|

市場調查報告書

商品編碼

1833634

肝素市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Heparin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

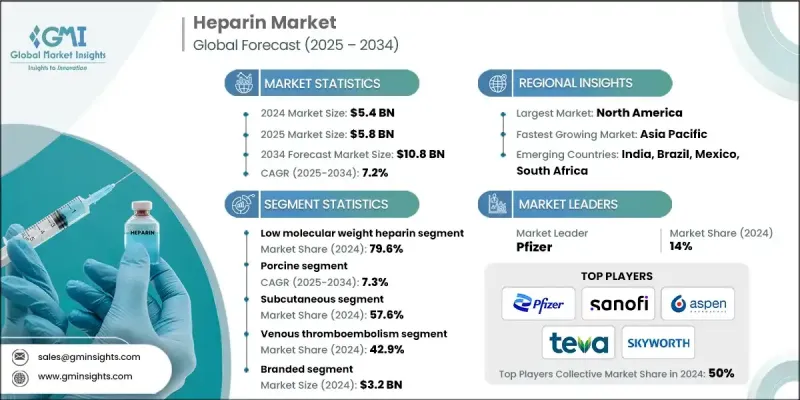

2024 年全球肝素市場價值為 54 億美元,預計到 2034 年將以 7.2% 的複合年成長率成長至 108 億美元。

需求成長主要歸因於心血管和血栓性疾病的激增,以及全球外科手術數量的不斷增加。肝素在透析、癌症治療和各種醫療器材應用等領域的應用也越來越廣泛。醫療基礎設施的改善進一步促進了肝素治療的擴展,尤其是在拉丁美洲和亞太地區的新興經濟體。持續專注於創新以及開發更有效、副作用更少的抗凝血療法,正在推動市場發展。研究計畫正在推動產品進步,使基於肝素的治療方案更容易在醫院、診所和家庭護理機構中獲得。隨著心血管疾病持續給全球醫療保健系統帶來沉重負擔,抗凝血技術的不斷發展預計將加速市場應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 54億美元 |

| 預測值 | 108億美元 |

| 複合年成長率 | 7.2% |

低分子量肝素 (LMWH) 市場在 2024 年佔據 79.6% 的市場佔有率,這得益於其多項臨床優勢,包括良好的藥物動力學、較低的出血風險、易於給藥以及適合門診治療。 LMWH 的治療效果可預測,且監測頻率較低,因此成為醫療服務提供者和患者的首選。

豬源肝素市場在2024年的複合年成長率為7.3%,這得益於其穩定的供應、臨床可靠性以及肝素誘導的血小板減少症(HIT)等併發症的發生率較低。這類肝素是生產最廣泛使用的低分子肝素(LMWH)不可或缺的原料,而且仍是大規模生產的基石。

2024年,美國肝素市場產值達28億美元。美國心血管疾病和慢性疾病的高發生率導致對抗凝血治療的需求強勁。美國食品藥物管理局(FDA)的監管支持以及優惠的報銷框架,持續促進了品牌藥和學名藥肝素製劑的廣泛接受。醫院和家庭護理環境中預充式注射器和自動注射器的使用日益增多,也促進了這些藥物的安全便捷使用。

全球肝素產業的主要領導者包括利奧製藥、輝瑞、Suanfarma、深圳海普瑞藥業、Bioiberica、Amphastar、賽諾菲、雷迪博士實驗室、常州千紅生物製藥、梯瓦製藥工業、費森尤斯卡比、Aspen Pharmacare、南京健友生化製藥、Rovi Laboratorios Farmaceacecosuti和煙台東生化。肝素市場的領導企業正在利用策略合作、垂直整合和產能擴張等組合來鞏固其市場地位。一些公司正在投資研發,以開發療效更好、副作用更少的下一代抗凝血劑。其他公司正在建立合作夥伴關係和許可協議,以拓寬分銷管道並確保原料供應。向高成長新興市場的地域擴張也已成為關鍵的關注領域。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 全球心血管疾病盛行率上升

- 人口老化與外科手術

- 擴大醫院基礎設施和家庭護理

- 政府和機構健康計劃

- 產業陷阱與挑戰

- 品牌 LMWH 和生物相似藥成本高昂

- 供應鏈中斷和原料依賴

- 市場機會

- 合成和重組肝素的開發

- 醫療保健投資不斷增加的新興市場

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 未來市場趨勢

- 技術格局

- 目前技術

- 新興技術

- 專利格局

- 定價分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 低分子量肝素

- 普通肝素

- 超低分子量肝素/合成肝素

第6章:市場估計與預測:按來源,2021 - 2034 年

- 主要趨勢

- 豬

- 牛

第7章:市場估計與預測:按管理路線,2021 - 2034 年

- 主要趨勢

- 靜脈

- 皮下

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 靜脈血栓栓塞症

- 心房顫動/撲動

- 冠狀動脈疾病

- 其他應用

第9章:市場估計與預測:按類型,2021 - 2034

- 主要趨勢

- 品牌

- 泛型

第 10 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 診所

- 門診手術中心(ASC)

- 其他最終用途

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 12 章:公司簡介

- Amphastar

- Aspen Pharmacare

- Bioiberica

- Changzhou Qianhong Biopharma

- Dr. Reddy's Laboratories

- Fresenius Kabi

- Laboratorios Farmaceuticos ROVI

- Leo Pharma

- Nanjing King-Friend Biochemical Pharmaceutical

- Pfizer

- Sanofi

- Shenzhen Hepalink Pharmaceuticals

- Suanfarma

- Teva Pharmaceutical Industries

The Global Heparin Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 10.8 billion by 2034.

The increasing demand is largely attributed to a surge in cardiovascular and thrombotic conditions, coupled with a growing number of surgical interventions worldwide. Heparin is also seeing broader adoption in fields like dialysis, cancer treatment, and various medical device applications. These therapeutic expansions are further amplified by improvements in healthcare infrastructure, particularly in emerging economies across Latin America and the Asia-Pacific region. The continued focus on innovation and the development of more effective anticoagulant therapies with fewer adverse effects is pushing market dynamics forward. Research initiatives are fueling product advancements, making heparin-based treatment options more accessible across hospitals, clinics, and home care facilities. As cardiovascular disease continues to place a substantial burden on healthcare systems globally, the ongoing evolution of anticoagulation technology is expected to accelerate market adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.4 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 7.2% |

The low molecular weight heparin (LMWH) segment held 79.6% share in 2024, driven by several clinical advantages, including its favorable pharmacokinetics, lower risk of bleeding, ease of administration, and suitability for outpatient settings. LMWH offers predictable therapeutic outcomes and requires less frequent monitoring, making it a preferred choice among healthcare providers and patients alike.

The porcine-derived heparin segment held a CAGR of 7.3% in 2024 due to its consistent supply, clinical reliability, and reduced incidence of complications like heparin-induced thrombocytopenia (HIT). This variety of heparin is integral in the manufacturing of the most widely used LMWH types and remains the cornerstone of large-scale production.

United States Heparin Market generated USD 2.8 billion in 2024. The country's high incidence of cardiovascular diseases and chronic health conditions has led to strong demand for anticoagulant therapies. Regulatory support from the FDA, along with favorable reimbursement frameworks, continues to facilitate the widespread acceptance of both branded and generic heparin formulations. The growing use of prefilled syringes and autoinjectors in hospitals and home care environments is also contributing to the safe and convenient use of these medications.

Key companies leading the global heparin industry include Leo Pharma, Pfizer, Suanfarma, Shenzhen Hepalink Pharmaceuticals, Bioiberica, Amphastar, Sanofi, Dr. Reddy's Laboratories, Changzhou Qianhong Biopharma, Teva Pharmaceutical Industries, Fresenius Kabi, Aspen Pharmacare, Nanjing King-Friend Biochemical Pharmaceutical, Laboratorios Farmaceuticos ROVI, and Yantai Dongcheng Biochemicals. Leading players in the heparin market are leveraging a combination of strategic collaborations, vertical integration, and capacity expansion to strengthen their market position. Several companies are investing in R&D to develop next-generation anticoagulants with better efficacy and fewer side effects. Others are entering into partnerships and licensing agreements to broaden distribution channels and secure raw material supplies. Geographic expansion into high-growth emerging markets has also become a critical focus area.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Source

- 2.2.4 Route of administration

- 2.2.5 Application

- 2.2.6 Type

- 2.2.7 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global cardiovascular disease prevalence

- 3.2.1.2 Aging population and surgical procedures

- 3.2.1.3 Expansion of hospital infrastructure and homecare

- 3.2.1.4 Government and institutional health initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of branded LMWH and biosimilars

- 3.2.2.2 Supply chain disruptions and raw material dependency

- 3.2.3 Market opportunities

- 3.2.3.1 Development of synthetic and recombinant heparin

- 3.2.3.2 Emerging markets with rising healthcare investment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Future market trends

- 3.6 Technology landscape

- 3.6.1 Current technology

- 3.6.2 Emerging technologies

- 3.7 Patent landscape

- 3.8 Pricing analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Low molecular weight heparin

- 5.3 Unfractionated heparin

- 5.4 Ultra-low molecular weight heparin/synthetic heparin

Chapter 6 Market Estimates and Forecast, By Source, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Porcine

- 6.3 Bovine

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Intravenous

- 7.3 Subcutaneous

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Venous thromboembolism

- 8.3 Atrial fibrillation/flutter

- 8.4 Coronary artery disease

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Branded

- 9.3 Generics

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Clinics

- 10.4 Ambulatory surgical centers (ASCs)

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Amphastar

- 12.2 Aspen Pharmacare

- 12.3 Bioiberica

- 12.4 Changzhou Qianhong Biopharma

- 12.5 Dr. Reddy’s Laboratories

- 12.6 Fresenius Kabi

- 12.7 Laboratorios Farmaceuticos ROVI

- 12.8 Leo Pharma

- 12.9 Nanjing King-Friend Biochemical Pharmaceutical

- 12.10 Pfizer

- 12.11 Sanofi

- 12.12 Shenzhen Hepalink Pharmaceuticals

- 12.13 Suanfarma

- 12.14 Teva Pharmaceutical Industries

肝素市場:2026-2032年全球市場預測(依產品類型、原料、給藥途徑、應用、最終用戶及通路分類)

肝素市場:2026-2032年全球市場預測(依產品類型、原料、給藥途徑、應用、最終用戶及通路分類) 2026-2034年全球肝素市場規模、佔有率、趨勢和成長分析報告低分子量肝素原料藥市場:依產品、生產流程、應用、最終用戶和通路分類,全球預測(2026-2032年)

2026-2034年全球肝素市場規模、佔有率、趨勢和成長分析報告低分子量肝素原料藥市場:依產品、生產流程、應用、最終用戶和通路分類,全球預測(2026-2032年) 低分子量肝素市場分析及預測(至2035年):依類型、產品類型、應用、最終用戶、給藥途徑、劑型、技術、成分及功能分類

低分子量肝素市場分析及預測(至2035年):依類型、產品類型、應用、最終用戶、給藥途徑、劑型、技術、成分及功能分類 低分子量肝素市場:依藥物、包裝、應用、最終用戶和地區分類全球未分級肝素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)肝素市場依產品類型、劑型及地區分類肝素市場-2026-2031年預測

低分子量肝素市場:依藥物、包裝、應用、最終用戶和地區分類全球未分級肝素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)肝素市場依產品類型、劑型及地區分類肝素市場-2026-2031年預測 日本肝素市場報告(按產品、來源、給藥途徑、應用、最終用戶、配銷通路和地區分類,2026-2034年)

日本肝素市場報告(按產品、來源、給藥途徑、應用、最終用戶、配銷通路和地區分類,2026-2034年) 肝素市場規模、佔有率和成長分析(按產品類型、給藥途徑、成分、供應、治療方法領域、規格、類型、包裝和地區分類)-2026-2033年產業預測

肝素市場規模、佔有率和成長分析(按產品類型、給藥途徑、成分、供應、治療方法領域、規格、類型、包裝和地區分類)-2026-2033年產業預測