|

市場調查報告書

商品編碼

1822611

智慧水錶市場機會、成長動力、產業趨勢分析及2025-2034年預測Smart Water Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

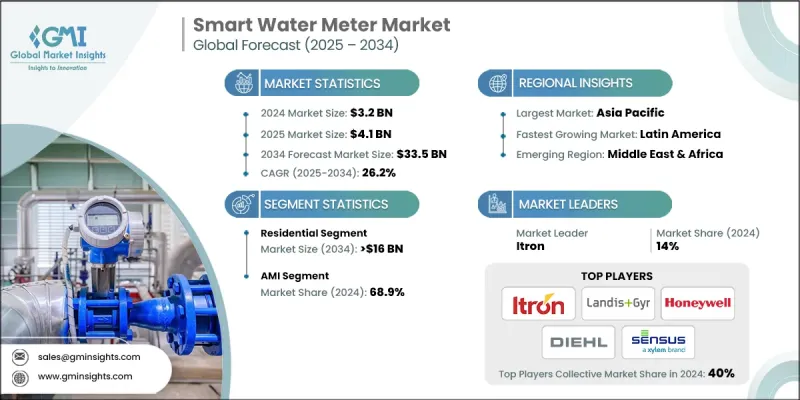

2024 年全球智慧水錶市場價值為 32 億美元,預計在即時資料需求和智慧城市計畫擴展的推動下,該市場將以 26.2% 的複合年成長率成長,到 2034 年達到 335 億美元。根據聯合國的報告,到 2050 年,城市地區預計將容納全球 68% 的人口,這凸顯了對高效水管理系統的需求。即時資料可實現精確監測、快速檢測問題和最佳化水管理,從而提高營運效率和資源節約。隨著智慧城市計畫的激增,將智慧水錶整合到城市基礎設施中對於改善整體水管理和基礎設施連接至關重要。對先進資料解決方案和智慧技術整合的日益重視推動了市場擴張和各個領域的應用。

例如,2024年6月,萊森推出了一款支援Sigfox的智慧水錶,旨在滿足市場對先進水管理解決方案日益成長的需求。 Sigfox技術的整合增強了連接和資料傳輸能力,滿足了可靠即時監控的需求。這項創新反映了市場向先進互聯系統發展的趨勢,並支援智慧水錶在各個領域的更廣泛應用。智慧水錶產業根據應用、技術、產品和地區細分。到2032年,商業領域將大幅成長,這歸因於企業和產業對精確用水監控的高需求。商業機構需要精確的水管理來最佳化營運效率、降低成本並遵守監管要求。智慧水錶提供即時資料、洩漏檢測和自動計費,使其成為大型用水用戶的理想選擇。商業應用中對高效水資源管理的需求推動了智慧水錶的廣泛應用,鞏固了該領域的主導市場地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 32億美元 |

| 預測值 | 335億美元 |

| 複合年成長率 | 26.2% |

到2032年,熱水錶市場將獲得顯著成長,這得益於住宅、商業和工業環境中對熱水使用情況的精確監控需求日益成長。準確測量熱水消耗有助於最佳化能源使用、降低成本並確保高效的資源管理。智慧熱水錶整合先進技術,可實現即時資料收集並提高計費準確性。對高效能熱水管理解決方案日益成長的需求推動了該市場在市場中的主導地位。到2032年,亞太地區智慧水錶市場佔有率將維持中等複合年成長率,這得益於快速的城市化、人口成長和水資源短缺問題日益嚴重。該地區各國政府正在大力投資智慧基礎設施,以改善水資源管理和效率。智慧城市計畫的日益普及和物聯網技術的進步進一步推動了市場的發展。住宅和商業領域對精確用水監控的高需求使亞太地區成為全球智慧水錶產業的核心貢獻者。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 進出口貿易分析

- 各地區價格趨勢分析(美元/單位)

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 新興機會和趨勢

- 數位化和物聯網整合

- 新興市場滲透

- 投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分析公司市場佔有率

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 競爭性基準描述

- 策略儀表板

- 創新與技術格局

第5章:市場規模與預測:按應用,2021 - 2034

- 主要趨勢

- 住宅

- 商業的

- 公用事業

第6章:市場規模及預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 急性心肌梗塞

- 抗腫瘤藥物

第7章:市場規模及預測:依產品,2021 - 2034

- 主要趨勢

- 熱水錶

- 冷水錶

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 瑞典

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- ABB

- Apator SA

- Arad Group:

- Badger Meter, Inc.

- BMETERS Srl

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Itron Inc.

- Kamstrup

- Landis+Gyr

- Neptune Technology Group Inc.

- Ningbo Water Meter Co., Ltd.

- Schneider Electric

- Siemens

- Sontex SA

- Xylem (Sensus)

- ZENNER International GmbH & Co. KG

- Suez

- Baylan Water Meters

- BOVE Technology

The Global Smart Water Meter Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 26.2% to reach USD 33.5 billion by 2034, driven by the demand for real-time data and the expansion of smart city initiatives. According to a report by the United Nations, urban areas are expected to house 68% of the world's population by 2050, highlighting the need for efficient water management systems. Real-time data allows for precise monitoring, quick detection of issues, and optimized water management, enhancing operational efficiency and resource conservation. As smart city projects proliferate, integrating smart water meters into urban infrastructure becomes crucial for improving overall water management and infrastructure connectivity. This growing emphasis on advanced data solutions and smart technology integration fuels market expansion and adoption across various sectors.

For instance, in June 2024, LAISON introduced a Sigfox-enabled smart water meter designed to meet the increasing demand for advanced water management solutions in the market. The integration of Sigfox technology enhances connectivity and data transmission capabilities, catering to the need for reliable real-time monitoring. This innovation reflects the market trend towards advanced, connected systems and supports the broader adoption of smart water meters across various sectors. The smart water meter industry is fragmented based on application, technology, product, and region. The commercial segment will see a considerable surge by 2032, attributed to the high demand for accurate water usage monitoring in businesses and industries. Commercial establishments require precise water management to optimize operational efficiency, reduce costs, and comply with regulatory requirements. Smart water meters offer real-time data, leak detection, and automated billing, making them ideal for large-scale water consumers. The need for efficient water resource management in commercial applications drives significant adoption, solidifying this segment's dominant market position.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $33.5 Billion |

| CAGR | 26.2% |

The hot water meter segment will garner remarkable gains by 2032, fueled by the rising need for precise monitoring of hot water usage in residential, commercial, and industrial settings. Accurate measurement of hot water consumption helps optimize energy usage, reduce costs, and ensure efficient resource management. The integration of advanced technologies in smart hot water meters allows for real-time data collection and improved billing accuracy. This growing demand for effective hot water management solutions drives the dominance of this segment in the market. Asia Pacific smart water meter market share will secure a moderate CAGR through 2032, owing to rapid urbanization, increasing population, and rising water scarcity issues. Governments in the region are investing heavily in smart infrastructure to improve water management and efficiency. The growing adoption of smart city initiatives and advancements in IoT technology further drive the market. High demand for accurate water usage monitoring in both residential and commercial sectors positions APAC as a central contributor to the global smart water meter industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Import/Export trade analysis

- 3.4 Price trend analysis, by region (USD/Unit)

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Utility

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 AMI

- 6.3 AMR

Chapter 7 Market Size and Forecast, By Product, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Hot water meter

- 7.3 Cold water meter

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.5.4 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Apator S.A.

- 9.3 Arad Group:

- 9.4 Badger Meter, Inc.

- 9.5 BMETERS S.r.l

- 9.6 Diehl Stiftung & Co. KG

- 9.7 Honeywell International Inc.

- 9.8 Itron Inc.

- 9.9 Kamstrup

- 9.10 Landis+Gyr

- 9.11 Neptune Technology Group Inc.

- 9.12 Ningbo Water Meter Co., Ltd.

- 9.13 Schneider Electric

- 9.14 Siemens

- 9.15 Sontex SA

- 9.16 Xylem (Sensus)

- 9.17 ZENNER International GmbH & Co. KG

- 9.18 Suez

- 9.19 Baylan Water Meters

- 9.20 BOVE Technology

智慧水錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

智慧水錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球漏水檢測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球漏水檢測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本智慧水錶市場報告:按產品類型、水錶類型、配置類型、組件、應用和地區分類(2026-2034年)

日本智慧水錶市場報告:按產品類型、水錶類型、配置類型、組件、應用和地區分類(2026-2034年) 全球智慧水務市場:預測至2032年-按組件、部署方式、解決方案、最終用戶和地區進行分析

全球智慧水務市場:預測至2032年-按組件、部署方式、解決方案、最終用戶和地區進行分析 全球漏水檢測系統市場

全球漏水檢測系統市場 漏水檢測系統市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、技術、最終用戶、地區和競爭細分,2020-2030 年)

漏水檢測系統市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、技術、最終用戶、地區和競爭細分,2020-2030 年) 全球智慧水錶市場:市場規模、市場佔有率、趨勢分析(按技術、儀表類型、應用和地區)、展望和未來預測(2025-2032 年)

全球智慧水錶市場:市場規模、市場佔有率、趨勢分析(按技術、儀表類型、應用和地區)、展望和未來預測(2025-2032 年) 智慧水錶市場規模、佔有率、趨勢分析報告:按水錶類型、技術、應用、地區、細分市場預測,2025-2030 年全球智慧水錶市場:市場規模(按類型、組件、應用和地區分類)、未來預測

智慧水錶市場規模、佔有率、趨勢分析報告:按水錶類型、技術、應用、地區、細分市場預測,2025-2030 年全球智慧水錶市場:市場規模(按類型、組件、應用和地區分類)、未來預測 水循環淋浴設備市場分析及預測(至2034年):類型、產品、服務、技術、組件、應用、材料類型、安裝類型、解決方案

水循環淋浴設備市場分析及預測(至2034年):類型、產品、服務、技術、組件、應用、材料類型、安裝類型、解決方案