|

市場調查報告書

商品編碼

1833638

睡眠呼吸中止設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Sleep Apnea Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

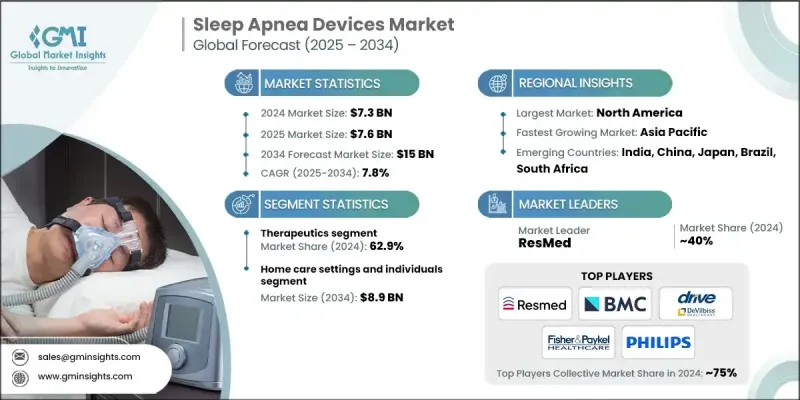

2024 年全球睡眠呼吸中止設備市場價值為 73 億美元,預計到 2034 年將以 7.8% 的複合年成長率成長至 150 億美元。

這一成長的促進因素包括全球睡眠呼吸中止症病例數量的增加、人們對睡眠障礙認知的提高以及對先進攜帶式治療解決方案日益成長的需求。睡眠呼吸中止症設備用於診斷和管理睡眠呼吸障礙,幫助維持呼吸道暢通並有效監測患者的睡眠健康。隨著越來越多的人意識到持續打鼾、白天疲勞和注意力不集中等症狀,醫療諮詢和睡眠障礙診斷變得越來越普遍。睡眠測試方法的創新,包括實驗室多導睡眠圖和家用測試套件,進一步促進了診斷率的飆升。隨著越來越多的患者獲得正式診斷,對持續性正壓呼吸器 (CPAP)、雙水平氣道正壓通氣 (BiPAP) 和其他睡眠呼吸中止症治療技術等設備的需求持續成長。這些設備有助於降低未經治療的睡眠呼吸中止症的健康風險,改善患者護理,並提高整體生活品質。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 73億美元 |

| 預測值 | 150億美元 |

| 複合年成長率 | 7.8% |

2024年,診斷細分市場佔了37.1%的市佔率。這一成長源於人們對早期睡眠障礙檢測的日益關注,以及緊湊型人工智慧診斷工具的普及。隨著這些技術日益成熟且價格合理,睡眠呼吸中止症篩檢對患者和醫療服務提供者來說都變得更快、更方便。居家檢測和即時資料分析的發展持續提升診斷能力,並促進市場擴張。

2024年,家庭護理機構和個人護理市場佔據56.9%的市場佔有率,預計到2034年將達到89億美元,這得益於臨床環境之外對經濟高效的長期治療方案日益成長的需求。居家管理睡眠呼吸中止症有助於減少頻繁就診和住院費用。家庭護理保險覆蓋範圍的擴大以及經濟實惠的治療方案的出現,正在幫助更多人群更容易獲得家庭睡眠治療,鼓勵更多人以獨立且經濟的方式管理自身疾病。

2024年,北美睡眠呼吸中止設備市場佔37.6%的市場佔有率,這得益於其強大的醫療基礎設施、完善的報銷體係以及公眾對睡眠相關健康問題的高度認知。該地區繼續大力推廣治療性和診斷性睡眠呼吸中止症技術。遠端監控平台與互聯健康解決方案的整合正在進一步提升該地區的患者護理水準。 Drive DeVilbiss、BMC、ResMed、Teleflex、Fisher & Paykel和飛利浦等主要產業參與者透過提供包括持續正壓通氣(CPAP)、雙水平正壓通氣(BiPAP)和遠端睡眠測試解決方案在內的全面產品組合,鞏固了其在北美市場的地位。

活躍於全球睡眠呼吸中止設備市場的關鍵公司包括 Cadwell、DynaFlex、Asahi KASEI、Glidewell、Apnea Sciences、SomnoMed、NIHON KOHDEN、Natus、WEINMANN 等。為了鞏固其在全球睡眠呼吸中止設備市場的地位,各公司正在部署多項核心策略。這些策略包括持續投資研發,以提高設備的準確性、便攜性和患者舒適度。各公司正在引入支援即時資料監控和遠距醫療相容性的互聯技術。此外,與睡眠診所、家庭護理提供者和保險網路的合作有助於擴大分銷。行銷計劃著重於提高公眾意識和鼓勵早期診斷。此外,公司正在透過監管部門的批准進入新市場並建立可擴展的生產以滿足日益成長的全球需求,特別是在家庭護理環境中。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 睡眠呼吸中止症及相關合併症的發生率不斷上升

- 對攜帶式高效能睡眠呼吸中止解決方案的需求不斷成長

- 人們對睡眠呼吸中止症和睡眠障礙的認知不斷提高

- 人口老化加劇需求

- 技術進步

- 產業陷阱與挑戰

- 缺乏對睡眠呼吸中止症治療的依從性

- 產品召回與安全問題

- 市場機會

- 向新興市場擴張

- 人工智慧與數位健康融合

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 現有技術

- 新興技術

- 未來市場趨勢

- 報銷場景

- 睡眠呼吸中止症植入物在睡眠呼吸中止症治療設備中的作用不斷演變

- 管道分析

- 投資前景

- 啟動場景

- 2024年定價分析

- 波特的分析

- PESTEL分析

- 差距分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲和中東地區

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 療法

- 氣道清除系統

- 氣道正壓通氣 (PAP) 裝置

- 持續性呼吸道正壓通氣 (CPAP) 設備

- 雙水平氣道正壓通氣 (BiPAP) 裝置

- 自動氣道正壓通氣 (APAP) 裝置

- 自適應伺服通氣 (ASV) 設備

- 口腔器具

- 下顎前移裝置

- 舌固定裝置

- 快速上顎擴弓

- 護齒套

- 其他療法

- 診斷

- 多導睡眠圖(PSG)設備

- 動態 PSG 設備

- 臨床 PSG 設備

- 體動記錄系統

- 脈搏血氧儀

- 居家睡眠測試 (HST) 設備

- 類型 2

- 類型 3

- 類型 4

- 呼吸描記器

- 多導睡眠圖(PSG)設備

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 居家照護機構及個人

- 睡眠實驗室和醫院

第7章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Asahi KASEI

- BMC

- Cadwell

- Drive DeVilbiss

- FISHER & PAYKEL

- natus

- NIHON KOHDEN

- Philips

- ResMed

- Teleflex

- WEINMANN

- Glidewell

- DynaFlex

- SomnoMed

- Apnea Sciences

The Global Sleep Apnea Devices Market was valued at USD 7.3 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 15 billion by 2034.

This growth is being driven by the rising number of sleep apnea cases worldwide, increased awareness around sleep disorders, and growing demand for advanced, portable treatment solutions. Sleep apnea devices are used both for diagnosing and managing sleep-disordered breathing, helping to keep the airway open and monitor patients' sleep health effectively. With more individuals recognizing symptoms such as persistent snoring, fatigue during the day, and difficulty focusing, medical consultations and sleep disorder diagnoses are becoming more common. Innovations in sleep testing methods, including lab-based polysomnography and home testing kits, are further contributing to this surge in diagnosis rates. As more patients are formally diagnosed, demand for devices like CPAP, BiPAP, and other sleep apnea treatment technologies continues to rise. These devices are instrumental in reducing the health risks of untreated sleep apnea, offering improved patient care and boosting overall quality of life.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $15 Billion |

| CAGR | 7.8% |

In 2024, the diagnostics segment held a 37.1% share. This growth stems from heightened attention to early sleep disorder detection and greater access to compact and AI-powered diagnostic tools. As these technologies become more sophisticated and affordable, screening for sleep apnea is becoming quicker and more convenient for both patients and providers. The evolution of home-based testing and real-time data analysis continues to enhance diagnostic capabilities and market expansion.

The home care settings and individuals segment held a share of 56.9% in 2024 and is expected to generate USD 8.9 billion by 2034, fueled by the rising demand for cost-effective, long-term treatment solutions outside of clinical settings. Managing sleep apnea at home helps cut down on frequent clinic visits and hospitalization expenses. Expanded insurance coverage for home-based care and the availability of budget-friendly treatment options are helping make home sleep therapy more accessible to a wide population base, encouraging more people to manage their condition independently and affordably.

North America Sleep Apnea Devices Market held a 37.6% share in 2024, supported by robust healthcare infrastructure, a well-established reimbursement ecosystem, and high public awareness around sleep-related health issues. The region continues to see strong early adoption of both therapeutic and diagnostic sleep apnea technologies. Integration of remote monitoring platforms and connected health solutions is further advancing patient care in the region. Major industry players such as Drive DeVilbiss, BMC, ResMed, Teleflex, Fisher & Paykel, and Philips have cemented their position in North America by offering comprehensive portfolios that include CPAP, BiPAP, and remote sleep testing solutions.

Key companies active in the Global Sleep Apnea Devices Market Include Cadwell, DynaFlex, Asahi KASEI, Glidewell, Apnea Sciences, SomnoMed, NIHON KOHDEN, Natus, WEINMANN, and others. To strengthen their position in the global sleep apnea devices market, companies are deploying several core strategies. These include consistent investment in research and development to enhance device accuracy, portability, and patient comfort. Firms are introducing connected technologies that support real-time data monitoring and telehealth compatibility. In addition, partnerships with sleep clinics, home care providers, and insurance networks are helping expand distribution. Marketing initiatives focus on increasing public awareness and encouraging early diagnosis. Moreover, companies are entering new markets through regulatory approvals and building scalable production to meet rising global demand, particularly in home care settings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of sleep apnea and related comorbidities

- 3.2.1.2 Growing demand for portable, high-performance sleep apnea solutions

- 3.2.1.3 Surging awareness of sleep apnea and sleep disorders

- 3.2.1.4 Rising aging population amplifying demand

- 3.2.1.5 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of adherence to sleep apnea treatment

- 3.2.2.2 Product recalls and safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 AI and digital health integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.8 Evolving role of sleep apnea implants within sleep apnea treatment devices

- 3.9 Pipeline analysis

- 3.10 Investment landscape

- 3.11 Start-up scenario

- 3.12 Pricing analysis, 2024

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutics

- 5.2.1 Airway clearance systems

- 5.2.2 Positive airway pressure (PAP) devices

- 5.2.2.1 Continuous positive airway pressure (CPAP) devices

- 5.2.2.2 Bilevel positive airway pressure (BiPAP) devices

- 5.2.2.3 Automatic positive airway pressure (APAP) devices

- 5.2.3 Adaptive servo-ventilation (ASV) devices

- 5.2.4 Oral appliances

- 5.2.4.1 Mandibular advancement devices

- 5.2.4.2 Tongue-retaining devices

- 5.2.4.3 Rapid maxillary expansion

- 5.2.4.4 Mouth guards

- 5.2.5 Other therapeutics

- 5.3 Diagnostics

- 5.3.1 Polysomnography (PSG) device

- 5.3.1.1 Ambulatory PSG devices

- 5.3.1.2 Clinical PSG devices

- 5.3.2 Actigraphy systems

- 5.3.3 Pulse oximeters

- 5.3.4 Home sleep testing (HST) devices

- 5.3.4.1 Type 2

- 5.3.4.2 Type 3

- 5.3.4.3 Type 4

- 5.3.5 Respiratory polygraph

- 5.3.1 Polysomnography (PSG) device

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Home care settings and individuals

- 6.3 Sleep laboratories and hospitals

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Asahi KASEI

- 8.2 BMC

- 8.3 Cadwell

- 8.4 Drive DeVilbiss

- 8.5 FISHER & PAYKEL

- 8.6 natus

- 8.7 NIHON KOHDEN

- 8.8 Philips

- 8.9 ResMed

- 8.10 Teleflex

- 8.11 WEINMANN

- 8.12 Glidewell

- 8.13 DynaFlex

- 8.14 SomnoMed

- 8.15 Apnea Sciences

睡眠呼吸中止症治療設備市場規模、佔有率、趨勢和預測:按產品類型、最終用戶和地區分類,2026-2034年

睡眠呼吸中止症治療設備市場規模、佔有率、趨勢和預測:按產品類型、最終用戶和地區分類,2026-2034年 2026年全球口腔睡眠呼吸中止症治療設備市場報告2026年全球睡眠呼吸中止設備市場報告

2026年全球口腔睡眠呼吸中止症治療設備市場報告2026年全球睡眠呼吸中止設備市場報告 2026-2034年全球口腔睡眠呼吸中止症候群治療設備市場規模、佔有率、趨勢和成長分析報告睡眠呼吸中止症治療設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,2026-2034 年日本睡眠呼吸中止設備市場報告(按產品類型(治療設備、診斷設備)、最終用戶(醫院和診所、睡眠實驗室、家庭護理機構及其他)和地區分類,2026-2034 年)

2026-2034年全球口腔睡眠呼吸中止症候群治療設備市場規模、佔有率、趨勢和成長分析報告睡眠呼吸中止症治療設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,2026-2034 年日本睡眠呼吸中止設備市場報告(按產品類型(治療設備、診斷設備)、最終用戶(醫院和診所、睡眠實驗室、家庭護理機構及其他)和地區分類,2026-2034 年) 睡眠呼吸中止症治療設備市場規模、佔有率和成長分析(按產品、最終用戶、年齡層、性別和地區分類)—2026-2033年產業預測

睡眠呼吸中止症治療設備市場規模、佔有率和成長分析(按產品、最終用戶、年齡層、性別和地區分類)—2026-2033年產業預測 睡眠呼吸中止設備市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、治療設備、診斷設備、適應症類型、最終用戶、地區和競爭格局分類,2020-2030 年預測)

睡眠呼吸中止設備市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、治療設備、診斷設備、適應症類型、最終用戶、地區和競爭格局分類,2020-2030 年預測) 睡眠呼吸中止設備-市場洞察、競爭格局及至2032年預測

睡眠呼吸中止設備-市場洞察、競爭格局及至2032年預測 全球睡眠呼吸中止症口腔器材市場

全球睡眠呼吸中止症口腔器材市場