|

市場調查報告書

商品編碼

1822651

視訊遠端資訊處理市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Video Telematics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

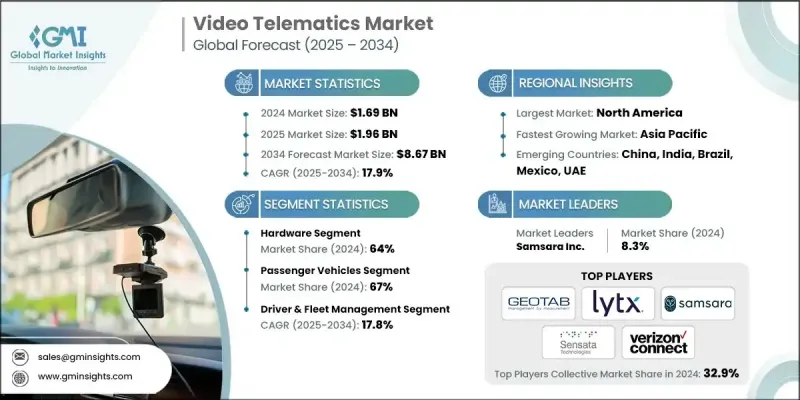

根據 Global Market Insights Inc. 發布的最新報告,全球視訊遠端資訊處理市場規模在 2024 年估計為 16.9 億美元,預計將從 2025 年的 19.6 億美元成長到 2034 年的 86.7 億美元,複合年成長率為 17.9%。

美國 ELD(電子記錄設備)授權和其他全球安全標準等法規正在推動車隊管理人員採用整合視訊和遠端資訊處理解決方案,以確保法律合規性和報告準確性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16.9億美元 |

| 預測值 | 86.7億美元 |

| 複合年成長率 | 17.9% |

硬體採用率不斷上升

2024年,硬體領域佔據了顯著佔有率,這主要得益於行車記錄器、車內攝影機、DVR以及感測器配件等設備的推動。隨著車隊營運商越來越重視即時視覺洞察以確保安全性和合規性,對堅固耐用、高解析度且整合AI功能的硬體的需求持續成長。製造商正致力於提升設備的耐用性、連接性和安裝便利性,以支援從乘用車到長途卡車等各種車型。

乘用車需求不斷成長

2025-2034年,乘用車市場將迎來強勁成長,這得益於人身安全、保險折扣和防盜需求的不斷成長。叫車服務、公司車隊,甚至個人消費者都在為車輛配備智慧行車記錄儀,以提供即時警報、駕駛行為追蹤和事故記錄功能。各公司正在客製化解決方案,使其更加謹慎、方便用戶使用,並與行動應用程式相容,以吸引這群精通科技的人。

駕駛員和車隊管理獲得牽引力

駕駛員和車隊管理細分市場在2024年佔據了顯著的佔有率,這得益於企業對監控駕駛員行為、提高燃油效率和降低營運風險的需求。即時視訊結合GPS、加速計和人工智慧分析技術,使車隊管理人員能夠偵測疲勞駕駛、分心駕駛、急煞車和路線偏差等情況。這種數據豐富的方法使管理人員能夠有效地指導駕駛員,同時最佳化路線和維護計劃。隨著雲端整合和即時決策的持續創新推動各行各業的採用,該細分市場的規模預計將超過30億美元。

區域洞察

北美將成為推動力地區

2024年,北美視訊遠端資訊處理市場佔據了強勁的市場佔有率,這得益於嚴格的車隊安全法規、商用車普及率的提高以及駕駛員責任意識的不斷增強。光是美國就佔據了相當大的市場收入佔有率,其應用領域涵蓋物流、現場服務、客運和公共部門車隊。強大的基礎設施和高技術滲透率使北美成為視訊遠端資訊處理應用持續創新和擴展的有利環境。

視訊遠端資訊處理市場的主要參與者有 Trimble Transportation(Trimble Inc.)、Nauto、Verizon Connect(Verizon Communications Inc.)、VisionTrack、Lytx、Geotab、SmartWitness(Sensata Technologies)、MiX Telematics、Samsara 和 Netradyne。

為了鞏固市場地位,視訊遠端資訊處理市場中的公司正專注於人工智慧驅動的創新、策略合作夥伴關係以及針對特定產業的解決方案。市場領導者正在嵌入人工智慧,以實現即時駕駛指導、自動事故偵測和預測性維護洞察。與保險公司、車隊租賃公司和物流供應商的合作有助於擴大客戶群並改善服務整合。

目錄

第1章:方法論

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- GMI 專有 AI 系統

- 人工智慧驅動的研究增強

- 來源一致性協議

- 人工智慧準確度指標

- 預測模型

- 初步研究和驗證

- 市場估計的主要趨勢

- 量化市場影響分析

- 生長參數對預測的數學影響

- 情境分析框架

- 一些主要來源(但不限於)

- 資料探勘來源

- 次要

- 付費來源

- 公共資源

- 來源(按地區)

- 次要

- 研究路徑和信心評分

- 研究路徑組成部分:

- 評分組件

- 研究透明度附錄

- 來源歸因框架

- 品質保證指標

- 我們對信任的承諾

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 事故率的上升推動了監控解決方案的採用。

- 政府強制要求採取電子記錄和安全措施。

- 保險與詐欺預防

- 車隊旨在透過路線和燃料最佳化來削減成本。

- 人工智慧、物聯網和雲端增強了視訊遠端資訊處理功能。

- 產業陷阱與挑戰

- 實施成本高

- 資料隱私和安全問題

- 市場機會

- 電子商務和物流需求不斷成長

- 人工智慧與高階分析整合

- 新興市場擴張

- 保險遠端資訊處理程序

- 成長動力

- 技術與創新格局

- 硬體組件和攝影系統

- 多攝影機配置和放置

- 影像感測器技術和解析度

- 儲存和資料管理系統

- 連接和通訊模組

- 軟體平台和分析引擎

- 即時視訊處理演算法

- 人工智慧和機器學習整合

- 事件檢測與分類

- 駕駛員行為分析與評分

- 雲端基礎架構和資料管理

- 視訊儲存和檢索系統

- 邊緣運算和本地處理

- 資料壓縮和頻寬最佳化

- API 整合和第三方連接

- 使用者介面和儀表板系統

- 車隊經理儀表板和報告

- 促進要素行動應用程式

- 即時警報和通知系統

- 硬體組件和攝影系統

- 成長潛力分析

- 監管格局

- 全球隱私與資料保護框架

- 運輸和車隊安全法規

- 保險和風險管理法規

- 網路安全和資料安全標準

- 波特的分析

- PESTEL分析

- 技術趨勢與創新

- 人工智慧和機器學習的進步

- 電腦視覺和物體識別

- 用於語音分析的自然語言處理

- 預測模型和風險評估

- 邊緣運算和即時處理

- 裝置上的 AI 處理能力

- 減少延遲和頻寬要求

- 離線操作和資料同步

- 先進的相機和感光元件技術

- 4K 和超高清影片

- 夜視和低光性能

- 360度多角度覆蓋

- 與物聯網和聯網汽車生態系統的整合

- 車聯網 (V2X) 通訊

- 智慧基礎設施整合

- 互聯車隊生態系統發展

- 人工智慧和機器學習的進步

- 專利分析

- 用例

- 最佳情況

- 消費者行為分析

- 成本效益分析與投資報酬率框架

- 總擁有成本(TCO)分析

- 投資報酬率(ROI)模型

- 實施和部署成本分析

- 按行業垂直分類的財務影響評估

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 新興競爭威脅

- 新市場進入者

- 科技顛覆者

- 替代商業模式

- 競爭情報框架

- 重要新聞和舉措

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 市場進入障礙與競爭護城河

- 技術和智慧財產權保護

- 客戶轉換成本和鎖定

- 規模和網路效應

第5章:市場估計與預測:依組件分類,2021 - 2034 年

- 主要趨勢

- 硬體

- 行車記錄儀

- GPS追蹤設備

- 感應器

- 車載診斷 (OBD) 設備

- 軟體

- 視訊分析和人工智慧處理軟體

- 車隊管理和儀表板平台

- 整合和 API 軟體

- 服務

- 安裝服務

- 維護和支援服務

- 託管服務

- 諮詢服務

第6章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 嵌入式系統

- 互聯系統

- 獨立系統

第7章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車

- 輕型商用車(LCV)

- 中型商用車(HCV)

- 重型商用車(HCV)

- 特種車輛和緊急車輛

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 駕駛員和車隊管理

- 預測性維護

- 保險遠端資訊處理

- 資產追蹤

- 執法

第9章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- 運輸與物流

- 建築和基礎設施

- 衛生保健

- 零售和消費者服務

- 政府和公共安全

- 能源和公用事業

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球領導者

- Geotab

- 萊特克斯

- 輪迴

- 天寶

- 威瑞森通訊

- Motive Technologies(原 KeepTruckin)

- 阿祖加

- Webfleet Solutions(普利司通)

- Teletrac 導航員

- 地區球員/冠軍

- 艦隊完成

- MiX 遠端資訊處理

- 森薩塔科技

- Quartix技術公司

- 速康有限公司

- 視覺追蹤

- 新興參與者/顛覆者

- 美國電話電報公司

- 艦隊攝影機

- LightMetrics

- 諾托

- Netradyne

- 一步式GPS

The global video telematics market was estimated at USD 1.69 billion in 2024 and is expected to grow from USD 1.96 billion in 2025 to USD 8.67 billion by 2034, at a CAGR of 17.9%, according to the latest report published by Global Market Insights Inc.

Regulations such as the ELD (Electronic Logging Device) mandate in the U.S. and other global safety standards are pushing fleet managers to adopt integrated video and telematics solutions to ensure legal compliance and reporting accuracy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.69 Billion |

| Forecast Value | $8.67 Billion |

| CAGR | 17.9% |

Rising Adoption in Hardware

The hardware segment held a notable share in 2024, driven by devices such as dashcams, in-cabin cameras, DVRs, and sensor-enabled accessories. As fleet operators increasingly prioritize real-time visual insights for safety and compliance, the demand for rugged, high-resolution, and AI-integrated hardware continues to rise. Manufacturers are focusing on improving device durability, connectivity, and ease of installation to support diverse vehicle types, from passenger cars to long-haul trucks.

Growing Demand in Passenger Vehicles

The passenger vehicles segment will witness strong growth during 2025-2034, driven by the rising demand for personal safety, insurance discounts, and theft prevention. Ride-hailing services, company car fleets, and even private consumers are equipping vehicles with intelligent dashcams that offer real-time alerts, driver behavior tracking, and accident recording capabilities. Companies tailoring solutions to be discreet, user-friendly, and compatible with mobile apps to appeal to this tech-savvy demographic.

Driver & Fleet Management to Gain Traction

The driver & fleet management segment generated a notable share in 2024, driven by the organizations ' need to monitor driver behavior, improve fuel efficiency, and reduce operational risk. Real-time video combined with GPS, accelerometers, and AI-powered analytics allows fleet managers to detect fatigue, distracted driving, harsh braking, and route deviations. This data-rich approach empowers managers to coach drivers effectively while optimizing routes and maintenance schedules. The segment is on track to exceed USD 3 billion, with continuous innovations in cloud integration and real-time decision-making driving adoption across industries.

Regional Insights

North America to Emerge as a Propelling Region

North America video telematics market held a robust share in 2024, driven by stringent fleet safety regulations, rising commercial vehicle adoption, and increasing awareness around driver accountability. The U.S. alone is responsible for a significant portion of market revenue, with adoption spanning logistics, field services, passenger transport, and public sector fleets. Robust infrastructure and high technology penetration make North America a favorable environment for continuous innovation and expansion in video telematics applications.

Major players in the video telematics market are Trimble Transportation (Trimble Inc.), Nauto, Verizon Connect (Verizon Communications Inc.), VisionTrack, Lytx, Geotab, SmartWitness (Sensata Technologies), MiX Telematics, Samsara, and Netradyne.

To solidify their presence, companies in the video telematics market are focusing on AI-driven innovation, strategic partnerships, and vertical-specific solutions. Market leaders are embedding artificial intelligence to enable real-time driver coaching, automated incident detection, and predictive maintenance insights. Collaborations with insurance firms, fleet leasing companies, and logistics providers help expand customer bases and improve service integration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.1.6 GMI proprietary AI system

- 1.1.6.1 AI-Powered research enhancement

- 1.1.6.2 Source consistency protocol

- 1.1.6.3 AI accuracy metrics

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Research Trail & Confidence Scoring

- 1.6.1 Research Trail Components:

- 1.6.2 Scoring Components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing accident rates drive adoption of monitoring solutions.

- 3.2.1.2 Governments mandate electronic logging and safety measures.

- 3.2.1.3 Insurance & Fraud Prevention

- 3.2.1.4 Fleets aim to cut costs through route and fuel optimization.

- 3.2.1.5 AI, IoT, and cloud enhance video telematics capabilities.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Implementation Costs

- 3.2.2.2 Data Privacy & Security Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Growing E-commerce & Logistics Demand

- 3.2.3.2 AI & Advanced Analytics Integration

- 3.2.3.3 Expansion in Emerging Markets

- 3.2.3.4 Insurance Telematics Programs

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.3.1 Hardware components and camera systems

- 3.3.1.1 Multi-camera configuration and placement

- 3.3.1.2 Image sensor technology and resolution

- 3.3.1.3 Storage and data management systems

- 3.3.1.4 Connectivity and communication modules

- 3.3.2 Software platform and analytics engine

- 3.3.2.1 Real-time video processing algorithms

- 3.3.2.2 AI and machine learning integration

- 3.3.2.3 Event detection and classification

- 3.3.2.4 Driver behavior analysis and scoring

- 3.3.3 Cloud infrastructure and data management

- 3.3.3.1 Video storage and retrieval systems

- 3.3.3.2 Edge computing and local processing

- 3.3.3.3 Data compression and bandwidth optimization

- 3.3.3.4 API integration and third-party connectivity

- 3.3.4 User interface and dashboard systems

- 3.3.4.1 Fleet manager dashboard and reporting

- 3.3.4.2 Driver mobile applications

- 3.3.4.3 Real-time alert and notification systems

- 3.3.1 Hardware components and camera systems

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 Global privacy and data protection framework

- 3.5.2 Transportation and fleet safety regulations

- 3.5.3 Insurance and risk management regulations

- 3.5.4 Cybersecurity and data security standards

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology trends and innovations

- 3.8.1 Artificial intelligence and machine learning advancement

- 3.8.1.1 Computer vision and object recognition

- 3.8.1.2 Natural language processing for voice analysis

- 3.8.1.3 Predictive modeling and risk assessment

- 3.8.2 Edge computing and real-time processing

- 3.8.2.1 On-device AI processing capabilities

- 3.8.2.2 Reduced latency and bandwidth requirements

- 3.8.2.3 Offline operation and data synchronization

- 3.8.3 Advanced camera and sensor technology

- 3.8.3.1 4K and ultra-high definition video

- 3.8.3.2 Night vision and low-light performance

- 3.8.3.3 360-degree and multi-angle coverage

- 3.8.4 Integration with IoT and connected vehicle ecosystem

- 3.8.4.1 Vehicle-to-everything (V2X) communication

- 3.8.4.2 Smart infrastructure integration

- 3.8.4.3 Connected fleet ecosystem development

- 3.8.1 Artificial intelligence and machine learning advancement

- 3.9 Patent analysis

- 3.10 Use cases

- 3.11 Best-case scenario

- 3.12 Consumer behaviour analysis

- 3.13 Cost-benefit analysis and ROI framework

- 3.13.1 Total cost of ownership (TCO) analysis

- 3.13.2 Return on investment (ROI) models

- 3.13.3 Implementation and deployment cost analysis

- 3.13.4 Financial impact assessment by industry vertical

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Emerging competitive threats

- 4.6.1 New market entrants

- 4.6.2 Technology disruptors

- 4.6.3 Alternative business models

- 4.6.4 Competitive intelligence framework

- 4.7 Key news and initiatives

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans and funding

- 4.8 Market entry barriers and competitive moats

- 4.8.1 Technology and IP protection

- 4.8.2 Customer switching costs and lock-in

- 4.8.3 Scale and network effects

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Dash cams

- 5.2.2 GPS tracking devices

- 5.2.3 Sensors

- 5.2.4 Onboard diagnostics (OBD) devices

- 5.3 Software

- 5.3.1 Video analytics and AI processing software

- 5.3.2 Fleet management and dashboard platforms

- 5.3.3 Integration and API software

- 5.4 Services

- 5.4.1 Installation services

- 5.4.2 Maintenance & support services

- 5.4.3 Managed services

- 5.4.4 Consulting services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Embedded systems

- 6.3 Connected systems

- 6.4 Standalone systems

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (HCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

- 7.4 Specialty and emergency vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Driver & fleet management

- 8.3 Predictive maintenance

- 8.4 Insurance telematics

- 8.5 Asset tracking

- 8.6 Law enforcement

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Transportation & logistics

- 9.3 Construction and infrastructure

- 9.4 Healthcare

- 9.5 Retail and consumer services

- 9.6 Government & public safety

- 9.7 Energy and utilities

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1.1 Global Leaders

- 11.1.1.1 Geotab

- 11.1.1.2 Lytx

- 11.1.1.3 Samsara

- 11.1.1.4 Trimble

- 11.1.1.5 Verizon Communications

- 11.1.1.6 Motive Technologies (formerly KeepTruckin)

- 11.1.1.7 Azuga

- 11.1.1.8 Webfleet Solutions (Bridgestone)

- 11.1.1.9 Teletrac Navman

- 11.1.2 Regional Players / Champions

- 11.1.2.1 Fleet Complete

- 11.1.2.2 MiX Telematics

- 11.1.2.3 Sensata Technologies

- 11.1.2.4 Quartix Technologies

- 11.1.2.5 SureCam Limited

- 11.1.2.6 VisionTrack

- 11.1.3 Emerging Players / Disruptors

- 11.1.3.1 AT&T

- 11.1.3.2 FleetCam

- 11.1.3.3 LightMetrics

- 11.1.3.4 Nauto

- 11.1.3.5 Netradyne

- 11.1.3.6 One Step GPS