|

市場調查報告書

商品編碼

1833690

馬達起動器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

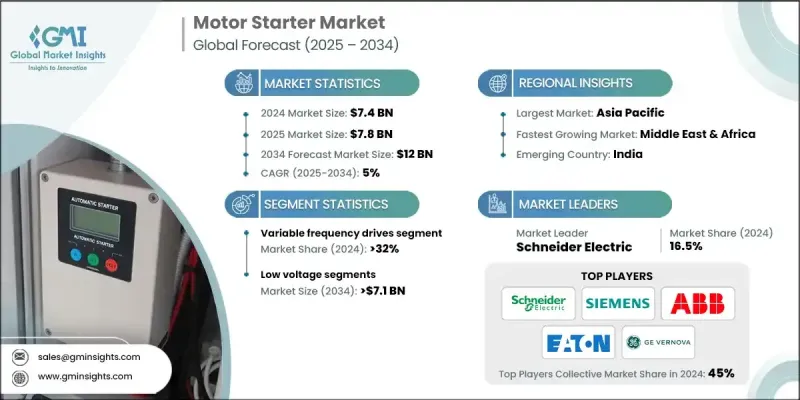

根據 Global Market Insights Inc. 發布的最新報告,全球電動馬達起動器市場規模預計在 2024 年為 74 億美元,預計將從 2025 年的 78 億美元成長到 2034 年的 120 億美元,複合年成長率為 5%。

由於高度重視節能和降低營運成本,各行各業都在投資先進的馬達啟動器,尤其是軟啟動器和智慧啟動器,以幫助減少電湧、管理負載並提高馬達效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 74億美元 |

| 預測值 | 120億美元 |

| 複合年成長率 | 5% |

變頻驅動器獲得牽引力

變頻驅動器 (VFD) 憑藉其卓越的能源效率、精確的電機控制以及對設備機械應力的降低,在 2024 年佔據了相當大的佔有率。 VFD 不僅可以調節馬達轉速,還可以延長馬達壽命並降低能耗,使其成為暖通空調、石油天然氣和水處理等行業的首選。

低壓應用日益普及

2024年,低壓起動器佔據了相當大的佔有率,這得益於其在商業建築、小規模製造和基礎設施應用中的廣泛應用。這些起動器非常適合控制額定電壓通常低於1,000V的系統中的電機,包括泵、壓縮機和傳送帶。

亞太地區將崛起成為推動力地區

2024年,亞太地區電機起動器市場維持了永續的佔有率,這得益於中國、印度和東南亞等國家工業化的蓬勃發展、基礎設施投資的增加以及能源需求的不斷成長。該地區在全球電機安裝量中佔有相當大的佔有率,尤其是在製造業、建築業和公用事業領域。

電機起動器市場的主要參與者有正泰集團、艾默生電氣、洛瓦托電氣、Kalp Controls、GE Vernova、羅克韋爾自動化、三菱電機、C&S 電氣、西門子、菲尼克斯電氣、富士電機、LS 電氣、WEG、c3controls、Havells India、ABB、CORDYsen、Lauritz Solutions、伊頓、歐姆龍公司、SKN-BENTEX。

為了擴大市場佔有率,電機起動器市場的領導者正專注於產品創新、數位化整合和策略合作夥伴關係。許多企業正在開發內建連接功能的智慧起動器,以實現遠端監控、診斷以及與工業控制系統的無縫整合。其他企業則透過在亞太和拉丁美洲等高成長地區建立製造中心和研發中心,擴大其全球影響力。此外,企業正在加強其服務網路,提供包括調試、維護和培訓在內的端到端支持,以提高客戶忠誠度。此外,企業還部署了客製化定價策略、垂直細分產品線以及在新興市場的積極行銷,以抓住尚未開發的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 電動馬達起動器成本結構分析

- 價格趨勢分析,(美元/單位)

- 按地區

- 按產品

- 新興機會和趨勢

- 馬達起動器的投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分析公司市場佔有率

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 戰略儀表板

- 競爭基準測試

- 創新與技術格局

- 競爭性定價策略基準測試

- 配銷通路策略比較

第5章:市場規模及預測:依產品,2021 - 2034

- 主要趨勢

- 軟啟動器

- 變頻驅動器(VFD)

- 跨線啟動器

- 可逆啟動器

- 混合馬達起動器

- 其他

第6章:市場規模及預測:依保護系統,2021 - 2034

- 主要趨勢

- 電子過載繼電器

- 固態過載保護

- 熱磁性保護

第7章:市場規模及預測:按控制系統,2021 - 2034

- 主要趨勢

- PLC

- 現場總線

第 8 章:市場規模與預測:按電壓,2021 - 2034 年

- 主要趨勢

- 低的

- 中等的

- 高的

第9章:市場規模及預測:依當前,2021 - 2034 年

- 主要趨勢

- > 9 安 - 27 安

- > 27 安 - 90 安

- > 90 安 - 270 安

- > 270 安 - 810 安

- > 810 安

第 10 章:市場規模與預測:按應用,2021 - 2034 年

- 主要趨勢

- 分散式架構

- 控制櫃

- 混合配置

第 11 章:市場規模與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 住宅

- 商業的

- 工業的

第 12 章:市場規模與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 俄羅斯

- 英國

- 義大利

- 西班牙

- 荷蘭

- 奧地利

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 奈及利亞

- 拉丁美洲

- 巴西

- 阿根廷

第13章:公司簡介

- ABB

- C&S Electric

- c3controls

- CG Power & Industrial Solutions

- CHINT Group

- CORDYNE

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric

- GE Vernova

- Havells India

- Kalp Controls

- Lauritz Knudsen Electrical & Automation

- LOVATO ELECTRIC

- LS ELECTRIC

- Mitsubishi Electric

- Omron Corporation

- Phoenix Contact

- Rockwell Automation

- Schneider Electric

- Siemens

- SKN-BENTEX

- WEG

The global motor starter market was estimated at USD 7.4 billion in 2024 and is expected to grow from USD 7.8 billion in 2025 to USD 12 billion by 2034, at a CAGR of 5%, as per the latest report published by Global Market Insights Inc.

With a strong focus on energy savings and reducing operational costs, industries are investing in advanced motor starters, especially soft starters and intelligent starters that help reduce power surges, manage load, and enhance motor efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $12 Billion |

| CAGR | 5% |

Variable Frequency Drives to Gain Traction

The variable frequency drives (VFD) segment held a significant share in 2024, owing to its superior energy efficiency, precise motor control, and reduced mechanical stress on equipment. VFDs not only regulate motor speed but also help extend motor life and lower energy consumption, making them a preferred choice across industries such as HVAC, oil & gas, and water treatment.

Rising Adoption of Low Voltage

The low voltage held a sizeable share in 2024, driven by its widespread use in commercial buildings, small-scale manufacturing, and infrastructure applications. These starters are ideal for controlling motors in systems with voltage ratings typically below 1,000V, including pumps, compressors, and conveyors.

Asia Pacific to Emerge as a Propelling Region

Asia Pacific motor starter market held a sustainable share in 2024, fueled by booming industrialization, rising investments in infrastructure, and growing energy demand across countries like China, India, and Southeast Asia. This region accounts for a significant share of global motor installations, particularly in manufacturing, construction, and utilities.

Major players in the motor starter market are CHINT Group, Emerson Electric, LOVATO ELECTRIC, Kalp Controls, GE Vernova, Rockwell Automation, Mitsubishi Electric, C&S Electric, Siemens, Phoenix Contact, Fuji Electric, LS ELECTRIC, WEG, c3controls, Havells India, ABB, CORDYNE, Lauritz Knudsen Electrical & Automation, Danfoss, Schneider Electric, CG Power & Industrial Solutions, Eaton, Omron Corporation, SKN-BENTEX.

To expand their presence, leading players in the motor starter market are focusing on product innovation, digital integration, and strategic partnerships. Many are developing smart starters with built-in connectivity, allowing remote monitoring, diagnostics, and seamless integration with industrial control systems. Others are expanding their global footprint by establishing manufacturing hubs and R&D centers in high-growth regions like the Asia Pacific and Latin America. In addition, companies are strengthening their service networks, offering end-to-end support that includes commissioning, maintenance, and training to enhance customer loyalty. Tailored pricing strategies, vertical-specific product lines, and aggressive marketing in emerging markets are also being deployed to capture untapped demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Protection system trends

- 2.1.4 Control system trends

- 2.1.5 Voltage trends

- 2.1.6 Current trends

- 2.1.7 Application trends

- 2.1.8 End use trends

- 2.1.9 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.7 Cost structure analysis of motor starters

- 3.8 Price trend analysis, (USD/Unit)

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Emerging opportunities & trends

- 3.10 Investment analysis & future outlook for the motor starter

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

- 4.7 Competitive pricing strategy benchmarking

- 4.8 Distribution channel strategy comparison

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 Soft starters

- 5.3 Variable frequency drives (VFDs)

- 5.4 Across-the-line starters

- 5.5 Reversing starters

- 5.6 Hybrid motor starters

- 5.7 Others

Chapter 6 Market Size and Forecast, By Protection System, 2021 - 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 Electronic overload relays

- 6.3 Solid-state overload protection

- 6.4 Thermal-magnetic protection

Chapter 7 Market Size and Forecast, By Control System, 2021 - 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 PLC

- 7.3 Fieldbus

Chapter 8 Market Size and Forecast, By Voltage, 2021 - 2034 (Units & USD Million)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Size and Forecast, By Current, 2021 - 2034 (Units & USD Million)

- 9.1 Key trends

- 9.2 > 9 A - 27 A

- 9.3 > 27 A - 90 A

- 9.4 > 90 A - 270 A

- 9.5 > 270 A - 810 A

- 9.6 > 810 A

Chapter 10 Market Size and Forecast, By Application, 2021 - 2034 (Units & USD Million)

- 10.1 Key trends

- 10.2 Distributed architecture

- 10.3 Control cabinet

- 10.4 Hybrid configuration

Chapter 11 Market Size and Forecast, By End Use, 2021 - 2034 (Units & USD Million)

- 11.1 Key trends

- 11.2 Residential

- 11.3 Commercial

- 11.4 Industrial

Chapter 12 Market Size and Forecast, By Region, 2021 - 2034 (Units & USD Million)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 Russia

- 12.3.4 UK

- 12.3.5 Italy

- 12.3.6 Spain

- 12.3.7 Netherlands

- 12.3.8 Austria

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 South Korea

- 12.4.4 India

- 12.4.5 Australia

- 12.4.6 New Zealand

- 12.4.7 Indonesia

- 12.5 Middle East & Africa

- 12.5.1 Saudi Arabia

- 12.5.2 UAE

- 12.5.3 Qatar

- 12.5.4 Egypt

- 12.5.5 South Africa

- 12.5.6 Nigeria

- 12.6 Latin America

- 12.6.1 Brazil

- 12.6.2 Argentina

Chapter 13 Company Profiles

- 13.1 ABB

- 13.2 C&S Electric

- 13.3 c3controls

- 13.4 CG Power & Industrial Solutions

- 13.5 CHINT Group

- 13.6 CORDYNE

- 13.7 Danfoss

- 13.8 Eaton

- 13.9 Emerson Electric

- 13.10 Fuji Electric

- 13.11 GE Vernova

- 13.12 Havells India

- 13.13 Kalp Controls

- 13.14 Lauritz Knudsen Electrical & Automation

- 13.15 LOVATO ELECTRIC

- 13.16 LS ELECTRIC

- 13.17 Mitsubishi Electric

- 13.18 Omron Corporation

- 13.19 Phoenix Contact

- 13.20 Rockwell Automation

- 13.21 Schneider Electric

- 13.22 Siemens

- 13.23 SKN-BENTEX

- 13.24 WEG

2026年全球磁力啟動器市場報告

2026年全球磁力啟動器市場報告 危險區域馬達啟動器市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材質、最終用戶、部署類型和功能分類2026年全球封閉式馬達起動器市場報告

危險區域馬達啟動器市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材質、最終用戶、部署類型和功能分類2026年全球封閉式馬達起動器市場報告 直通式馬達啟動器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

直通式馬達啟動器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 2032 年馬達起動器市場預測:按類型、電壓、應用、最終用戶和地區進行的全球分析

2032 年馬達起動器市場預測:按類型、電壓、應用、最終用戶和地區進行的全球分析 中東和非洲危險場所的馬達起動器:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)拉丁美洲危險區域馬達起動器:市場佔有率分析、產業趨勢和成長預測(2025-2030)馬達起動機:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)單相自動馬達啟動器市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032

中東和非洲危險場所的馬達起動器:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)拉丁美洲危險區域馬達起動器:市場佔有率分析、產業趨勢和成長預測(2025-2030)馬達起動機:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)單相自動馬達啟動器市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032