|

市場調查報告書

商品編碼

1822632

軟體定義資料中心市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Software-Defined Data Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

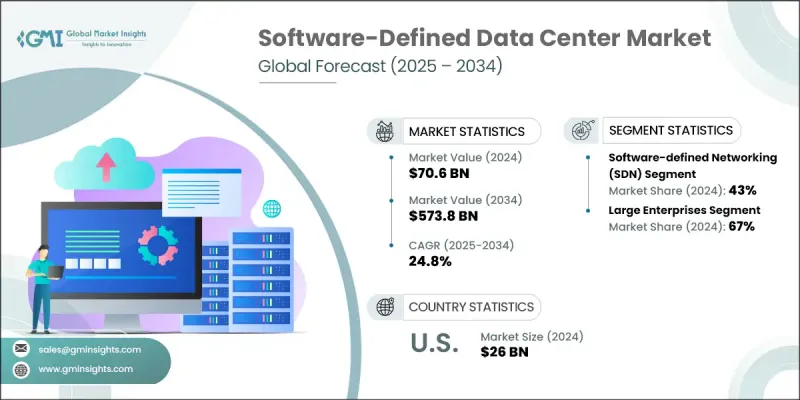

2024 年全球軟體定義資料中心市場價值為 706 億美元,預計到 2034 年將以 24.8% 的複合年成長率成長,達到 5,738 億美元。

資料中心架構的這種轉變正在推動企業設計和管理基礎架構方式的重大變革。企業不再只依賴僵化的硬體驅動模式,而是轉向軟體驅動、敏捷且可擴展的框架。人工智慧、機器學習和意圖式網路與 SDDC 解決方案的整合正在迅速改變人們的期望。因此,對了解跨領域技術(例如編排、虛擬化和雲端原生基礎架構)的專業人員的需求日益成長。高級認證和持續培訓對於確保最佳性能和營運敏捷性至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 706億美元 |

| 預測值 | 5738億美元 |

| 複合年成長率 | 24.8% |

企業數位轉型的演變,尤其是在以技術為中心的公私合作領域,正在為軟體定義資料中心 (SDDC) 的採用提供更強勁的動力。早在疫情爆發之前,企業就已開始從傳統的硬體模式轉型為虛擬化、軟體定義的環境,以降低成本並提升靈活性。這種轉變在電信、金融服務、保險和保險業 (BFSI) 以及超大規模雲端服務供應商等產業最為明顯。雖然私有雲和混合雲端模式先前已獲得廣泛應用,但大規模部署的步伐此前一直受到高昂的前期投資需求和熟練專家短缺的阻礙。然而,自動化和統一基礎設施管理的快速發展正在幫助消除這些障礙。

2024年,軟體定義網路 (SDN) 佔據了43%的市場佔有率,預計到2034年將以23%的複合年成長率成長。基於人工智慧的自動化技術正在徹底改變SDN,它能夠實現即時流量控制、預測性問題檢測以及基於即時工作負載的動態網路配置。隨著網路變得更加智慧和自主配置,企業正在減少停機時間,同時提升邊緣和多雲環境下的服務效能。這些進步也有助於減少人工干預,同時增強整個生態系統的可擴展性和網路安全。

大型企業在2024年佔了67%的佔有率,預計在2025年至2034年期間將以20%的複合年成長率成長。這些企業正引領向人工智慧整合分析的轉變,這些分析有助於最佳化工作負載、預測硬體問題並實現自主基礎設施管理。隨著即時智慧嵌入運算、儲存和網路元件,企業正在獲得敏捷性和更快的投資回報。這種層級的智慧資源分配支援滿足不斷變化的業務需求和擴展所需的靈活性,而不受傳統系統的限制。

美國軟體定義資料中心市場佔了90%的市場佔有率,2024年市場規模達到260億美元。美國的主導地位得益於其廣泛採用的混合雲和多雲模式、積極的數位基礎設施建設以及深厚的供應商生態系統。企業級自動化投資的強勁成長(尤其是在財富500強企業中)也推動了這一成長。此外,科技公司、教育機構和公共部門之間的策略合作正專注於勞動力發展和數位化現代化,從而加快了整體應用步伐。

全球軟體定義資料中心市場的主要參與者包括 Nutanix、思科系統、甲骨文、華為、微軟、戴爾科技和Google。這些公司在雲端原生基礎設施、虛擬化環境和人工智慧自動化領域中引領創新。軟體定義資料中心市場的頂尖公司正在積極投資人工智慧驅動的基礎架構編排、混合雲端支援和自動化工作負載管理工具,以使自己脫穎而出。許多公司正在增強與第三方雲端平台的互通性,以提供跨公有和私有環境的無縫整合。與學術機構、政府機構和雲端原生新創公司的策略合作夥伴關係有助於建立一支熟練的員工隊伍並加速技術部署。產品開發現在專注於容器化支援、即時分析和意圖式網路。此外,華為、微軟、Google、甲骨文、思科系統、戴爾科技和 Nutanix 等公司正在優先考慮基於訂閱的模式並擴展其 SaaS 產品組合,以提高客戶保留率和長期盈利能力。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 對敏捷、可擴展的 IT 基礎架構的需求

- 人工智慧與自動化的融合

- 混合雲和多雲採用

- 資料中心虛擬化的成長

- 產業陷阱與挑戰

- 前期投資高

- 安全和合規挑戰

- 市場機會

- 邊緣運算整合

- 政府主導的數位基礎設施計劃

- 產業特定的 SDDC 解決方案

- 供應商驅動的培訓和認證

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 專利分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 人工智慧與機器學習整合

- AI 驅動的 SDDC 管理與編排

- 機器學習在基礎設施自動化的應用

- AIOps 和智慧營運

- 邊緣運算和分散式 SDDC

- Edge SDDC 架構與設計

- 5G與物聯網整合

- 邊緣用例和應用

- 容器和 Kubernetes 的演變

- 容器原生 SDDC 平台

- Kubernetes 編排與管理

- 服務網格和應用程式連接

- 量子運算和下一代技術

- 量子運算與 SDDC 的整合

- 量子安全與加密

- 量子網路與通訊

- 混合經典量子計算

- 永續性和綠色計算

- 節能的 SDDC 設計與營運

- 減少並最佳化碳足跡

- 再生能源整合

- 循環經濟與資源最佳化

- 人工智慧與機器學習整合

- 價格趨勢

- 按地區

- 按產品

- 歷史定價分析與市場演變(2019-2024)

- 軟體授權成本趨勢

- 虛擬機器管理程式和虛擬化許可

- SDN 控制器和網路軟體定價

- 儲存虛擬化軟體成本

- 管理和編排平台定價

- 企業授權協議 (ELA) 趨勢

- 硬體成本影響和最佳化

- 每個虛擬機器的伺服器硬體成本

- 儲存硬體成本最佳化

- 網路硬體減少的好處

- 商品硬體與專有解決方案

- 硬體更新周期最佳化

- 服務和支持定價的演變

- 專業服務成本趨勢

- 實施和遷移服務定價

- 持續的支援和維護成本

- 培訓和認證定價

- 託管服務和外包成本

- 軟體授權成本趨勢

- 目前 SDDC 定價格局(2024-2025 年)

- 授權模式分析與比較

- 永久許可與訂閱許可

- 按插槽定價模型與按核心定價模型

- 基於容量的定價(每 Tb、每 Vm)

- 基於使用情況和消費的定價

- 混合和多雲定價模型

- 區域定價差異及分析

- 供應商定價策略分析

- 總擁有成本 (TCO) 和投資報酬率分析

- SDDC 與傳統基礎設施 TCO 對比

- ROI計算和商業價值

- 成本最佳化策略

- 授權模式分析與比較

- 未來價格預測與市場趨勢(2025-2034)

- 短期價格預測(1-2年)

- 中期價格演變(3-5年)

- 長期價格趨勢(5-10年)

- 成本效益分析與財務建模

- 財務論證框架

- 預算規劃與分配模型

- 成本中心與利潤中心分析

- 退款和展示退款模型

- 財務風險評估與緩解

- 歷史定價分析與市場演變(2019-2024)

- 加速數位轉型場景

- 市場規模和成長預測

- 科技採用加速

- 行業縱向擴展

- 地理市場開發

- 投資和併購活動

- 人工智慧和自動化革命場景

- AI驅動的SDDC管理

- 自主基礎設施營運

- 智慧工作負載最佳化

- 預測分析和維護

- 新的服務模式和產品

- 邊緣運算普及場景

- 分散式 SDDC 架構

- 5G與物聯網融合

- 即時處理要求

- 邊緣到雲端的編排

- 新的市場機遇

- 技術突破場景

- 量子計算整合

- 先進的人工智慧和機器學習

- 下一代網路技術

- 永續和綠色計算

- 沉浸式技術(AR/VR/元宇宙)

- 監管和市場演變情景

- 數據主權和本地化要求

- 網路安全法規和標準

- 環境與永續發展任務

- 產業整合與標準化

- 開源和社群驅動的開發

- 戰略意義和建議

- 技術投資策略

- 市場進入與擴張規劃

- 夥伴關係和生態系統發展

- 創新和研發重點

- 風險緩解和應急計劃

- 案例研究

- 企業 SDDC 轉型案例研究

- 全球製造業數位轉型

- 醫療保健系統 SDDC 和合規性

- 成功案例

- 中小企業和中型市場成功案例

- 政府和公共部門實施

- 產業轉型案例

- 能源效率及成本最佳化案例

- 用例

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按解決方案,2021 - 2034 年

- 主要趨勢

- 軟體定義網路 (SDN)

- 硬體

- 軟體

- 服務

- 託管

- 專業的

- 軟體定義儲存 (SDS)

- 硬體

- 軟體

- 服務

- 託管

- 專業的

- 軟體定義計算 (SDC)

- 硬體

- 軟體

- 服務

- 託管

- 專業的

第6章:市場估計與預測:依組織規模,2021 - 2034 年

- 主要趨勢

- 中小企業

- 大型企業

第7章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- 金融服務業協會

- 零售與電子商務

- 政府

- 衛生保健

- 製造業

- IT支援服務

- 其他

第 8 章:市場估計與預測:按部署,2021 年至 2034 年

- 主要趨勢

- 本地

- 公共雲端

- 私有雲端

- 混合雲端

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 資源池化與虛擬化

- 災難復原和業務連續性

- 資料中心整合

- 動態資源分配

- DevOps 和 CI/CD 自動化

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- Advanced Systems Group

- Cisco Systems

- Citrix Systems

- Dell Technologies

- Equinix

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Hitachi Data Systems

- Huawei

- IBM

- Juniper

- Microsoft

- NEC Corporation of America

- NetApp

- Nutanix

- Red Hat

- VMware

- 區域參與者

- Cloudistics

- DriveScale

- Maxta

- Nexenta Systems

- Pluribus Networks

- QTS Realty Trust

- Rahi Systems

- SUSE

- Super Micro Computer

- Emerging and specialist players

- Atlantis Computing

- Cloudistics

- Maxta

- Cloud and hyperscale players

- Alibaba Cloud

- Amazon Web Services (AWS)

- Huawei Technologies

- Oracle

The Global Software-Defined Data Center Market was valued at USD 70.6 billion in 2024 and is estimated to grow at a CAGR of 24.8% to reach USD 573.8 billion by 2034.

This shift in data center architecture is driving a major transformation in how organizations design and manage infrastructure. Instead of relying solely on rigid, hardware-driven models, businesses are now leaning into software-powered, agile, and scalable frameworks. The integration of AI, machine learning, and intent-based networking into SDDC solutions is rapidly evolving expectations. As a result, there is a growing demand for professionals who understand cross-domain technologies such as orchestration, virtualization, and cloud-native infrastructure. Advanced certifications and ongoing training are becoming essential for ensuring optimal performance and operational agility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $70.6 Billion |

| Forecast Value | $573.8 Billion |

| CAGR | 24.8% |

The evolution of enterprise digital transformation, especially in tech-centric public-private collaborations, is fueling stronger momentum for SDDC adoption. Even before the pandemic, companies began transitioning from traditional hardware-bound models to virtualized, software-defined environments to reduce costs and boost flexibility. This shift has been most evident across sectors such as telecom, BFSI, and hyperscale cloud providers. While private and hybrid cloud models saw earlier traction, the pace of widespread deployment was previously held back by large upfront investment needs and a shortage of skilled experts. However, rapid advancements in automation and unified infrastructure management are helping eliminate these roadblocks.

In 2024, the software-defined networking (SDN) held a 43% share and is anticipated to grow at a CAGR of 23% through 2034. AI-based automation is radically transforming SDN by enabling real-time traffic control, predictive issue detection, and dynamic network configurations based on live workloads. As networks become more intelligent and self-configuring, enterprises are reducing downtime while increasing service performance across edge and multi-cloud setups. These advances are also helping reduce manual intervention while enhancing scalability and cybersecurity throughout the ecosystem.

The large enterprises segment held a 67% share in 2024 and is projected to grow at a 20% CAGR between 2025 and 2034. These businesses are leading the shift toward AI-integrated analytics that help optimize workloads, predict hardware issues, and enable autonomous infrastructure management. With real-time intelligence embedded across compute, storage, and networking components, enterprises are gaining agility and faster ROI. This level of smart resource allocation supports the flexibility needed to meet shifting business demands and scale without the limitations of legacy systems.

United States Software-Defined Data Center Market held a 90% share and generated USD 26 billion in 2024. The US dominance is driven by its widespread adoption of hybrid and multi-cloud models, active digital infrastructure development, and deep vendor ecosystems. The strong presence of enterprise-grade automation investments-especially among Fortune 500 firms-is also pushing this growth. Moreover, strategic collaborations between technology companies, educational institutions, and public sector initiatives are focusing on workforce development and digital modernization, enhancing the overall pace of adoption.

Major players in the Global Software-Defined Data Center Market include Nutanix, Cisco Systems, Oracle, Huawei, Microsoft, Dell Technologies, and Google. These companies are leading innovation across cloud-native infrastructure, virtualized environments, and AI-powered automation. Top companies in the Software-Defined Data Center Market are aggressively investing in AI-driven infrastructure orchestration, hybrid cloud enablement, and automated workload management tools to differentiate themselves. Many are enhancing interoperability with third-party cloud platforms to provide seamless integration across public and private environments. Strategic partnerships with academic institutions, government bodies, and cloud-native startups are helping to build a skilled workforce and accelerate technology deployment. Product development now focuses on containerization support, real-time analytics, and intent-based networking. In addition, players like Huawei, Microsoft, Google, Oracle, Cisco Systems, Dell Technologies, and Nutanix are prioritizing subscription-based models and expanding their SaaS portfolios to improve customer retention and long-term profitability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Organization size

- 2.2.4 End use

- 2.2.5 Deployment

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Demand for agile, scalable IT infrastructure

- 3.2.1.2 Integration of AI and automation

- 3.2.1.3 Hybrid and multi-cloud adoption

- 3.2.1.4 Data center virtualization growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront investment

- 3.2.2.2 Security and compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Edge computing integration

- 3.2.3.2 Government-led digital infrastructure initiatives

- 3.2.3.3 Industry-specific SDDC solutions

- 3.2.3.4 Vendor-driven training and certification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.8.2.1 Artificial intelligence and machine learning integration

- 3.8.2.1.1 AI-powered SDDC management and orchestration

- 3.8.2.1.2 Machine learning for infrastructure automation

- 3.8.2.1.3 AIOps and intelligent operations

- 3.8.2.2 Edge computing and distributed SDDC

- 3.8.2.2.1 Edge SDDC architecture and design

- 3.8.2.2.2 5G and IoT integration

- 3.8.2.2.3 Edge use cases and applications

- 3.8.2.3 Container and Kubernetes evolution

- 3.8.2.3.1 Container-native SDDC platforms

- 3.8.2.3.2 Kubernetes orchestration and management

- 3.8.2.3.3 Service mesh and application connectivity

- 3.8.2.4 Quantum computing and next-generation technologies

- 3.8.2.4.1 Quantum computing integration with SDDC

- 3.8.2.4.2 Quantum-safe security and encryption

- 3.8.2.4.3 Quantum networking and communication

- 3.8.2.4.4 Hybrid classical-quantum computing

- 3.8.2.5 Sustainability and green computing

- 3.8.2.5.1 Energy-efficient SDDC design and operations

- 3.8.2.5.2 Carbon footprint reduction and optimization

- 3.8.2.5.3 Renewable energy integration

- 3.8.2.5.4 Circular economy and resource optimization

- 3.8.2.1 Artificial intelligence and machine learning integration

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.9.2.1 Historical pricing analysis and market evolution (2019-2024)

- 3.9.2.1.1 Software licensing cost trends

- 3.9.2.1.1.1 Hypervisor and virtualization licensing

- 3.9.2.1.1.2 SDN controller and network software pricing

- 3.9.2.1.1.3 Storage virtualization software costs

- 3.9.2.1.1.4 Management and orchestration platform pricing

- 3.9.2.1.1.5 Enterprise license agreement (ELA) trends

- 3.9.2.1.2 Hardware cost impact and optimization

- 3.9.2.1.2.1 Server hardware cost per virtual machine

- 3.9.2.1.2.2 Storage hardware cost optimization

- 3.9.2.1.2.3 Network hardware reduction benefits

- 3.9.2.1.2.4 Commodity hardware vs proprietary solutions

- 3.9.2.1.2.5 Hardware refresh cycle optimization

- 3.9.2.1.3 Service and support pricing evolution

- 3.9.2.1.3.1 Professional services cost trends

- 3.9.2.1.3.2 Implementation and migration service pricing

- 3.9.2.1.3.3 Ongoing support and maintenance costs

- 3.9.2.1.3.4 Training and certification pricing

- 3.9.2.1.3.5 Managed services and outsourcing costs

- 3.9.2.1.1 Software licensing cost trends

- 3.9.2.2 Current SDDC pricing landscape (2024-2025)

- 3.9.2.2.1 Licensing model analysis and comparison

- 3.9.2.2.1.1 Perpetual vs subscription licensing

- 3.9.2.2.1.2 Per-socket vs per-core pricing models

- 3.9.2.2.1.3 Capacity-based pricing (per Tb, per Vm)

- 3.9.2.2.1.4 Usage-based and consumption pricing

- 3.9.2.2.1.5 Hybrid and multi-cloud pricing models

- 3.9.2.2.2 Regional pricing variations and analysis

- 3.9.2.2.3 Vendor pricing strategy analysis

- 3.9.2.2.4 Total cost of ownership (TCO) and ROI analysis

- 3.9.2.2.4.1 SDDC vs traditional infrastructure TCO

- 3.9.2.2.4.2 ROI calculation and business value

- 3.9.2.2.4.3 Cost optimization strategies

- 3.9.2.2.1 Licensing model analysis and comparison

- 3.9.2.3 Future pricing projections and market trends (2025-2034)

- 3.9.2.3.1 Short-term pricing forecast (1-2 years)

- 3.9.2.3.2 Medium-term pricing evolution (3-5 years)

- 3.9.2.3.3 Long-term price trends (5-10 years)

- 3.9.2.4 Cost-benefit analysis and financial modeling

- 3.9.2.4.1 Financial justification frameworks

- 3.9.2.4.2 Budget planning and allocation models

- 3.9.2.4.3 Cost center vs profit center analysis

- 3.9.2.4.4 Chargeback and show back models

- 3.9.2.4.5 Financial risk assessment and mitigation

- 3.9.2.1 Historical pricing analysis and market evolution (2019-2024)

- 3.10 Accelerated digital transformation scenario

- 3.10.1 Market size and growth projections

- 3.10.2 Technology adoption acceleration

- 3.10.3 Industry vertical expansion

- 3.10.4 Geographic market development

- 3.10.5 Investment and M&A activity

- 3.11 AI and automation revolution scenario

- 3.11.1 AI-driven SDDC management

- 3.11.2 Autonomous infrastructure operations

- 3.11.3 Intelligent workload optimization

- 3.11.4 Predictive analytics and maintenance

- 3.11.5 New service models and offerings

- 3.12 Edge computing proliferation scenario

- 3.12.1 Distributed SDDC architecture

- 3.12.2. 5 g and IoT integration

- 3.12.3 Real-time processing requirements

- 3.12.4 Edge-to-cloud orchestration

- 3.12.5 New market opportunities

- 3.13 Technology breakthrough scenarios

- 3.13.1 Quantum computing integration

- 3.13.2 Advanced AI and machine learning

- 3.13.3 Next-generation networking technologies

- 3.13.4 Sustainable and green computing

- 3.13.5 Immersive technologies (AR/VR/metaverse)

- 3.14 Regulatory and market evolution scenarios

- 3.14.1 Data sovereignty and localization requirements

- 3.14.2 Cybersecurity regulations and standards

- 3.14.3 Environmental and sustainability mandates

- 3.14.4 Industry consolidation and standardization

- 3.14.5 Open source and community-driven development

- 3.15 Strategic implications and recommendations

- 3.15.1 Technology investment strategies

- 3.15.2 Market entry and expansion planning

- 3.15.3 Partnership and ecosystem development

- 3.15.4 Innovation and R&D priorities

- 3.15.5 Risk mitigation and contingency planning

- 3.16 Case studies

- 3.16.1 Enterprise SDDC transformation case studies

- 3.16.2 Global manufacturing company digital transformation

- 3.16.3 Healthcare system SDDC and compliance

- 3.17 Success stories

- 3.17.1 SME and mid-market success stories

- 3.17.2 Government and public sector implementations

- 3.17.3 Industry-specific transformation cases

- 3.17.4 Energy efficiency and cost optimization cases

- 3.18 Use cases

- 3.19 Sustainability and environmental aspects

- 3.19.1 Sustainable practices

- 3.19.2 Waste reduction strategies

- 3.19.3 Energy efficiency in production

- 3.19.4 Eco-friendly Initiatives

- 3.19.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Software-defined networking (SDN)

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.2.3.1 Managed

- 5.2.3.2 Professional

- 5.3 Software-defined storage (SDS)

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.3.3.1 Managed

- 5.3.3.2 Professional

- 5.4 Software-defined compute (SDC)

- 5.4.1 Hardware

- 5.4.2 Software

- 5.4.3 Services

- 5.4.3.1 Managed

- 5.4.3.2 Professional

Chapter 6 Market Estimates & Forecast, By Organization size, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 SME

- 6.3 Large enterprises

Chapter 7 Market Estimates & Forecast, By End use, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Retail and e-commerce

- 7.4 Government

- 7.5 Healthcare

- 7.6 Manufacturing

- 7.7 IT-enabled services

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Public cloud

- 8.4 Private cloud

- 8.5 Hybrid cloud

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Resource pooling & virtualization

- 9.3 Disaster recovery & business continuity

- 9.4 Data center consolidation

- 9.5 Dynamic resource allocation

- 9.6 DevOps and CI/CD automation

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Advanced Systems Group

- 11.1.2 Cisco Systems

- 11.1.3 Citrix Systems

- 11.1.4 Dell Technologies

- 11.1.5 Equinix

- 11.1.6 Fujitsu

- 11.1.7 Hewlett Packard Enterprise (HPE)

- 11.1.8 Hitachi Data Systems

- 11.1.9 Huawei

- 11.1.10 IBM

- 11.1.11 Juniper

- 11.1.12 Microsoft

- 11.1.13 NEC Corporation of America

- 11.1.14 NetApp

- 11.1.15 Nutanix

- 11.1.16 Red Hat

- 11.1.17 VMware

- 11.2 Regional players

- 11.2.1 Cloudistics

- 11.2.2 DriveScale

- 11.2.3 Maxta

- 11.2.4 Nexenta Systems

- 11.2.5 Pluribus Networks

- 11.2.6 QTS Realty Trust

- 11.2.7 Rahi Systems

- 11.2.8 SUSE

- 11.2.9 Super Micro Computer

- 11.3 Emerging and specialist players

- 11.3.1 Atlantis Computing

- 11.3.2 Cloudistics

- 11.3.3 Maxta

- 11.4 Cloud and hyperscale players

- 11.4.1 Alibaba Cloud

- 11.4.2 Amazon Web Services (AWS)

- 11.4.3 Google

- 11.4.4 Huawei Technologies

- 11.4.5 Oracle

2026年全球軟體定義資料中心市場報告

2026年全球軟體定義資料中心市場報告 軟體定義資料中心市場:按元件、資料中心類型、應用領域、最終使用者類型、產業和部署方式分類-全球預測,2026-2032年

軟體定義資料中心市場:按元件、資料中心類型、應用領域、最終使用者類型、產業和部署方式分類-全球預測,2026-2032年 軟體定義資料中心 (SDDC) 市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

軟體定義資料中心 (SDDC) 市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 軟體定義資料中心市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

軟體定義資料中心市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 軟體定義資料中心市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、類型、部署方式、垂直產業、地區和競爭格局分類),2021-2031年

軟體定義資料中心市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、類型、部署方式、垂直產業、地區和競爭格局分類),2021-2031年 2026-2030年全球軟體定義資料中心(SDDC)市場

2026-2030年全球軟體定義資料中心(SDDC)市場 軟體定義資料中心市場規模、佔有率和成長分析(按組件、部署模式、企業規模、垂直產業和地區分類)-2026年至2033年產業預測

軟體定義資料中心市場規模、佔有率和成長分析(按組件、部署模式、企業規模、垂直產業和地區分類)-2026年至2033年產業預測 全球軟體定義資料中心(SDDC)市場:依產品、組織規模、最終用戶產業、地區、機會和預測,2018-2032

全球軟體定義資料中心(SDDC)市場:依產品、組織規模、最終用戶產業、地區、機會和預測,2018-2032 全球軟體定義資料中心市場規模、佔有率和趨勢分析:按組件、類型、部署、企業規模、最終用途、地區和細分市場,預測 2025-2033 年

全球軟體定義資料中心市場規模、佔有率和趨勢分析:按組件、類型、部署、企業規模、最終用途、地區和細分市場,預測 2025-2033 年 2032 年軟體定義資料中心市場預測:按類型、組件、組織規模、部署類型、最終用戶和地區進行的全球分析

2032 年軟體定義資料中心市場預測:按類型、組件、組織規模、部署類型、最終用戶和地區進行的全球分析