|

市場調查報告書

商品編碼

1833413

戰鬥無人機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Combat Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

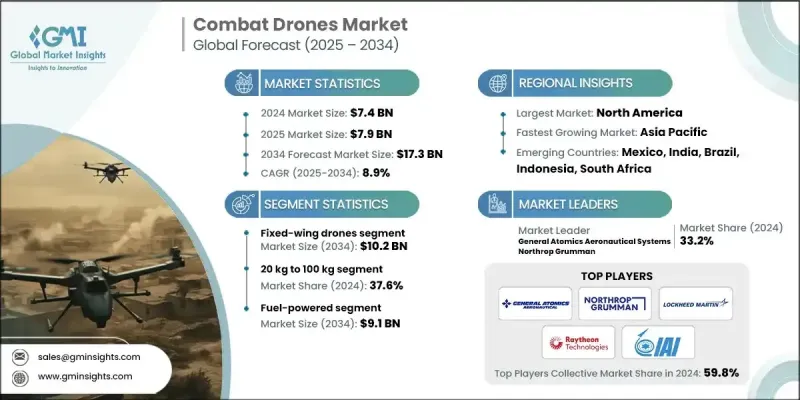

2024 年全球戰鬥無人機市場價值為 74 億美元,預計到 2034 年將以 8.9% 的複合年成長率成長至 173 億美元。

這一激增是由多種因素推動的,包括軍隊的現代化建設、國防開支的增加以及人工智慧 (AI)、感測器和自主技術的快速發展。隨著新興經濟體優先考慮國防現代化,大量資源被分配用於無人作戰航空系統的研發。這些努力使各國能夠保持與主要軍事強國的競爭力,同時也受惠於先進的無人機技術。配備隱形和低可探測技術的作戰無人機正日益受到青睞,使軍隊能夠在高威脅環境中作戰,同時躲避複雜防空系統的探測。此外,由於協同無人機可以更有效地滲透和摧毀敵方防禦,因此蜂群無人機戰術的使用也越來越流行。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 74億美元 |

| 預測值 | 173億美元 |

| 複合年成長率 | 8.9% |

預計到2034年,固定翼無人機市場規模將達102億美元。固定翼無人機尤其受到青睞,因為它們擁有更長的續航里程、更高的有效載荷能力,並且更適合執行遠程打擊和監視任務。預計該領域在北美和亞洲等地區的應用將會成長,因為這些地區已經將固定翼無人機用於邊境巡邏和大規模行動。為了保持競爭力,製造商必須專注於增強隱身性能,並整合先進的情報、監視和偵察 (ISR) 負載。

2024年,20公斤至100公斤重量級無人機的市佔率為37.6%。由於便攜性和價格實惠,該重量級無人機擴大用於偵察和精確打擊等戰術任務。對於那些國防預算有限、尋求經濟高效的軍隊現代化解決方案的國家來說,這些系統極具吸引力。製造商需要專注於生產緊湊型、人工智慧驅動、高效且價格合理的無人機,以滿足這些發展中市場的需求。

2024年,美國作戰無人機市場規模達28億美元,這得益於雄厚的國防預算、無人機的廣泛應用以及下一代無人作戰飛機(UCAV)研發的持續創新。美國在無人機集群技術和人工智慧驅動的自主性方面也保持領先地位。進入該市場的公司必須與美國國防現代化進程保持一致,專注於能夠融入當前和未來軍事戰略的可擴展無人機系統。

戰鬥無人機市場的主要參與者包括諾斯羅普·格魯曼公司、通用原子航空系統公司、以色列航太公司 (IAI)、雷神技術公司、埃爾比特系統公司、萊昂納多公司、波音公司、AeroVironment公司和空中巴士公司等公司。這些公司在開發尖端無人機技術方面處於領先地位,並致力於滿足軍事行動中日益成長的無人機系統需求。他們的市場策略專注於將創新的人工智慧、自主能力和隱身功能融入其產品中。各公司也大力投資研發,以保持領先於不斷變化的國防需求,同時與政府機構建立戰略合作夥伴關係,以配合國防優先事項。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 軍隊現代化和國防開支的增加

- 人工智慧、感測器和自主技術的快速進步

- 安全威脅情勢與地緣政治不穩定不斷升級

- 監理轉變與出口自由化

- 策略聯盟和供應鏈擴張

- 產業陷阱與挑戰

- 開發和採購成本高

- 嚴格的監管和出口管制限制

- 市場機會

- 人工智慧與機器學習的融合

- 擴展無人機群能力

- 混合和隱形技術的採用日益增多

- 向新興國防市場出口的潛力

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按無人機類型,2021 - 2034 年

- 主要趨勢

- 固定翼無人機

- 旋翼無人機

- 單旋翼

- 多旋翼

- 混合無人機

第6章:市場估計與預測:按有效載荷能力,2021 - 2034 年

- 主要趨勢

- 最多 2 公斤

- 2公斤至19公斤

- 20公斤至100公斤

- 100公斤以上

第7章:市場估計與預測:按電源,2021 - 2034

- 主要趨勢

- 電池供電

- 油電混合

- 燃料驅動

第8章:市場估計與預測:按技術分類,2021 - 2034 年

- 主要趨勢

- 遙控無人機

- 半自動無人機

- 全自動無人機

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 致命的作戰無人機

- 隱形無人機

- 巡飛彈藥無人機

- 目標無人機

- 其他

第 10 章:市場估計與預測:按發射模式,2021 年至 2034 年

- 主要趨勢

- 垂直起降(VTOL)

- 自動起飛和降落(ATOL)

- 彈射無人機

- 手射無人機

第 11 章:市場估計與預測:按最終用途應用,2021 - 2034 年

- 主要趨勢

- 軍事行動

- 戰略監視

- 戰術戰鬥

- 偵察任務

- 訓練與模擬

- 戰鬥訓練

- 打靶

- 邊境和海上安全

- 海岸監視

- 邊境巡邏

- 反恐與執法

- 都市監控

- 戰術干預

第 12 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 全球關鍵參與者

- Northrop Grumman Corporation

- Raytheon Technologies Corporation (RTX)

- Lockheed Martin Corporation

- 區域關鍵參與者

- 北美洲

- General Atomics Aeronautical Systems, Inc.

- AeroVironment, Inc.

- The Boeing Company (Insitu, Inc.)

- 歐洲

- Airbus SE

- Leonardo SpA

- BAE Systems plc

- 亞太地區

- Israel Aerospace Industries Ltd. (IAI)

- Turkish Aerospace Industries, Inc. (TAI)

- Safran SA

- 北美洲

- 利基市場參與者/顛覆者

- Elbit Systems Ltd.

- QinetiQ Group plc

- Kratos Defense & Security Solutions, Inc.

- Anduril Industries, Inc.

- Textron Inc.

- Thales Group

- Griffon Aerospace

- Sistemas de Control Remoto (SCR)

The Global Combat Drones Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 17.3 billion by 2034.

This surge is driven by several factors, including modernization efforts in military forces, increased defense spending, and rapid advancements in artificial intelligence (AI), sensors, and autonomous technologies. As emerging economies prioritize defense modernization, significant resources are being allocated for the development of unmanned combat aerial systems. These efforts allow nations to stay competitive with major military powers while benefiting from advanced drone technologies. Combat drones equipped with stealth and low-observable technologies are gaining traction, enabling military forces to operate in high-threat environments while evading detection by sophisticated air defense systems. Additionally, the use of swarm drone tactics is becoming increasingly popular, as coordinated UAVs can infiltrate and neutralize enemy defenses more effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $17.3 Billion |

| CAGR | 8.9% |

The fixed-wing drone segment is expected to reach USD 10.2 billion by 2034. Fixed-wing drones are particularly favored due to their longer operational range, enhanced payload capacity, and suitability for long-range strike and surveillance missions. The segment's adoption is expected to rise in regions like North America and Asia, where they are already used for border patrols and mass operations. Manufacturers must focus on enhancing stealth features and incorporating advanced intelligence, surveillance, and reconnaissance (ISR) payloads to remain competitive.

The 20 kg to 100 kg weight class segment held a 37.6% share in 2024. Drones within this weight range are increasingly used for tactical missions such as reconnaissance and precision strikes due to their portability and affordability. These systems are attractive to nations with limited defense budgets seeking cost-effective solutions for modernizing their armed forces. Manufacturers will need to focus on producing compact, AI-powered drones that are both effective and affordable for these developing markets.

United States Combat Drones Market generated USD 2.8 billion in 2024, driven by a robust defense budget, extensive use of drones, and ongoing innovation in the development of next-generation unmanned combat aerial vehicles (UCAVs). The U.S. also remains a leader in swarm technology and AI-driven autonomy in drones. Companies entering the market must align with U.S. defense modernization efforts, focusing on scalable drone systems that can integrate into both current and future military strategies.

Key players in the combat drones market include companies like Northrop Grumman, General Atomics Aeronautical Systems, Israel Aerospace Industries (IAI), Raytheon Technologies, Elbit Systems, Leonardo, Boeing, AeroVironment, and Airbus. These companies are at the forefront of developing cutting-edge drone technologies and meeting the growing demand for unmanned aerial systems in military operations. Their market strategies focus on incorporating innovative AI, autonomous capabilities, and stealth features into their products. Companies also invest heavily in R&D to stay ahead of evolving defense needs while fostering strategic partnerships with government agencies to align with national defense priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Drone type trends

- 2.2.2 Payload capacity trends

- 2.2.3 Power source trends

- 2.2.4 Technology trends

- 2.2.5 Application trends

- 2.2.6 Launching mode trends

- 2.2.7 End use application trends

- 2.2.8 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Force modernization and rising defense spending

- 3.2.1.2 Rapid technological advancements in AI, sensors, and autonomy

- 3.2.1.3 Escalating security threat landscape and geopolitical instability

- 3.2.1.4 Regulatory shifts and export liberalization

- 3.2.1.5 Strategic alliances and supply-chain expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and procurement costs

- 3.2.2.2 Stringent regulatory and export control restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of artificial intelligence and machine learning

- 3.2.3.2 Expansion of swarm drone capabilities

- 3.2.3.3 Growing adoption of hybrid and stealth technologies

- 3.2.3.4 Export potential to emerging defense markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Drone Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed-wing drones

- 5.3 Rotary-wing drones

- 5.3.1 Single-rotor

- 5.3.2 Multi-rotor

- 5.4 Hybrid drones

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Up to 2 kg

- 6.3 2 kg to 19 kg

- 6.4 20 kg to 100 kg

- 6.5 Above 100 kg

Chapter 7 Market Estimates and Forecast, By Power Source, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Battery-powered

- 7.3 Hybrid-powered

- 7.4 Fuel-powered

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Remotely operated drones

- 8.3 Semi-autonomous drones

- 8.4 Fully autonomous drones

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Lethal combat drones

- 9.3 Stealth drones

- 9.4 Loitering munition drones

- 9.5 Target drones

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Launching Mode, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 Vertical take-off and landing (VTOL)

- 10.3 Automatic take-off and landing (ATOL)

- 10.4 Catapult-launched drones

- 10.5 Hand-launched drones

Chapter 11 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Units)

- 11.1 Key trends

- 11.2 Military operations

- 11.2.1 Strategic surveillance

- 11.2.2 Tactical combat

- 11.2.3 Reconnaissance missions

- 11.3 Training & simulation

- 11.3.1 Combat training

- 11.3.2 Target practice

- 11.4 Border & maritime security

- 11.4.1 Coastal surveillance

- 11.4.2 Border patrol

- 11.5 Counter-terrorism & law enforcement

- 11.5.1 Urban surveillance

- 11.5.2 Tactical interventions

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Northrop Grumman Corporation

- 13.1.2 Raytheon Technologies Corporation (RTX)

- 13.1.3 Lockheed Martin Corporation

- 13.2 Regional Key Players

- 13.2.1 North America

- 13.2.1.1 General Atomics Aeronautical Systems, Inc.

- 13.2.1.2 AeroVironment, Inc.

- 13.2.1.3 The Boeing Company (Insitu, Inc.)

- 13.2.2 Europe

- 13.2.2.1 Airbus SE

- 13.2.2.2 Leonardo S.p.A.

- 13.2.2.3 BAE Systems plc

- 13.2.3 APAC

- 13.2.3.1 Israel Aerospace Industries Ltd. (IAI)

- 13.2.3.2 Turkish Aerospace Industries, Inc. (TAI)

- 13.2.3.3 Safran SA

- 13.2.1 North America

- 13.3 Niche Players / Disruptors

- 13.3.1 Elbit Systems Ltd.

- 13.3.2 QinetiQ Group plc

- 13.3.3 Kratos Defense & Security Solutions, Inc.

- 13.3.4 Anduril Industries, Inc.

- 13.3.5 Textron Inc.

- 13.3.6 Thales Group

- 13.3.7 Griffon Aerospace

- 13.3.8 Sistemas de Control Remoto (SCR)

全球作戰無人機市場:2026-2036年

全球作戰無人機市場:2026-2036年 2026-2030年全球軍用無人機市場

2026-2030年全球軍用無人機市場 軍用無人機市場:2026-2032年全球市場預測(按無人機類型、設計類型、推進方式、運行模式、航程、應用、最終用戶和分銷管道分類)

軍用無人機市場:2026-2032年全球市場預測(按無人機類型、設計類型、推進方式、運行模式、航程、應用、最終用戶和分銷管道分類) 2026年全球作戰無人機市場報告2026年全球國防無人機市場報告2026年全球無人機戰爭市場報告2026年全球軍用無人機市場報告無人機作戰市場:2026-2032年全球市場預測(按無人機類型、功能、操作模式、航程、應用和最終用戶分類)作戰無人機市場:按類型、航程、技術、發射方式、應用和最終用戶分類-2026-2032年全球市場預測

2026年全球作戰無人機市場報告2026年全球國防無人機市場報告2026年全球無人機戰爭市場報告2026年全球軍用無人機市場報告無人機作戰市場:2026-2032年全球市場預測(按無人機類型、功能、操作模式、航程、應用和最終用戶分類)作戰無人機市場:按類型、航程、技術、發射方式、應用和最終用戶分類-2026-2032年全球市場預測 軍用無人機市場規模、佔有率、成長率及全球市場分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測

軍用無人機市場規模、佔有率、成長率及全球市場分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測