|

市場調查報告書

商品編碼

1844269

飛機彈射座椅市場機會、成長動力、產業趨勢分析及2025-2034年預測Aircraft Ejection Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

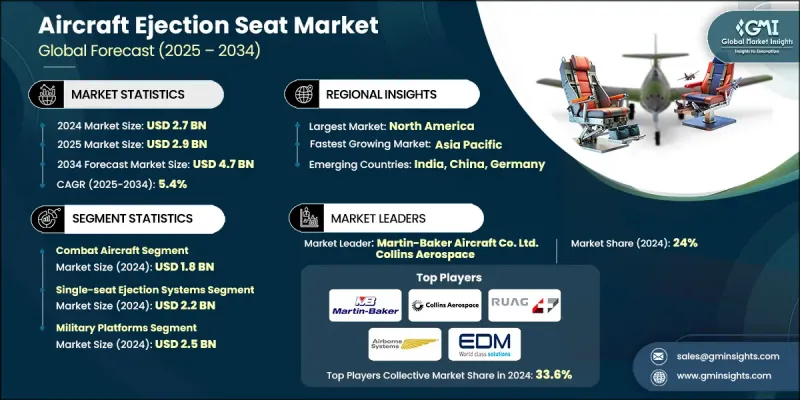

2024 年全球飛機彈射座椅市場價值為 27 億美元,預計到 2034 年將以 5.4% 的複合年成長率成長至 47 億美元。

這一成長主要源於戰鬥機採購量的增加、國防飛機隊的持續升級以及飛行員生存技術的進步。隨著全球國防製造商逐步提升自給自足能力,彈射座椅系統成為空戰安全創新的焦點。國防機構將增強飛行員安全性和高風險情況下的關鍵任務生存能力放在首位,對技術先進且智慧化的彈射解決方案的需求日益成長。快速的現代化升級計劃和針對老舊機身的延壽計劃進一步擴大了對可改裝的下一代彈射座椅的需求。國防參與者也正在整合更智慧的系統和即時感測器輸入,以最佳化彈射時機並降低高速彈射過程中的受傷風險。這種創新與策略的融合將持續塑造全球彈射座椅的發展軌跡。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 27億美元 |

| 預測值 | 47億美元 |

| 複合年成長率 | 5.4% |

2024年,戰鬥機市場收入達到18億美元,這得益於國防預算的增加、現代化升級的推進、日益加劇的地緣政治不確定性以及全球對升級飛行員保護解決方案的追求。人們對整合更輕、模組化、更可靠的彈射座椅系統的興趣日益濃厚,這些系統能夠與智慧航空電子設備和救生技術介接。這些系統正成為注重快速部署和機隊壽命的軍事航空計畫不可或缺的一部分。

2024年,單座彈射系統市場產值達22億美元。單座彈射系統的需求與先進前線戰機的採購以及全球戰鬥機隊持續現代化的步伐密切相關。對更緊湊、更輕、更耐用且整合健康監測功能的彈射系統的需求日益成長。這與更廣泛的努力一致,即提供可擴展的彈射解決方案,使其能夠無縫嵌入未來戰鬥機平台,從而最佳化任務準備和生存能力。

2024年,美國飛機彈射座椅市場規模達到11億美元,這得益於強勁的國防撥款、空軍戰略升級以及對先進彈射能力不斷成長的投資。美國國內製造商正優先考慮設計創新,以增強飛機相容性、減輕材料重量、開發人工智慧驅動的決策系統以及改善彈射後支援基礎設施。美國不斷擴大的機隊現代化計劃以及對機組人員保護的重視,仍然是市場持續成長的關鍵因素。

飛機彈射座椅市場的領先公司包括印度斯坦航空有限公司、柯林斯航太、AmSafe Bridport 有限公司、洛克希德馬丁、諾斯羅普格魯曼、馬丁貝克飛機有限公司、Airborne Systems Inc.、QinetiQ Group Plc、Parachute Laboratories Inc.、Quickstep Technologies、Tencate Advanced Armor、RUEscal. Equipment Services Ltd.、Vector 航太、Cobham Plc 和 NPP Zvezda。為了加強其影響力,各公司正專注於更輕、模組化的彈射座椅設計、改進的基於感測器的計時系統和整合智慧安全技術。許多參與者正在擴大其改裝產品,以支援老化的飛機平台,同時確保符合下一代國防標準。與空軍和 OEM 的策略合作、持續的研發投資以及強大的售後服務能力使這些公司獲得了競爭優勢。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 增加戰鬥機採購

- 彈射系統的技術改進

- 增強飛行員的生存能力需要先進的彈射系統

- 新興戰鬥機升級和壽命延長計劃

- 國防越來越自力更生

- 製造業的陷阱與挑戰

- 開發和維護成本高

- 與各種飛機的複雜整合

- 成長動力

3.2.3. 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按飛機類型,2021 - 2034 年

- 主要趨勢

- 戰鬥機

- 訓練飛機

- 其他

第6章:市場估計與預測:依座位類型,2021 - 2034

- 主要趨勢

- 單座彈射系統

- 雙座彈射系統

第7章:市場估計與預測:按適用性,2021 - 2034

- 主要趨勢

- 線擬合

- 改造

第8章:市場估計與預測:按組件,2021 - 2034

- 火箭引擎/彈射系統

- 降落傘

- 頂篷拋棄系統

- 其他

第9章:市場估計與預測:依最終用途應用,2021 - 2034

- 軍事平台

- 研究機構

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球關鍵參與者

- Martin-Baker Aircraft Co. Ltd.

- Collins Aerospace

- BAE Systems

- Lockheed Martin

- Northrop Grumman

- 區域關鍵參與者

- 北美洲

- EDM Limited

- AmSafe Bridport Ltd.

- Quickstep Technologies

- 亞太地區

- Hindustan Aeronautics Limited

- NPP Zvezda

- Airborne Systems Inc.

- 歐洲

- RUAG Group

- Safran SA

- Cobham Plc

- QinetiQ Group Plc

- Tencate Advanced Armor

- Vector Aerospace

- Survival Equipment Services Ltd.

- 北美洲

- 利基市場參與者/分銷商

- Butler Parachute Systems Inc.

- Parachute Laboratories Inc.

The Global Aircraft Ejection Seat Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.7 billion by 2034.

The growth is driven by rising fighter jet procurement, ongoing upgrades of defense aircraft fleets, and advancements in pilot survival technologies. As global defense manufacturers move toward greater self-sufficiency, ejection seat systems have become a focal point in air combat safety innovation. With defense agencies prioritizing enhanced safety for pilots and mission-critical survivability in high-risk scenarios, the demand for technologically advanced and intelligent ejection solutions is gaining momentum. Rapid modernization initiatives and life-extension programs for aging airframes are further amplifying demand for retrofit-compatible, next-generation ejection seats. Defense players are also incorporating smarter systems with real-time sensor inputs to optimize timing and reduce injury risk during high-speed ejections. This convergence of innovation and strategy continues to shape the trajectory of ejection seat development worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 5.4% |

The combat aircraft segment generated USD 1.8 billion in 2024, fueled by expanded defense budgets, modernization efforts, rising geopolitical uncertainty, and the global push for upgraded pilot protection solutions. There's rising interest in integrating lighter, modular, and more reliable ejection seat systems capable of interfacing with smart avionics and life-saving technologies. These systems are becoming integral to military aviation programs focused on rapid deployability and fleet longevity.

The single-seat segment generated USD 2.2 billion in 2024. Demand for single-seat systems is closely tied to the procurement of advanced frontline jets and sustained efforts to modernize global fighter fleets. The push for more compact, lightweight systems with enhanced durability and integrated health monitoring features is growing. This aligns with broader efforts to deliver scalable ejection solutions that can be seamlessly embedded into future fighter platforms, optimizing mission readiness and survivability.

U.S. Aircraft Ejection Seat Market reached USD 1.1 billion in 2024, supported by robust defense allocations, strategic air force upgrades, and growing investments in advanced ejection capabilities. Domestic manufacturers are prioritizing design innovations that enhance aircraft compatibility, material lightness, AI-driven decision systems, and improved post-ejection support infrastructure. The country's expanding fleet modernization initiatives and emphasis on aircrew protection remain key contributors to sustained market momentum.

Leading companies involved in Aircraft Ejection Seat Market include Hindustan Aeronautics Limited, Collins Aerospace, AmSafe Bridport Ltd., Lockheed Martin, Northrop Grumman, Martin-Baker Aircraft Co. Ltd., Airborne Systems Inc., QinetiQ Group Plc, Parachute Laboratories Inc., Quickstep Technologies, Tencate Advanced Armor, RUAG Group, Safran SA, EDM Limited, BAE Systems, Butler Parachute Systems Inc., Survival Equipment Services Ltd., Vector Aerospace, Cobham Plc, and NPP Zvezda. To strengthen their presence, companies are focusing on lighter, modular ejection seat designs, improved sensor-based timing systems, and integrated smart safety technologies. Many players are expanding their retrofit offerings to support aging aircraft platforms while ensuring compliance with next-generation defense standards. Strategic collaborations with air forces and OEMs, continuous R&D investments, and strong aftermarket service capabilities are enabling these firms to gain a competitive edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Aircraft type trends

- 2.2.2 Seat type trends

- 2.2.3 Fit trends

- 2.2.4 Component trends

- 2.2.5 End use trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Fighter Aircraft Acquisition

- 3.2.1.2 Technological Improvements in Ejection Systems

- 3.2.1.3 Enhanced pilot survivability demands advanced ejection systems

- 3.2.1.4 Emerging Fighters Upgrade and Life Extension Programs

- 3.2.1.5 Increasingly Self-Reliant in Their Defense

- 3.2.2 Manufacturing Industry pitfalls and challenges

- 3.2.2.1 High cost to develop and maintain

- 3.2.2.2 Complex integration with various aircraft

- 3.2.1 Growth drivers

3.2.3. Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Defense budget analysis

- 3.13 Global defense spending trends

- 3.14 Regional defense budget allocation

- 3.14.1 North America

- 3.14.2 Europe

- 3.14.3 Asia Pacific

- 3.14.4 Middle East and Africa

- 3.14.5 Latin America

- 3.15 Key defense modernization programs

- 3.16 Budget forecast (2025-2034)

- 3.16.1 Impact on Industry Growth

- 3.16.2 Defense Budgets by Country

- 3.17 Supply chain resilience

- 3.18 Geopolitical analysis

- 3.19 Workforce analysis

- 3.20 Digital transformation

- 3.21 Mergers, acquisitions, and strategic partnerships landscape

- 3.22 Risk assessment and management

- 3.23 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Combat Aircraft

- 5.3 Training Aircraft

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Seat Type, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single-seat ejection systems

- 6.3 Twin-seat ejection systems

Chapter 7 Market Estimates and Forecast, By Fit, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Line-fit

- 7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Million & Units)

- 8.1 Rocket motors / catapult systems

- 8.2 Parachutes

- 8.3 Canopy jettison systems

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Units)

- 9.1 Military platforms

- 9.2 Research institutes

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Martin-Baker Aircraft Co. Ltd.

- 11.1.2 Collins Aerospace

- 11.1.3 BAE Systems

- 11.1.4 Lockheed Martin

- 11.1.5 Northrop Grumman

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 EDM Limited

- 11.2.1.2 AmSafe Bridport Ltd.

- 11.2.1.3 Quickstep Technologies

- 11.2.2 Asia Pacific

- 11.2.2.1 Hindustan Aeronautics Limited

- 11.2.2.2 NPP Zvezda

- 11.2.2.3 Airborne Systems Inc.

- 11.2.3 Europe

- 11.2.3.1 RUAG Group

- 11.2.3.2 Safran SA

- 11.2.3.3 Cobham Plc

- 11.2.3.4 QinetiQ Group Plc

- 11.2.3.5 Tencate Advanced Armor

- 11.2.3.6 Vector Aerospace

- 11.2.3.7 Survival Equipment Services Ltd.

- 11.2.1 North America

- 11.3 Niche Players/Distributors

- 11.3.1 Butler Parachute Systems Inc.

- 11.3.2 Parachute Laboratories Inc.