|

市場調查報告書

商品編碼

1833665

血液透析導管市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Hemodialysis Catheters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

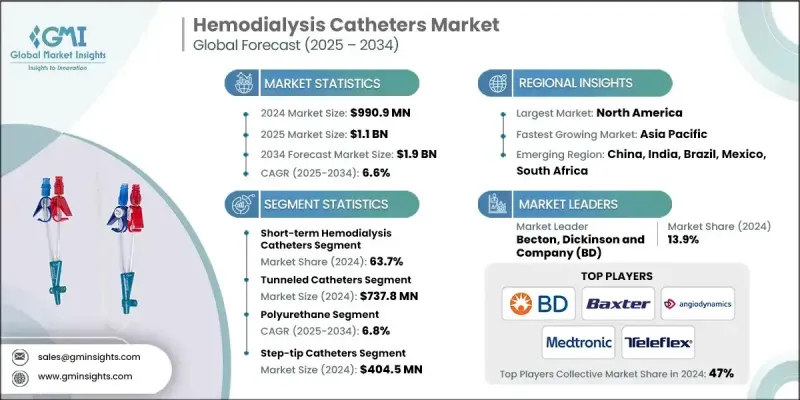

2024 年全球血液透析導管市場價值為 9.909 億美元,預計將以 6.6% 的複合年成長率成長,到 2034 年達到 19 億美元。

該市場的穩定成長很大程度上與慢性腎臟病 (CKD) 和末期腎病 (ESRD) 盛行率的上升有關,這帶來了對透析治療的巨大需求。人們對腎臟替代療法的認知不斷提高,進一步加速了各地區的應用。此外,導管設計的技術進步以及先進、生物相容性和抗感染材料的引入,正在推動產業擴張。全球人口快速老化,更容易受到腎臟相關併發症的影響,這也擴大了患者群體,並增加了對長期透析的需求。同時,醫療保健支出的增加、透析中心的不斷建立以及政府支持的加強基礎設施的舉措,使得人們能夠更廣泛地獲得挽救生命的治療。醫療保健機構正在優先投資透析服務,而製造商則不斷創新,設計出更安全、更有效率的導管,從而支持預測期內的持續成長。這些因素,加上診斷方案的改進和腎臟健康宣傳活動的發展,正在推動全球透析採用率的提高。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 9.909億美元 |

| 預測值 | 19億美元 |

| 複合年成長率 | 6.6% |

短期血液透析導管市場在2024年佔據63.7%的市場佔有率,這得益於其在急性腎損傷和緊急情況下提供快速血管通路的重要作用。這類導管因其易於插入、成本效益高且可立即啟動透析,廣泛應用於醫院和重症監護環境。急性腎損傷(通常與外科手術、敗血症和心血管併發症相關)的發生率不斷上升,並持續推高了對這些設備的需求。

隧道導管細分市場在2024年的收入為7.378億美元,確立了其在市場上的主導地位。這些導管旨在為正在接受透析的患者提供可靠的長期血管通路。其皮下隧道設計可降低感染風險並提供卓越的穩定性,同時與非隧道產品相比,其更高的耐用性和更高的患者舒適度使其成為醫療保健提供者的首選。

2024年,美國血液透析導管市場規模達4.375億美元,這主要得益於慢性腎臟病(CKD)和末期腎臟病(ESRD)患者數量的不斷成長。糖尿病、高血壓和肥胖病例激增,以及鼓勵早期診斷和治療的認知度提升等因素共同推動了這一市場的成長。憑藉先進的醫療基礎設施、數量眾多的透析中心以及隧道式導管和生物相容性導管等創新導管的快速普及,美國仍然是全球血液透析導管市場成長的關鍵貢獻者。

血液透析導管產業主要的活躍公司包括 Vygon、Amecath、Cook Medical、Polymed、Mozarc Medical、Delta Med、Teleflex、B. Braun、ST Stone Medical、Merit Medical、Medcomp、AngioDynamics、Becton、Dickinson and Company (BD)、Healthline Medical Products、Baxter 和 Bain Medical Equipment。為了鞏固市場地位,血液透析導管產業的公司正優先考慮創新、地理擴張和策略合作。製造商正專注於先進的導管設計,以提高生物相容性、降低感染風險並改善流動性能,以滿足日益成長的患者和臨床醫生需求。他們正在與醫療保健提供者和透析中心建立策略聯盟,以確保長期供應協議並提高產品可及性。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 慢性腎臟疾病和末期腎臟病盛行率上升

- 促進慢性腎臟病意識的促進舉措

- 腎臟替代治療數量不斷增加

- 血液透析導管的技術進步

- 全球腎臟捐贈者短缺

- 產業陷阱與挑戰

- 對腎臟相關疾病的認知不足

- 血液透析導管相關併發症

- 市場機會

- 擴展居家透析和遠端患者監控解決方案

- 抗菌和生物相容性導管材料的採用日益增多

- 醫療保健基礎設施不斷完善的新興市場具有成長潛力

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 轉向長期使用隧道式帶囊導管

- 抗菌塗層和肝素塗層導管的進展

- 微創導管置入技術的應用日益廣泛

- 新興技術

- 開發藥物洗脫導管以最大限度地減少感染和血栓形成

- 嵌入感測器的智慧導管,可即時監測血流和凝血情況

- 針對患者特定解剖結構設計的 3D 列印客製化導管

- 當前的技術趨勢

- 未來市場趨勢

- 轉向永久性血管通路以限制對導管的依賴

- 居家透析的使用日益成長,推動了先進導管的需求

- 遠端導管監測的數位健康整合

- 市場進入策略

- 定價分析

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲和中東地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按導管類型,2021 - 2034

- 主要趨勢

- 短期血液透析導管

- 長期血液透析導管

第6章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 隧道導管

- 帶套囊隧道導管

- 無袖套隧道導管

- 非隧道導管

第7章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 聚氨酯

- 矽酮

第8章:市場估計與預測:按提示配置,2021 - 2034 年

- 主要趨勢

- 階梯式導管

- 尖端分叉導管

- 對稱導管

- 其他尖端配置

第9章:市場估計與預測:按流明,2021 - 2034 年

- 主要趨勢

- 單腔

- 雙腔

- 三腔

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Amecath

- AngioDynamics

- B. Braun

- Bain Medical Equipment

- Baxter

- Becton, Dickinson and Company (BD)

- Cook Medical

- Delta Med

- Healthline Medical Products

- Medcomp

- Merit Medical

- Mozarc Medical

- Polymed

- ST Stone Medical

- Teleflex

- Vygon

The Global Hemodialysis Catheters Market was valued at USD 990.9 million in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 1.9 billion by 2034.

The steady rise in this market is largely linked to the increasing prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), which creates significant demand for dialysis treatments. Growing awareness about renal replacement therapies has further accelerated adoption across regions. Additionally, technological progress in catheter design and the introduction of advanced, biocompatible, and infection-resistant materials are fueling industry expansion. The rapidly aging global population, which is more vulnerable to kidney-related complications, is also widening the patient base and boosting the need for long-term dialysis access. At the same time, greater healthcare spending, the rising establishment of dialysis centers, and government-backed initiatives to strengthen infrastructure are enabling broader access to life-saving therapies. Healthcare organizations are prioritizing investments in dialysis services while manufacturers continue to innovate with safer and more efficient catheter designs, supporting sustained growth over the forecast period. These factors, along with improved diagnosis programs and awareness campaigns on renal health, are driving higher adoption rates worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $990.9 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 6.6% |

The short-term hemodialysis catheters segment held a 63.7% share in 2024, supported by their essential role in providing fast vascular access in acute kidney injury and emergency cases. These catheters are widely utilized in hospital and critical care environments because they can be inserted easily, offer cost efficiency, and allow immediate dialysis initiation. The rising incidence of acute kidney injury, often associated with surgical interventions, sepsis, and cardiovascular complications, continues to increase demand for these devices.

The tunneled catheters segment generated USD 737.8 million in 2024, establishing its dominance in the market. These catheters are designed to deliver dependable long-term vascular access for patients undergoing ongoing dialysis. Their subcutaneous tunneling reduces infection risks and provides superior stability, while enhanced durability and greater patient comfort compared to non-tunneled products make them the preferred option among healthcare providers.

U.S. Hemodialysis Catheters Market was valued at USD 437.5 million in 2024, driven by the rising number of patients diagnosed with CKD and ESRD. Contributing factors include a surge in diabetes, hypertension, and obesity cases, alongside improved awareness programs that encourage early diagnosis and treatment. With advanced healthcare infrastructure, a strong presence of dialysis centers, and rapid adoption of innovative catheters such as tunneled and biocompatible designs, the country remains a key contributor to global growth.

Key companies active in the Hemodialysis Catheters Industry include Vygon, Amecath, Cook Medical, Polymed, Mozarc Medical, Delta Med, Teleflex, B. Braun, ST Stone Medical, Merit Medical, Medcomp, AngioDynamics, Becton, Dickinson and Company (BD), Healthline Medical Products, Baxter, and Bain Medical Equipment. To strengthen their market position, companies in the hemodialysis catheters sector are prioritizing innovation, geographic expansion, and strategic collaborations. Manufacturers are focusing on advanced catheter designs with enhanced biocompatibility, lower infection risks, and better flow performance to address growing patient and clinician demands. Strategic alliances with healthcare providers and dialysis centers are being pursued to secure long-term supply agreements and improve product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Catheter type trends

- 2.2.3 Product trends

- 2.2.4 Material trends

- 2.2.5 Tip configuration trends

- 2.2.6 Lumen trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic kidney disorders and end-stage renal disease

- 3.2.1.2 Facilitative initiatives to promote chronic kidney disorder awareness

- 3.2.1.3 Rising number of renal replacement therapy

- 3.2.1.4 Technological advancements in hemodialysis catheters

- 3.2.1.5 Shortage of kidney donors globally

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Low awareness about kidney-related disorders

- 3.2.2.2 Complications associated with hemodialysis catheters

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of home-based dialysis and remote patient monitoring solutions

- 3.2.3.2 Increasing adoption of antimicrobial and biocompatible catheter materials

- 3.2.3.3 Growth potential in emerging markets with rising healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Shift toward tunneled cuffed catheters for long-term use

- 3.5.1.2 Advancements in antimicrobial-coated and heparin-coated catheters

- 3.5.1.3 Rising adoption of minimally invasive catheter placement techniques

- 3.5.2 Emerging technologies

- 3.5.2.1 Development of drug-eluting catheters to minimize infection and thrombosis

- 3.5.2.2 Smart catheters with embedded sensors for real-time monitoring of flow and clotting

- 3.5.2.3 3D-printed customized catheters designed for patient-specific anatomy

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.6.1 Shift toward permanent vascular access to limit catheter reliance

- 3.6.2 Growing use of home dialysis driving advanced catheter demand

- 3.6.3 Integration of digital health for remote catheter monitoring

- 3.7 Go-to-market strategies

- 3.8 Pricing analysis

- 3.9 GAP analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LAMEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Merger and acquisition

- 4.7.2 Partnership and collaboration

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Catheter Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Short-term hemodialysis catheters

- 5.3 Long-term hemodialysis catheters

Chapter 6 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tunneled catheters

- 6.2.1 Cuffed tunneled catheters

- 6.2.2 Non-cuffed tunneled catheters

- 6.5 Non-tunneled catheters

Chapter 7 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Polyurethane

- 7.3 Silicone

Chapter 8 Market Estimates and Forecast, By Tip Configuration, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Step-tip catheters

- 8.3 Split-tip catheters

- 8.4 Symmetric catheters

- 8.5 Other tip configurations

Chapter 9 Market Estimates and Forecast, By Lumen, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Single-lumen

- 9.3 Double-lumen

- 9.4 Triple-lumen

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amecath

- 11.2 AngioDynamics

- 11.3 B. Braun

- 11.4 Bain Medical Equipment

- 11.5 Baxter

- 11.6 Becton, Dickinson and Company (BD)

- 11.7 Cook Medical

- 11.8 Delta Med

- 11.9 Healthline Medical Products

- 11.10 Medcomp

- 11.11 Merit Medical

- 11.12 Mozarc Medical

- 11.13 Polymed

- 11.14 ST Stone Medical

- 11.15 Teleflex

- 11.16 Vygon

血液透析導管市場:2026-2032年全球市場預測(依產品類型、形狀、尖端類型、材質、管腔結構、插入部位、最終用戶和病患類型分類)

血液透析導管市場:2026-2032年全球市場預測(依產品類型、形狀、尖端類型、材質、管腔結構、插入部位、最終用戶和病患類型分類) 2026-2034年全球透析導管市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球透析導管市場規模、佔有率、趨勢和成長分析報告 透析導管市場機會、成長要素、產業趨勢分析及2026-2035年預測。

透析導管市場機會、成長要素、產業趨勢分析及2026-2035年預測。 透析導管市場(依產品類型分類)

透析導管市場(依產品類型分類) 2026年全球血液透析導管市場報告全球血液透析導管市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球血液透析導管市場報告全球血液透析導管市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球透析導管市場:市場規模、佔有率和趨勢分析(2026-2032 年)2025年全球血液透析機導管市場報告

全球透析導管市場:市場規模、佔有率和趨勢分析(2026-2032 年)2025年全球血液透析機導管市場報告 血液透析導管市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、材料、應用、最終用戶、地區和競爭細分,2020-2030 年

血液透析導管市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、材料、應用、最終用戶、地區和競爭細分,2020-2030 年 血液透析機導管市場規模、佔有率和趨勢分析報告:按設計、應用、材料、形狀、組件、性別、最終用途、地區和細分市場預測,2025-2033 年

血液透析機導管市場規模、佔有率和趨勢分析報告:按設計、應用、材料、形狀、組件、性別、最終用途、地區和細分市場預測,2025-2033 年