|

市場調查報告書

商品編碼

1822618

鐵粉市場機會、成長動力、產業趨勢分析及2025-2034年預測Iron Powder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

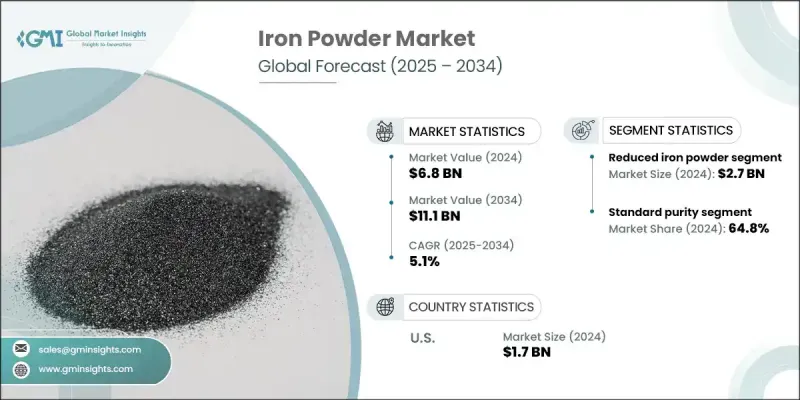

全球鐵粉市場價值 68 億美元,預計到 2034 年將以 5.1% 的複合年成長率成長,達到 111 億美元,這得益於生產流程的技術進步。包括精煉粉末生產技術和增強的品質控制標準在內的創新正在提升鐵粉的性能。這些改進使其能夠用於從汽車到電子產品的更廣泛的應用領域。此外,粉末冶金技術的進步和積層製造的興起使生產更加精確和高效。大量使用鐵粉的建築和電子產業也在促進市場成長。根據世界鋼鐵協會的報告,建築業對鐵粉的需求預計每年將增加 4%。生產方法的創新,例如改進的加工技術和專門的牌號,正在進一步推動市場活力。

整個鐵粉市場按類型、純度、最終用途行業和地區進行分類。到2032年,霧化鐵粉市場將實現可觀的複合年成長率,這得益於其優於其他類型鐵粉的優異性能。霧化鐵粉的粒度和形狀均勻性極佳,從而提高了其在精密應用中的性能。其一致的品質對於需要高精度和高可靠性的行業至關重要,例如航太和高科技製造。此外,霧化技術的進步提高了生產效率,進一步提高了該領域的收入。到2032年,高純度鐵粉將佔據顯著的市場佔有率,因為它在要求最低污染的先進製造流程中發揮重要作用。高純度鐵粉對於生產具有精確特性和卓越性能的零件至關重要,尤其是在電子和製藥等高科技行業。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 68億美元 |

| 預測值 | 111億美元 |

| 複合年成長率 | 5.1% |

此外,嚴格的行業標準和法規也大幅推高了對高純度材料的需求,因為它們對於實現最佳性能和安全性至關重要。由於工業活動的增加和各行業的技術進步,北美鐵粉市場將在2024年至2032年期間呈現強勁的複合年成長率。該地區不斷擴張的汽車和航太工業正在推動製造過程中對高品質材料的需求。此外,對基礎設施建設和再生能源項目的關注,正在推動該地區建築和能源應用對鐵粉的需求增加。對積層製造創新和進步的推動也促進了對鐵粉需求的成長,從而支撐了北美市場的成長。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021-2034

- 主要趨勢

- 還原鐵粉

- 霧化鐵粉

- 電解鐵粉

第6章:市場估計與預測:依純度,2021-2034

- 主要趨勢

- 高純度

- 標準純度

第7章:市場估計與預測:依最終用途產業,2021-2034

- 主要趨勢

- 汽車

- 電子的

- 一般工業

- 消費產業

- 建造

第8章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- American Element

- BASF SE

- Belmont Metals

- CNPC Powder

- Hoganas

- Industrial Metal Powders (India) Pvt. Ltd.

- JFE Steel Corporation

- Pometon

- Reade

- Rio Tinto Metal Powder

- SAGWELL USA INC.

- Serena Nutrition

The Global Iron Powder Market was valued at USD 6.8 billion and is estimated to grow at a CAGR of 5.1% to reach USD 11.1 billion by 2034, backed by the technological advancements in production processes. Innovations, including refined powder production techniques and enhanced quality control standards, are advancing the properties of iron powder. These improvements enable its use in a wider array of applications, from automotive to electronics. Additionally, advancements in powder metallurgy and the rise of additive manufacturing are making production more precise and efficient. The construction and electronics sectors, which heavily utilize iron powder, are also contributing to market growth. According to a report by the World Steel Association, the demand for iron powder in construction is expected to rise by 4% annually. Innovations in production methods, such as improved processing techniques and specialized grades, are further driving market dynamics.

The overall iron powder market is sorted based on type, purity, End Use industry, and region. The atomized iron powder segment will register decent CAGR through 2032, driven by its superior properties compared to other types. Atomized iron powder offers excellent uniformity in particle size and shape, which enhances performance in precision applications. Its consistent quality is crucial for industries requiring high levels of accuracy and reliability, such as aerospace and high-tech manufacturing. Additionally, advancements in atomization technology have made the production process more efficient, further boosting the segment revenues. By 2032, the high-purity segment will clutch a noticeable market share, because of its role in advanced manufacturing processes that require minimal contamination. High-purity iron powder is essential for producing components with precise characteristics and superior performance, particularly in high-tech industries such as electronics and pharmaceuticals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $11.1 Billion |

| CAGR | 5.1% |

Additionally, stringent industry standards and regulations are catapulting the need for high-purity materials, as they are crucial for achieving optimal performance and safety. North America iron powder market will showcase a strong CAGR from 2024 to 2032, owing to increased industrial activity and technological advancements across various sectors. The region's expanding automotive and aerospace industries are driving the need for high-quality materials in manufacturing processes. Additionally, the focus on infrastructure development and renewable energy projects is creating a higher demand for iron powder in construction and energy applications across the region. The push for innovation and advancements in additive manufacturing also contributes to the rising demand for iron powder, bolstering the market growth in North America.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Purity trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Reduced iron powder

- 5.3 Atomised iron powder

- 5.4 Electrolytic iron powder

Chapter 6 Market Estimates and Forecast, By Purity, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 High purity

- 6.3 Standard purity

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Electronic

- 7.4 General industries

- 7.5 Consumer industries

- 7.6 Construction

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 American Element

- 9.2 BASF SE

- 9.3 Belmont Metals

- 9.4 CNPC Powder

- 9.5 Hoganas

- 9.6 Industrial Metal Powders (India) Pvt. Ltd.

- 9.7 JFE Steel Corporation

- 9.8 Pometon

- 9.9 Reade

- 9.10 Rio Tinto Metal Powder

- 9.11 SAGWELL USA INC.

- 9.12 Serena Nutrition

食品級鐵粉市場:按類型、粒徑、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

食品級鐵粉市場:按類型、粒徑、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 全球羰基鐵粉市場規模、佔有率、趨勢和成長分析報告(2026-2034年)3D列印用鐵粉市場:按類型、列印技術、粉末形態、終端用戶產業和粒徑範圍分類 - 全球預測(2026-2032年)用於 3D 列印的鐵基金屬粉末市場:按類型、製造技術、形狀、最終用途行業和配銷通路分類 - 全球預測 2026-2032 年鋼粉市場按製造技術、合金成分、粉末形態和應用分類-全球預測(2026-2032 年)全球鐵粉市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量及未來預測(2026-2034)

全球羰基鐵粉市場規模、佔有率、趨勢和成長分析報告(2026-2034年)3D列印用鐵粉市場:按類型、列印技術、粉末形態、終端用戶產業和粒徑範圍分類 - 全球預測(2026-2032年)用於 3D 列印的鐵基金屬粉末市場:按類型、製造技術、形狀、最終用途行業和配銷通路分類 - 全球預測 2026-2032 年鋼粉市場按製造技術、合金成分、粉末形態和應用分類-全球預測(2026-2032 年)全球鐵粉市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量及未來預測(2026-2034) 鐵粉市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區和細分市場預測(2025-2033 年)

鐵粉市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區和細分市場預測(2025-2033 年) 羰基氟化物:全球市場佔有率和排名、總收入和需求預測(2025-2031年)鋼粉:全球市佔率及排名、總收入及需求預測(2025-2031年)鐵粉:全球市佔率排名、總銷售額和需求預測(2025-2031年)

羰基氟化物:全球市場佔有率和排名、總收入和需求預測(2025-2031年)鋼粉:全球市佔率及排名、總收入及需求預測(2025-2031年)鐵粉:全球市佔率排名、總銷售額和需求預測(2025-2031年)