|

市場調查報告書

商品編碼

1833441

非小細胞肺癌市場機會、成長動力、產業趨勢分析及2025-2034年預測Non-Small Cell Lung Cancer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

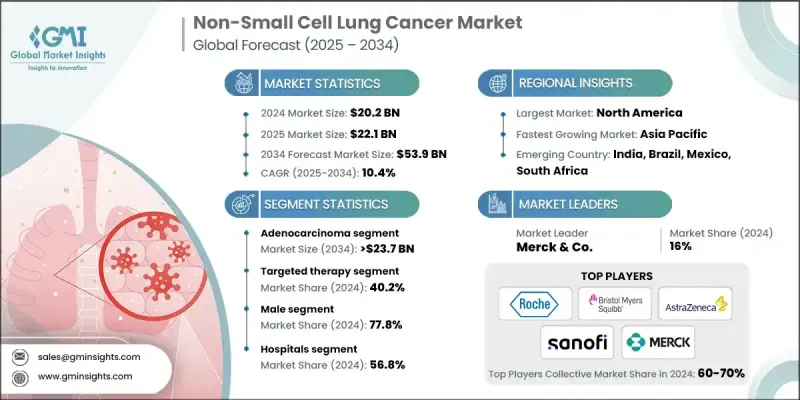

2024 年全球非小細胞肺癌市場價值為 202 億美元,預計將以 10.4% 的複合年成長率成長,到 2034 年達到 539 億美元。

針對特定基因突變(如 EGFR、ALK、ROS1 和 KRAS)的療法的發展已經改變了治療途徑、擴展了個人化醫療並顯著改善了特定患者群體的治療效果。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 202億美元 |

| 預測值 | 539億美元 |

| 複合年成長率 | 10.4% |

腺癌盛行率上升

腺癌在2024年佔據了相當大的佔有率,這得益於其高發病率,尤其是在非吸煙者和年輕患者中。腺癌是非小細胞肺癌(NSCLC)最常見的組織學亞型,通常與可操作的基因突變相關,使其成為分子標靶治療的主要關注點。

標靶治療的應用日益廣泛

標靶治療領域在2024年佔據了相當大的佔有率,其優勢在於提供個人化治療方案,在提高生存率的同時最大限度地降低全身毒性。由於多種針對EGFR、ALK、BRAF、MET和KRAS等特定致癌促進因素的藥物獲得批准,該領域發展勢頭強勁。標靶藥物通常被推薦為符合條件患者的第一線治療方案,與傳統化療相比,其無惡化存活期更長。

男性產業將獲得發展

由於男性吸菸率和職業性肺癌致癌物暴露率歷來較高,男性市場在2024年佔據了相當大的佔有率。儘管基於性別的治療方案並無顯著差異,但男性患者發病率較高,導致診斷、治療啟動和後續護理方面的需求不成比例。

北美將成為推動力地區

2025-2034年期間,北美非小細胞肺癌市場將以可觀的複合年成長率成長,這得益於強大的醫療基礎設施、廣泛的生物標記檢測以及下一代療法的早期應用。該地區也受惠於積極參與全球臨床試驗以及快速核准的監管途徑,這些途徑能夠更快地將新型療法推向市場。隨著精準腫瘤學投資的不斷增加以及政府的支持性舉措,北美預計將在非小細胞肺癌領域保持主導地位。

非小細胞肺癌產業的一些知名企業包括 Xcovery、默克公司、楊森生物技術公司、賽諾菲、艾伯維、諾華、安斯泰來製藥、輝瑞、禮來、武田、羅氏公司、百時美施貴寶公司、阿斯特捷利康、太陽製藥和 Merus。

為了鞏固在非小細胞肺癌市場的地位,各大公司正在實施一系列策略,包括擴大精準腫瘤學產品組合,並透過監管快速通道加快上市時間。重點是開發下一代抑制劑,以克服現有療法的抗藥性,尤其是在標靶治療領域。與診斷公司的合作也至關重要,因為它們可以透過伴隨診斷簡化患者識別。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 非小細胞肺癌盛行率不斷上升

- 免疫療法和標靶治療的突破

- 診斷技術的進步

- 個人化醫療的普及率不斷提高

- 產業陷阱與挑戰

- 先進療法成本高昂

- 監管和診斷基礎設施差距

- 市場機會

- 新興市場需求不斷成長

- 轉向個人化和聯合治療

- 成長動力

- 成長潛力分析

- 監管格局

- 未來市場趨勢

- 管道分析

- 技術和創新格局

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

第5章:市場估計與預測:按類型,2021 - 2034

- 主要趨勢

- 腺癌

- 鱗狀細胞癌

- 大細胞癌

- 其他類型

第6章:市場估計與預測:依治療方式,2021 - 2034

- 主要趨勢

- 化療

- 免疫療法

- 標靶治療

- 其他治療類型

第7章:市場估計與預測:依性別,2021 - 2034 年

- 主要趨勢

- 男性

- 女性

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 專科診所

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AbbVie

- Astellas Pharma

- AstraZeneca

- Bristol-Myers Squibb Company

- Eli Lilly

- F. Hoffmann La Roche

- Janssen Biotech

- Merck & Co.

- Merus

- Novartis

- Pfizer

- Sanofi

- Sun Pharmaceutical

- Takeda

- Xcovery

The Global Non-Small Cell Lung Cancer Market was valued at USD 20.2 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 53.9 billion by 2034.

The development of therapies targeting specific genetic mutations (like EGFR, ALK, ROS1, and KRAS) has transformed treatment pathways, expanded personalized medicine and significantly improved outcomes in select patient groups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.2 Billion |

| Forecast Value | $53.9 Billion |

| CAGR | 10.4% |

Rising Prevalence of Adenocarcinoma

The adenocarcinoma segment held a significant share in 2024, driven by its high prevalence, particularly among non-smokers and younger patients. As the most common histological subtype of NSCLC, adenocarcinoma is often associated with actionable genetic mutations, making it a prime focus for molecularly targeted therapies.

Increasing Adoption of Targeted Therapy

The targeted therapy segment held a sizeable share in 2024, backed by offering a personalized approach that improves survival while minimizing systemic toxicity. This segment has gained strong momentum due to the approval of multiple agents addressing specific oncogenic drivers like EGFR, ALK, BRAF, MET, and KRAS mutations. Targeted drugs are often preferred as first-line treatments for eligible patients, resulting in longer progression-free survival compared to traditional chemotherapy.

Male Sector to Gain Traction

The male segment generated a substantial share in 2024, owing to historically higher rates of smoking and occupational exposure to lung carcinogens among men. Although gender-based treatment protocols do not significantly differ, the higher incidence among male patients drives disproportionate demand in terms of diagnostics, therapy initiation, and follow-up care.

North America to Emerge as a Propelling Region

North America non-small cell lung cancer market will grow at a decent CAGR during 2025-2034, fueled by robust healthcare infrastructure, widespread biomarker testing, and early adoption of next-generation therapies. The region also benefits from active participation in global clinical trials and fast-track regulatory pathways that bring novel treatments to market faster. With rising investment in precision oncology and supportive government initiatives, North America is expected to maintain its dominant position in the NSCLC landscape.

Some prominent players operating in the non-small cell lung cancer industry include Xcovery, Merck & Co., Janssen Biotech, Sanofi, AbbVie, Novartis, Astellas Pharma, Pfizer, Eli Lilly, Takeda, F. Hoffmann La Roche, Bristol-Myers Squibb Company, AstraZeneca, Sun Pharmaceutical, and Merus.

To strengthen their presence in the non-small cell lung cancer market, companies are implementing a range of strategies, including expanding their precision oncology portfolios and accelerating time-to-market through regulatory fast-tracks. A major focus lies in developing next-generation inhibitors to overcome resistance to existing therapies, particularly in the targeted therapy segment. Collaborations with diagnostic firms are also key, as they enable streamlined patient identification through companion diagnostics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Treatment

- 2.2.4 Gender

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of non-small cell lung cancer

- 3.2.1.2 Breakthroughs in immunotherapy and targeted treatments

- 3.2.1.3 Advancements in diagnostic technologies

- 3.2.1.4 Growing adoption of personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced therapies

- 3.2.2.2 Regulatory and diagnostic infrastructure gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand in emerging markets

- 3.2.3.2 Shift toward personalized and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Technology and innovation landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Adenocarcinoma

- 5.3 Squamous cell carcinoma

- 5.4 Large cell carcinoma

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Other treatment types

Chapter 7 Market Estimates and Forecast, By Gender, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Male

- 7.3 Female

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Astellas Pharma

- 10.3 AstraZeneca

- 10.4 Bristol-Myers Squibb Company

- 10.5 Eli Lilly

- 10.6 F. Hoffmann La Roche

- 10.7 Janssen Biotech

- 10.8 Merck & Co.

- 10.9 Merus

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sun Pharmaceutical

- 10.14 Takeda

- 10.15 Xcovery

非小細胞肺癌治療市場:依治療方法、治療階段、生物標記表達及通路分類-2026年至2032年全球市場預測

非小細胞肺癌治療市場:依治療方法、治療階段、生物標記表達及通路分類-2026年至2032年全球市場預測 非小細胞肺癌 (NSCLC) 市場分析及預測(至 2035 年):按類型、產品類型、技術、應用、最終用戶、疾病分期、設備、解決方案和流程分類

非小細胞肺癌 (NSCLC) 市場分析及預測(至 2035 年):按類型、產品類型、技術、應用、最終用戶、疾病分期、設備、解決方案和流程分類 非小細胞肺癌市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、療法、藥物類別、最終用戶、地區和競爭格局分類,2021-2031年)

非小細胞肺癌市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、療法、藥物類別、最終用戶、地區和競爭格局分類,2021-2031年) 非小細胞肺癌(NSCLC)的全球市場,規模,佔有率,趨勢,產業分析報告:類別,不同治療,各流通管道,各地區 - 市場預測,2025年~2034年

非小細胞肺癌(NSCLC)的全球市場,規模,佔有率,趨勢,產業分析報告:類別,不同治療,各流通管道,各地區 - 市場預測,2025年~2034年 全球B型進行性纖維肉瘤轉移性非小細胞肺癌市場(依國家及地區)分析與預測(2025-2035)

全球B型進行性纖維肉瘤轉移性非小細胞肺癌市場(依國家及地區)分析與預測(2025-2035) 非小細胞肺癌治療市場,按療法、按配銷通路、按癌症類型、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

非小細胞肺癌治療市場,按療法、按配銷通路、按癌症類型、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 非小細胞肺癌治療市場規模、佔有率、趨勢分析報告:按類型、治療方法、分銷管道、地區和細分市場預測,2025 年至 2030 年

非小細胞肺癌治療市場規模、佔有率、趨勢分析報告:按類型、治療方法、分銷管道、地區和細分市場預測,2025 年至 2030 年 非小細胞肺癌市場按類型、治療、最終用戶和地區分類

非小細胞肺癌市場按類型、治療、最終用戶和地區分類 非小細胞肺癌市場規模、佔有率、成長分析、按類型、按治療方法、按最終用途行業、按地區 - 行業預測,2025-2032 年

非小細胞肺癌市場規模、佔有率、成長分析、按類型、按治療方法、按最終用途行業、按地區 - 行業預測,2025-2032 年