.5% |

SUV細分市場在2024年佔據42.8%的市場佔有率,預計到2034年將以10.3%的複合年成長率成長。如今,SUV擴大配備了能夠適應路面變化的煞車系統,從而增強了在崎嶇地形上的牽引力和車輛控制。這些技術通常與電子穩定和牽引力控制系統配合使用,以在各種駕駛條件下支援安全性和越野操控性。

2024年,碟式煞車市場佔44%的市場佔有率,預計2025年至2034年的複合年成長率將達到9.9%。碟式煞車,尤其是碳-碳複合材料製成的碟式煞車,因其能夠承受極端溫度並減輕車輛總重量而日益受到歡迎。其卓越的強度重量比和耐熱性使其成為性能和耐用性至關重要的越野應用的理想選擇。

2025年至2034年間,美國越野車煞車系統市場將以10.1%的複合年成長率成長。廣泛的越野車道、專用公園、經銷商和服務基礎設施網路正在推動國內需求。電動越野車的興起也提升了市場潛力。製造商正在推出電動越野車,這些車型在不影響車輛堅固耐用性能的情況下,能夠提供更大的扭力、更安靜的性能和更低的排放。美國消費者越來越青睞配備GPS、遠端資訊處理、車載電腦和電子輔助轉向等先進功能的越野車,這進一步提升了對精密煞車系統的需求。

主導越野車煞車系統市場的關鍵參與者包括採埃孚、克諾爾、萬都、愛德克斯、羅伯特·博世、大陸、布雷博、曙光煞車工業和日信工業。為了鞏固其地位,越野車煞車系統領域的公司正專注於創新和策略合作。許多公司正在投資輕質、高性能煞車材料,以提高耐熱性和耐用性,特別是對於電動和混合動力越野平台。製造商也將電子煞車解決方案與先進的駕駛輔助技術相結合,以增強安全性和控制力。擴大與原始設備製造商的合作夥伴關係並根據特定地形需求客製化煞車系統,有助於公司提供更專業、更有價值的解決方案。同時,擴大製造能力和利用車輛遠端資訊處理資料有助於製造商提供預測性維護和性能最佳化,從而確保長期客戶忠誠度。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預報

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 電氣化和再生煞車

- 安全法規和標準

- 惡劣的環境暴露

- 車輛載重和重量

- 地形多變

- 產業陷阱與挑戰

- 開發和維護成本高

- 對新興市場的認知有限

- 市場機會

- 電動越野車的成長

- 高級安全整合

- 農業和國防部門的需求

- 智慧型互聯煞車系統

- 成長動力

- 成長潛力分析

- 監管格局

- 波特的分析

- PESTEL分析

- 技術與創新格局

- 當前的技術趨勢

- 新興技術

- 成本分解分析

- 專利分析

- 價格趨勢

- 按地區

- 搭車

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本結構與經濟分析

- 製造成本明細(材料、人工、間接費用)

- 研發投資需求及攤銷

- 規模經濟分析

- 總擁有成本 (TCO) 模型

- 需求價格彈性分析

- 進出口貿易分析

- 全球貿易流程圖(HS編碼分析)

- 主要進出口國家

- 各地區貿易平衡分析

- 關稅結構和貿易壁壘的影響

- 供應鏈脆弱性評估

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重要新聞和舉措

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- SUV

- UTV

- 沙灘車

- 雪地摩托車

- 越野摩托車

第6章:市場估計與預測:按制動,2021 - 2034 年

- 主要趨勢

- 碟式煞車

- 鼓式煞車

- 液壓煞車

- 氣動煞車

- 機電煞車

第7章:市場估計與預測:按煞車系統營運,2021 - 2034 年

- 主要趨勢

- 手動煞車系統

- 自動煞車系統

- 防鎖死煞車系統(ABS)

- 電子穩定控制系統(ESC)

- 牽引力控制系統(TCS)

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 休閒娛樂

- 商業的

- 農業

- 軍事和國防

- 採礦和開採

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 荷蘭

- 俄羅斯

- 亞太地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 新加坡

- 韓國

- 泰國

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球頂尖玩家

- 布雷博

- 採埃孚

- 大陸航空

- 羅伯特·博世

- 曙光煞車工業

- 愛信

- 天納克

- 萬都

- 日清工業

- 區域參與者

- 毛蟲

- 小松

- 克諾爾煞車系統公司

- 瀚德

- 日立阿斯泰莫

- 技術專家

- 愛德克斯

- 海耶斯績效系統

- 威爾伍德工程公司

- 新興企業和顛覆者

- 雅馬哈

- Rivian 汽車

- OEM整合合作夥伴

- 約翰迪爾

- 沃爾沃建築設備

- 利勃海爾

- 凱斯紐荷蘭工業集團

The Global Off-road Vehicle Braking System Market was valued at USD 1.63 billion in 2024 and is estimated to grow at a CAGR of 9.5% to reach USD 3.96 billion by 2034.

The demand for high-performance braking systems in off-road vehicles continues to grow due to the diverse terrains these vehicles encounter, including steep inclines, loose rocks, sand, and mud. Unlike conventional braking systems, off-road braking mechanisms must deliver adaptive responsiveness to varying surface conditions while maintaining traction and control. Drivers depend on braking systems to offer precise modulation, particularly when navigating rugged terrain or managing heavy payloads. As off-road vehicles frequently carry added equipment or passengers, their braking systems must handle weight distribution shifts while effectively dissipating heat and regulating fluid temperature. These systems must also resist brake fade, ensuring reliability under extreme conditions and during prolonged operation. Advancements in braking technology continue to focus on improving stability, control, and responsiveness, making it possible to maintain optimal stopping power even when vehicles are fully loaded or maneuvering through harsh, unpredictable environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.63 Billion |

| Forecast Value | $3.96 Billion |

| CAGR | 9.5% |

The SUV segment held 42.8% in 2024 and is forecasted to grow at a CAGR of 10.3% through 2034. SUVs today are increasingly equipped with braking systems that adapt to changing surfaces, enhancing traction and vehicle control across uneven terrains. These technologies are often paired with electronic stability and traction control systems to support safety and off-road maneuverability in a wide range of driving conditions.

In 2024, the disc brake segment held a 44% share and will grow at a CAGR of 9.9% from 2025 to 2034. Disc brakes, particularly those constructed from carbon-carbon composites, are gaining popularity due to their ability to withstand extreme temperatures while reducing overall vehicle weight. Their superior strength-to-weight ratio and heat resistance make them ideal for off-road applications where both performance and durability are critical.

U.S. Off-road Vehicle Braking System Market will grow at a CAGR of 10.1% between 2025 and 2034. An extensive network of off-road trails, dedicated parks, dealerships, and service infrastructure is driving domestic demand. The rise of electric off-road vehicles is also boosting market potential. Manufacturers are rolling out electric variants that deliver greater torque, quieter performance, and lower emissions all without compromising the vehicle's rugged capabilities. U.S. consumers are increasingly favoring off-road vehicles equipped with advanced features like GPS, telematics, onboard computers, and electronic power steering, further elevating the demand for precision-engineered braking systems.

Key players dominating the Off-road Vehicle Braking System Market include ZF Friedrichshafen, Knorr-Bremse, Mando, Advics, Robert Bosch, Continental, Brembo, Akebono Brake Industry, and Nissin Kogyo. To strengthen their position, companies in the off-road vehicle braking system sector are focusing on innovation and strategic collaboration. Many are investing in lightweight, high-performance brake materials that enhance thermal resistance and durability, particularly for electric and hybrid off-road platforms. Manufacturers are also integrating electronic braking solutions with advanced driver-assist technologies to enhance safety and control. Expanding partnerships with OEMs and customizing braking systems for terrain-specific needs are helping companies offer more specialized, value-driven solutions. In parallel, expanding manufacturing capabilities and leveraging data from vehicle telematics are helping manufacturers provide predictive maintenance and performance optimization, securing long-term customer loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Brake

- 2.2.4 Brake system operations

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification & regenerative braking

- 3.2.1.2 Safety regulations & standards

- 3.2.1.3 Harsh environmental exposure

- 3.2.1.4 Vehicle load & weight

- 3.2.1.5 Terrain variability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development & maintenance costs

- 3.2.2.2 Limited awareness in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric off-road vehicles

- 3.2.3.2 Advanced safety integration

- 3.2.3.3 Demand in agriculture & defense sectors

- 3.2.3.4 Smart & connected braking systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology & innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By Vehicle

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost Structure & Economics Analysis

- 3.12.1 Manufacturing Cost Breakdown (Materials, Labor, Overhead)

- 3.12.2 R&D Investment Requirements & Amortization

- 3.12.3 Economies of Scale Analysis

- 3.12.4 Total Cost of Ownership (TCO) Models

- 3.12.5 Price Elasticity of Demand Analysis

- 3.13 Import-Export Trade Analysis

- 3.13.1 Global Trade Flow Mapping (HS Code Analysis)

- 3.13.2 Top Importing & Exporting Countries

- 3.13.3 Trade Balance Analysis by Region

- 3.13.4 Tariff Structure & Trade Barriers Impact

- 3.13.5 Supply Chain Vulnerability Assessment

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.1.1 SUV

- 5.1.2 UTV

- 5.1.3 ATV

- 5.1.4 Snowmobile

- 5.1.5 Off-road Motorcycle

Chapter 6 Market Estimates & Forecast, By Brake, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Disc Brakes

- 6.3 Drum Brakes

- 6.4 Hydraulic Brakes

- 6.5 Pneumatic Brakes

- 6.6 Electromechanical Brakes

Chapter 7 Market Estimates & Forecast, By Brake System Operations, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.1.1 Manual Brake Systems

- 7.1.2 Automatic Brake Systems

- 7.1.3 Anti-lock Braking Systems (ABS)

- 7.1.4 Electronic Stability Control (ESC)

- 7.1.5 Traction Control Systems (TCS)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Recreational

- 8.3 Commercial

- 8.4 Agricultural

- 8.5 Military and Defense

- 8.6 Mining and Extraction

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 Australia

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Indonesia

- 9.4.5 Japan

- 9.4.6 Singapore

- 9.4.7 South Korea

- 9.4.8 Thailand

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1.1.1 Top Global Players

- 10.1.1.1.1 Brembo

- 10.1.1.1.2 ZF Friedrichshafen

- 10.1.1.1.3 Continental

- 10.1.1.1.4 Robert Bosch

- 10.1.1.1.5 Akebono Brake Industry

- 10.1.1.1.6 AISIN

- 10.1.1.1.7 Tenneco

- 10.1.1.1.8 Mando

- 10.1.1.1.9 Nissin Kogyo

- 10.1.1.2 Regional Players

- 10.1.1.2.1 Caterpillar

- 10.1.1.2.2 Komatsu

- 10.1.1.2.3 KNORR-BREMSE

- 10.1.1.2.4 Haldex

- 10.1.1.2.5 Hitachi Astemo

- 10.1.1.2.6 Technology Specialists

- 10.1.1.2.7 ADVICS

- 10.1.1.2.8 Hayes Performance Systems

- 10.1.1.2.9 Wilwood Engineering

- 10.1.1.3 Emerging Players & Disruptors

- 10.1.1.3.1 Yamaha

- 10.1.1.3.2 Rivian Automotive

- 10.1.1.3.3 OEM Integration Partners

- 10.1.1.3.4 John Deere

- 10.1.1.3.5 Volvo Construction Equipment

- 10.1.1.3.6 Liebherr

- 10.1.1.3.7 CNH Industrial

風力發電機輔助爬升系統市場:依系統類型、安裝方式、渦輪機容量、渦輪機高度、通路、應用、最終用戶分類,全球預測,2026-2032年全球動力爬坡輔助系統市場依技術、動力源、產品類型、通路、應用及最終用戶分類,2026-2032年預測

風力發電機輔助爬升系統市場:依系統類型、安裝方式、渦輪機容量、渦輪機高度、通路、應用、最終用戶分類,全球預測,2026-2032年全球動力爬坡輔助系統市場依技術、動力源、產品類型、通路、應用及最終用戶分類,2026-2032年預測 2026-2034年全球汽車煞車系統市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車煞車系統市場規模、佔有率、趨勢和成長分析報告 商用車煞車系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、銷售管道、產品類型、地區和競爭格局分類,2021-2031年)自動緊急煞車系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、技術類型、感測器類型、地區和競爭格局分類,2021-2031年)重型煞車改裝套件市場:按煞車卡鉗類型、轉子設計、材質、車輛類型、應用和最終用戶分類 - 全球預測 2026-2032 年電機制動器市場:按操作方式、類型、材料、分銷管道和最終用戶分類,全球預測(2026-2032)乘用車煞車系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、銷售管道、產品類型、地區和競爭格局分類(2021-2031 年預測)

商用車煞車系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、銷售管道、產品類型、地區和競爭格局分類,2021-2031年)自動緊急煞車系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、技術類型、感測器類型、地區和競爭格局分類,2021-2031年)重型煞車改裝套件市場:按煞車卡鉗類型、轉子設計、材質、車輛類型、應用和最終用戶分類 - 全球預測 2026-2032 年電機制動器市場:按操作方式、類型、材料、分銷管道和最終用戶分類,全球預測(2026-2032)乘用車煞車系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、銷售管道、產品類型、地區和競爭格局分類(2021-2031 年預測) 煞車系統市場規模、佔有率和成長分析(按產品類型、最終用途、分銷管道和地區分類)-2026-2033年產業預測

煞車系統市場規模、佔有率和成長分析(按產品類型、最終用途、分銷管道和地區分類)-2026-2033年產業預測 2025年全球越野車煞車系統市場報告

2025年全球越野車煞車系統市場報告