|

市場調查報告書

商品編碼

1833453

煞車摩擦產品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Brake Friction Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

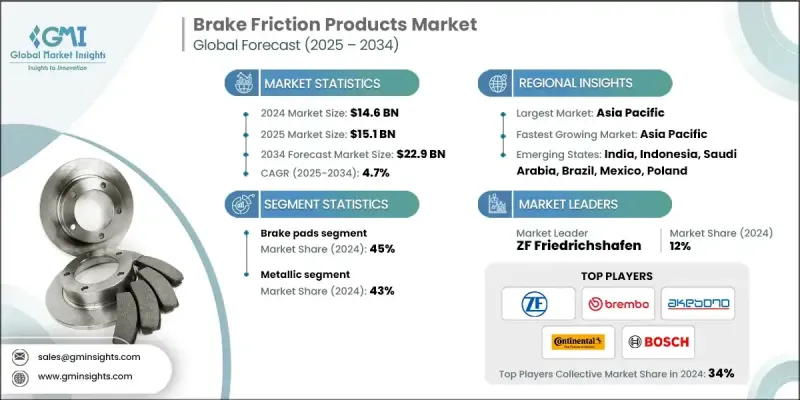

2024 年全球煞車摩擦產品市場價值為 146 億美元,預計到 2034 年將以 4.7% 的複合年成長率成長至 229 億美元。

全球汽車產量的穩定成長是煞車摩擦產品市場的主要驅動力。隨著經濟發展和都市化進程,越來越多的消費者購買乘用車、商用卡車和二輪車來滿足其出行需求。這些車輛都高度依賴可靠的煞車系統來確保安全,因此,煞車片、襯片和蹄片等煞車摩擦部件成為每輛新車的必備部件。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 146億美元 |

| 預測值 | 229億美元 |

| 複合年成長率 | 4.7% |

煞車片需求不斷成長

2024年,煞車片市場收入可觀,這得益於車輛安全性和性能的提升,使其成為乘用車、商用車和二輪車不可或缺的部件。為了滿足日益成長的消費者期望,製造商正致力於提升煞車片的耐用性和降噪能力。此外,陶瓷和半金屬化合物等先進材料的日益普及也推動了該領域的成長。隨著創新的不斷推進和安全法規的嚴格實施,在汽車產量和更換需求不斷成長的推動下,煞車片市場規模持續擴張。

金屬材料的採用日益增多

金屬摩擦材料憑藉其卓越的耐熱性和耐用性,在2024年佔據了相當大的佔有率。該領域尤其受到商用車和高性能汽車的青睞,這些汽車需要在嚴苛條件下實現強勁的煞車性能。然而,該行業也面臨著許多挑戰,例如環境法規要求降低金屬含量,以及開發更環保的替代品的需求。各公司正在加大研發投入,以創新低金屬或混合摩擦材料,從而兼顧性能與永續性,確保該領域保持競爭力並符合不斷發展的標準。

亞太地區將成為推動力地區

受中國、印度和日本等國汽車產量不斷成長和城鎮化進程加快的推動,亞太地區煞車摩擦產品市場將在2034年之前實現快速成長。消費者對車輛安全的意識不斷增強,以及售後市場的蓬勃發展,將進一步推動市場擴張。主要參與者正在透過建立本地製造部門、與原始設備製造商建立戰略合作夥伴關係,以及專注於根據地區偏好和監管要求客製化經濟高效的高品質摩擦材料,鞏固其在該地區的地位。

煞車摩擦產品市場的主要參與者有德爾福科技、輝門、布雷博、曙光煞車工業株式會社、愛德克斯株式會社、羅伯特博世、大陸集團、採埃孚、日清紡控股、愛信精機株式會社。

煞車摩擦產品市場的公司正在部署創新、策略合作夥伴關係和區域擴張等多種策略,以鞏固其市場地位。在研發方面的大量投入使製造商能夠開發出符合嚴格環境和安全法規的先進摩擦材料,同時提升產品性能。與原始設備製造商 (OEM) 的合作有助於確保長期供應契約,從而確保穩定的收入來源。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 嚴格的安全規定

- 新興市場汽車產量成長

- 轉向無銅和環保材料

- 亞太地區二輪車和車隊擁有量不斷成長

- 產業陷阱與挑戰

- 原物料價格波動

- 來自低成本非正規參與者的競爭

- 市場機會

- 車輛電氣化

- 售後市場數位化與電子商務

- 已開發市場的高階化趨勢

- 策略合作與併購

- 成長動力

- 成長潛力分析

- 監管格局

- 全球的

- ISO 26867:2009 測試標準實施

- 環境法規

- 效能測試和驗證協議

- 品質保證和製造標準

- 區域

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 全球的

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 電動車革命影響評估

- 線控制動系統的開發與應用

- 自動駕駛汽車煞車要求

- 製造技術創新

- 新興技術

- 智慧材料和自適應性能

- 人工智慧與預測性維護整合

- 永續材料創新與發展

- 當前的技術趨勢

- 價格趨勢

- 按地區

- 按產品

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本分解分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

- 煞車粉塵排放分析及環境影響

- 環境法規合規框架

- 企業永續性與 ESG 績效

- 制動性能分析和測試智慧

- 真實世界停車距離資料庫

- 熱性能和衰減分析

- 摩擦係數一致性分析

- 噪音、振動和聲振粗糙度 (NVH) 情報

- 煞車噪音分析與緩解

- 振動和抖動性能

- 嚴酷性和舒適度指標

- 健康與環境影響情報

- 煞車粉塵排放量化

- 職業健康與安全分析

- 環境生命週期評估

第3章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 製造和供應鏈分析

- 全球製造足跡和產能分析

- 原物料供應鏈與風險評估

- 製造成本分析與最佳化

- 供應鏈彈性與風險管理

- 品質控制和性能驗證框架

- 統計製程管制(SPC)分析

- 效能測試和驗證協議

- 故障模式與影響分析(FMEA)

第4章:市場估計與預測:依產品,2021 - 2034

- 主要趨勢

- 煞車片

- 煞車蹄

- 煞車片

- 煞車鼓

- 煞車碟盤/煞車盤

- 其他

第5章:市場估計與預測:依資料,2021 - 2034 年

- 主要趨勢

- 金屬

- 陶瓷製品

- 合成的

- 其他

第6章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- 搭乘用車

- 轎車

- SUV

- 掀背車

- 商用車

- 輕型商用車(LCV)

- 重型商用車(HCV)

- 中型商用車(MCV)

- 二輪車

- 非公路車輛

第7章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- 原始設備製造商(OEM)

- 售後市場

第8章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Global companies

- Aisin Seiki Co.

- Akebono Brake Industry Co.

- Brembo

- Continental

- Federal-Mogul

- Miba Friction Group

- Robert Bosch

- Tenneco

- TMD Friction Holdings

- ZF Friedrichshafen

- Regional companies

- Advics Co.

- ATE

- Delphi Technologies

- EBC Brakes

- Ferodo

- Jurid

- MAT Holdings

- Nisshinbo Holdings

- NRS Brakes

- Sangsin Brake

- Wagner Brake

- 新興企業

- AI-Powered Brake Analytics Startups

- Drivezy

- Brake Parts

- Fras-le

- Galfer Bike

- Hardron Friction Material

- SGL Carbon SE - Brake Disc Division

- Xinyi Brake Pad Co.

The Global Brake Friction Products Market was valued at USD 14.6 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 22.9 billion by 2034.

The steady rise in global vehicle production is a primary driver in the brake friction products market. As economies develop and urbanize, more consumers are purchasing passenger cars, commercial trucks, and two-wheelers to meet their transportation needs. Each of these vehicles depends heavily on reliable braking systems to ensure safety, making brake friction components like pads, linings, and shoes essential parts in every new vehicle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.6 Billion |

| Forecast Value | $22.9 Billion |

| CAGR | 4.7% |

Increasing Demand for Brake Pads

The brake pads segment generated substantial revenues in 2024, driven by vehicle safety and performance that makes them indispensable across passenger cars, commercial vehicles, and two-wheelers. Manufacturers are focusing on enhancing the durability and noise reduction capabilities of brake pads to meet rising consumer expectations. Furthermore, the increasing adoption of advanced materials such as ceramic and semi-metallic compounds is fueling growth within this segment. With ongoing innovations and stringent safety regulations, the brake pads segment continues to expand, driven by rising vehicle production and replacement demand.

Rising Adoption of Metallic Material

The metallic segment held a significant share in 2024 owing to its superior heat resistance and durability. This segment is particularly favored in commercial vehicles and high-performance automobiles that require robust braking under demanding conditions. However, industry faces challenges such as environmental regulations pushing for reduced metal content and the need to develop eco-friendlier alternatives. Companies are investing in R&D to innovate low-metallic or hybrid friction materials that balance performance with sustainability, ensuring this segment remains competitive and compliant with evolving standards.

Asia Pacific to Emerge as a Propelling Region

Asia Pacific brake friction products market will witness rapid growth through 2034, driven by escalating vehicle production and expanding urbanization across countries like China, India, and Japan. Increasing consumer awareness regarding vehicle safety and the growing aftermarket segment are further propelling market expansion. Key players are strengthening their foothold in this region by establishing local manufacturing units, forming strategic partnerships with OEMs, and focusing on cost-effective, high-quality friction materials tailored to regional preferences and regulatory requirements.

Major players in the brake friction products market are Delphi Technologies, Federal-Mogul, Brembo, Akebono Brake Industry Co., Advics Co., Robert Bosch, Continental, ZF Friedrichshafen, Nisshinbo Holdings, Aisin Seiki Co.

Companies operating in the brake friction products market are deploying a combination of innovation, strategic partnerships, and regional expansion to bolster their market position. Heavy investments in R&D allow manufacturers to develop advanced friction materials that meet stringent environmental and safety regulations while enhancing product performance. Collaborations with original equipment manufacturers (OEMs) help secure long-term supply contracts, ensuring steady revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Industry Insights

- 2.1 Industry ecosystem analysis

- 2.1.1 Supplier landscape

- 2.1.2 Profit margin

- 2.1.3 Cost structure

- 2.1.4 Value addition at each stage

- 2.1.5 Factor affecting the value chain

- 2.1.6 Disruptions

- 2.2 Industry impact forces

- 2.2.1 Growth drivers

- 2.2.1.1 Stringent safety regulations

- 2.2.1.2 Vehicle production growth in emerging markets

- 2.2.1.3 Shift toward copper-free & eco-friendly materials

- 2.2.1.4 Rising two-wheeler and fleet ownership in APAC

- 2.2.2 Industry pitfalls and challenges

- 2.2.2.1 Raw material price volatility

- 2.2.2.2 Competition from low-cost unorganized players

- 2.2.3 Market opportunities

- 2.2.3.1 Electrification of vehicles

- 2.2.3.2 Aftermarket digitization & e-commerce

- 2.2.3.3 Premiumization trend in developed markets

- 2.2.3.4 Strategic collaborations & M&A

- 2.2.1 Growth drivers

- 2.3 Growth potential analysis

- 2.4 Regulatory landscape

- 2.4.1 Global

- 2.4.1.1 ISO 26867:2009 Testing Standards Implementation

- 2.4.1.2 Environmental Regulations

- 2.4.1.3 Performance Testing and Validation Protocols

- 2.4.1.4 Quality Assurance and Manufacturing Standards

- 2.4.2 Regional

- 2.4.2.1 North America

- 2.4.2.2 Europe

- 2.4.2.3 Asia Pacific

- 2.4.2.4 Latin America

- 2.4.2.5 Middle East & Africa

- 2.4.1 Global

- 2.5 Porter’s analysis

- 2.6 PESTEL analysis

- 2.7 Technology and innovation landscape

- 2.7.1 Current technological trends

- 2.7.1.1 Electric vehicle revolution impact assessment

- 2.7.1.2 Brake-by-wire systems development and adoption

- 2.7.1.3 Autonomous vehicle braking requirements

- 2.7.1.4 Manufacturing technology innovation

- 2.7.2 Emerging technologies

- 2.7.2.1 Smart materials and adaptive performance

- 2.7.2.2 AI and predictive maintenance integration

- 2.7.2.3 Sustainable material innovation and development

- 2.7.1 Current technological trends

- 2.8 Price trends

- 2.8.1 By region

- 2.8.2 By product

- 2.9 Production statistics

- 2.9.1 Production hubs

- 2.9.2 Consumption hubs

- 2.9.3 Export and import

- 2.10 Cost breakdown analysis

- 2.11 Patent analysis

- 2.12 Sustainability and environmental aspects

- 2.12.1 Sustainable practices

- 2.12.2 Waste reduction strategies

- 2.12.3 Energy efficiency in production

- 2.12.4 Eco-friendly initiatives

- 2.12.5 Carbon footprint considerations

- 2.12.6 Brake dust emission analysis and environmental impact

- 2.12.7 Environmental regulation compliance framework

- 2.12.8 Corporate sustainability and ESG performance

- 2.13 Brake performance analytics and testing intelligence

- 2.13.1 Real-world stopping distance database

- 2.13.2 Thermal performance and fade analysis

- 2.13.3 Friction coefficient consistency analytics

- 2.14 Noise, vibration, and harshness (NVH) intelligence

- 2.14.1 Brake noise analysis and mitigation

- 2.14.2 Vibration and judder performance

- 2.14.3 Harshness and comfort metrics

- 2.15 Health and environmental impact intelligence

- 2.15.1 Brake dust emission quantification

- 2.15.2 Occupational health and safety analysis

- 2.15.3 Environmental lifecycle assessment

Chapter 3 Competitive Landscape, 2024

- 3.1 Introduction

- 3.2 Company market share analysis

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 LATAM

- 3.2.5 MEA

- 3.3 Competitive analysis of major market players

- 3.4 Competitive positioning matrix

- 3.5 Strategic outlook matrix

- 3.6 Key developments

- 3.6.1 Mergers & acquisitions

- 3.6.2 Partnerships & collaborations

- 3.6.3 New product launches

- 3.6.4 Expansion plans and funding

- 3.7 Manufacturing and supply chain analysis

- 3.7.1 Global manufacturing footprint and capacity analysis

- 3.7.2 Raw material supply chain and risk assessment

- 3.7.3 Manufacturing cost analysis and optimization

- 3.7.4 Supply chain resilience and risk management

- 3.8 Quality control and performance validation framework

- 3.8.1 Statistical process control (SPC) analytics

- 3.8.2 Performance testing and validation protocols

- 3.8.3 Failure mode and effects analysis (FMEA)

Chapter 4 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 4.1 Key trends

- 4.2 Brake pads

- 4.3 Brake shoes

- 4.4 Brake linings

- 4.5 Brake drums

- 4.6 Brake rotors/discs

- 4.7 Others

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Metallic

- 5.3 Ceramic

- 5.4 Composite

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUVs

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Heavy commercial vehicles (HCVs)

- 6.3.3 Medium commercial vehicles (MCVs)

- 6.4 Two-wheelers

- 6.5 Off-highway vehicles

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Original equipment manufacturer (OEM)

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global companies

- 9.1.1 Aisin Seiki Co.

- 9.1.2 Akebono Brake Industry Co.

- 9.1.3 Brembo

- 9.1.4 Continental

- 9.1.5 Federal-Mogul

- 9.1.6 Miba Friction Group

- 9.1.7 Robert Bosch

- 9.1.8 Tenneco

- 9.1.9 TMD Friction Holdings

- 9.1.10 ZF Friedrichshafen

- 9.2 Regional companies

- 9.2.1 Advics Co.

- 9.2.2 ATE

- 9.2.3 Delphi Technologies

- 9.2.4 EBC Brakes

- 9.2.5 Ferodo

- 9.2.6 Jurid

- 9.2.7 MAT Holdings

- 9.2.8 Nisshinbo Holdings

- 9.2.9 NRS Brakes

- 9.2.10 Sangsin Brake

- 9.2.11 Wagner Brake

- 9.3 Emerging players

- 9.3.1 AI-Powered Brake Analytics Startups

- 9.3.2 Drivezy

- 9.3.3 Brake Parts

- 9.3.4 Fras-le

- 9.3.5 Galfer Bike

- 9.3.6 Hardron Friction Material

- 9.3.7 SGL Carbon SE - Brake Disc Division

- 9.3.8 Xinyi Brake Pad Co.

煞車摩擦材料市場-2026-2032年全球市場預測

煞車摩擦材料市場-2026-2032年全球市場預測 煞車摩擦材料市場分析及至2035年預測:類型、產品、技術、組件、應用、材質、最終用戶、功能、安裝類型

煞車摩擦材料市場分析及至2035年預測:類型、產品、技術、組件、應用、材質、最終用戶、功能、安裝類型 2026年全球煞車摩擦產品市場報告煞車塊市場:全球市場按材料、應用、分銷管道和銷售管道分類的預測,2026-2032年

2026年全球煞車摩擦產品市場報告煞車塊市場:全球市場按材料、應用、分銷管道和銷售管道分類的預測,2026-2032年 汽車煞車摩擦材料市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、煞車碟盤材料、車輛類型、類型、地區及競爭格局分類,2021-2031年)煞車摩擦材料市場-全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、襯片類型、材料類型、地區和競爭格局分類,2021-2031年

汽車煞車摩擦材料市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、煞車碟盤材料、車輛類型、類型、地區及競爭格局分類,2021-2031年)煞車摩擦材料市場-全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、襯片類型、材料類型、地區和競爭格局分類,2021-2031年 煞車摩擦材料市場規模、佔有率及成長分析(依產品類型、材質、車輛類型、銷售管道及地區分類)-2026-2033年產業預測

煞車摩擦材料市場規模、佔有率及成長分析(依產品類型、材質、車輛類型、銷售管道及地區分類)-2026-2033年產業預測 煞車摩擦產品市場,按產品類型、按車輛類型、按碟式類型、按配銷通路、按國家/地區 - 行業分析、市場規模、市場佔有率及預測(2025 年至 2032 年)

煞車摩擦產品市場,按產品類型、按車輛類型、按碟式類型、按配銷通路、按國家/地區 - 行業分析、市場規模、市場佔有率及預測(2025 年至 2032 年) 全球煞車摩擦產品市場(OEM、售後市場)按類型、碟式煞車類型、襯套類型、車輛類型和地區分類 - 預測至 2032 年汽車自動變速箱濕式摩擦片市場按產品類型、材料類型、車輛類型和銷售管道分類 - 2025 年至 2030 年全球預測

全球煞車摩擦產品市場(OEM、售後市場)按類型、碟式煞車類型、襯套類型、車輛類型和地區分類 - 預測至 2032 年汽車自動變速箱濕式摩擦片市場按產品類型、材料類型、車輛類型和銷售管道分類 - 2025 年至 2030 年全球預測