|

市場調查報告書

商品編碼

1822568

電池模擬軟體市場機會、成長動力、產業趨勢分析及2025-2034年預測Battery Simulation Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

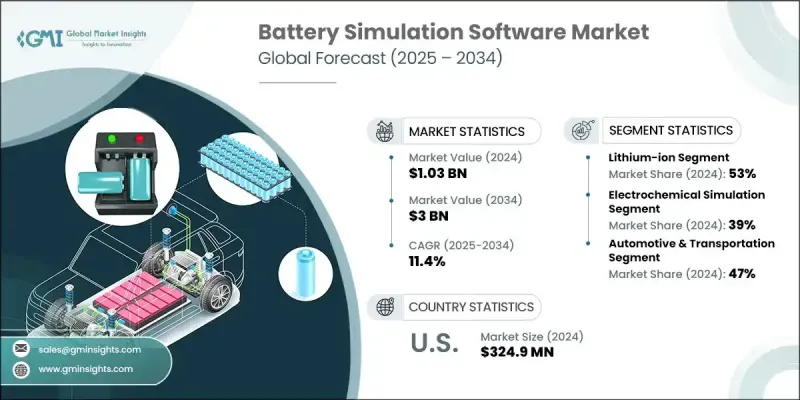

2024 年全球電池模擬軟體市場價值為 10.3 億美元,預計將以 11.4% 的複合年成長率成長,到 2034 年達到 30 億美元。

這一成長反映出,為了因應電動車和電網規模儲能需求的激增,人們正更廣泛地尋求更智慧、更具成本效益和更節能的電池系統。模擬軟體提供了強大的工具集,可模擬電池行為、簡化設計並最佳化效能,同時最大限度地減少昂貴的實體原型製作。汽車製造商和能源解決方案供應商擴大利用模擬來提高電池安全性、延長續航里程並符合不斷發展的儲能法規。隨著再生能源被納入國家電網,需要可靠的儲能系統來支援負載平衡、降低尖峰壓力並穩定供應。電池模擬平台對於實現這些目標至關重要,尤其是在電網營運商和公用事業供應商擴大智慧能源基礎設施規模的情況下。新冠疫情等疫情導致實驗室訪問受限和出行限制,迫使企業轉向遠端設計和虛擬測試,從而加速了數位化工程的轉型。如今,企業依靠混合雲端環境、數位孿生系統和經過驗證的虛擬模型來推進電池技術開發並縮短創新週期。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 10.3億美元 |

| 預測值 | 30億美元 |

| 複合年成長率 | 11.4% |

鋰離子電池市場在2024年佔據了53%的市場佔有率,預計到2034年將維持11%的複合年成長率。鋰離子電池憑藉其高能量密度、長循環壽命和高效的性能特點,仍然是電動車、電網能源系統和行動電子設備最主要的選擇。模擬軟體使開發人員能夠透過對熱行為、電化學反應和充放電循環進行預測建模來改進鋰離子電池的設計。這些工具在提高電池壽命和系統可靠性方面也發揮著至關重要的作用。隨著電動車和清潔能源產業的不斷擴張,模擬為創新提供了必要的基礎,確保這些電池滿足日益嚴格的性能和安全基準。

電化學模擬領域在2024年佔據了39%的市場佔有率,預計2025年至2034年的複合年成長率將達到11%。該領域因其能夠在分子層面模擬電池化學和內部過程而脫穎而出。它使製造商能夠在物理試驗之前評估離子動力學、充電行為和反應機制,從而加快開發速度並提高成本效益。電化學建模對於改進電池結構、最佳化電極材料和調整電解質成分至關重要。這種模擬類型有助於深入了解電池在各種工作條件下的性能,這對於安全性和耐用性至關重要的應用(例如電動車和航太系統)至關重要。

2024年,美國電池模擬軟體產業佔85%的市場佔有率,產值達3.249億美元。美國電池模擬產業受益於其成熟的技術生態系統、先進的運算基礎設施以及為模擬工作負載提供可擴展環境的雲端服務供應商的強大影響力。對多物理場、高保真模擬模型的需求正在成長,尤其是在電動車製造商、航太公司和清潔能源新創公司。美國在研發投資和數位工程轉型方面也處於領先地位,使企業能夠透過基於雲端的建模平台降低實體原型製作成本並縮短產品上市時間。

全球電池模擬軟體產業的知名企業包括達梭、ESI、西門子、COMSOL、AVL List、MathWorks、Autodesk、Ansys 和 Altair Engineering。為了鞏固市場地位,電池模擬軟體領域的公司將創新、協作和雲端整合放在首位。各公司正透過投資適應實際電池使用條件的 AI 增強建模工具來提高模擬精度。許多企業正在與原始設備製造商 (OEM)、電池開發商和學術機構建立合作夥伴關係,以開發專有演算法並共同開發行業特定的應用程式。他們非常注重提供混合部署選項(基於雲端和本地),以滿足不同 IP 敏感度等級的需求。領先的供應商還在改進使用者介面、減少模擬運行時間並支援多物理環境,以吸引更多企業用戶。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 電動車(EV)的普及率不斷上升

- 增加對再生能源儲存的投資

- 電池化學技術進步

- 人工智慧與雲端運算在模擬中的融合

- 產業陷阱與挑戰

- 初始投資高且軟體複雜

- 數據可用性和模型準確性挑戰

- 市場機會

- 新興市場的擴張

- 與電池製造商和原始設備製造商合作

- 與數位孿生和物聯網技術的整合

- 下一代電池的客製化

- 成長動力

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利分析

- 定價趨勢與經濟分析

- 用例

- 單元級設計與最佳化

- 模組和包級整合

- 系統級性能和整合

- 生命週期和退化分析

- 最佳情況

- 投資前景和資金分析

- 全球電池產業投資趨勢

- 模擬軟體投資與研發支出

- 區域投資模式和政府支持

- 技術轉移和商業化

- 成本效益分析

- 軟體實施成本結構

- 營運效益和價值創造

- 策略利益和競爭優勢

- 投資報酬率分析和回報評估

- 永續性和環境影響分析

- 生命週期評估與環境建模

- 永續設計與最佳化

- 環境合規與報告

- 綠色科技與創新

- 未來技術路線圖與創新時間表

- 模擬技術演進(2024-2034)

- 電池技術整合與改造

- 技術融合與平台演進

- 市場演變與顛覆情景

- 品質保證和驗證框架

- 模型驗證和確認

- 軟體品質保證

- 法規遵從性和文檔

- 持續改進和創新

- 技術整合和工作流程最佳化

- CAD 和設計工具整合

- PLM 和資料管理整合

- 製造和測試整合

- 數位孿生和物聯網整合

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依電池類型,2021 - 2034

- 主要趨勢

- 鋰離子

- 鉛酸電池

- 固態

- 其他

第6章:市場估計與預測:透過模擬,2021 - 2034

- 主要趨勢

- 電化學模擬

- 熱模擬

- 結構和機械模擬

- 電氣和電路模擬

- 其他

第7章:市場估計與預測:依部署模式,2021 - 2034

- 主要趨勢

- 本地部署

- 雲

- 混合

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 汽車與運輸

- 消費性電子產品

- 儲能系統

- 工業設備

第9章:市場估計與預測:依企業分類,2021 - 2034 年

- 主要趨勢

- 中小企業

- 大型企業

第 10 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- OEM

- 電池製造商

- 研究與開發組織

- 大學和學術機構

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 全球參與者

- Ansys

- Siemens

- Altair Engineering

- MathWorks

- Dassault Systemes

- AVL List GmbH

- ESI Group

- Ricardo

- Intertek Group

- Hexagon

- Synopsys

- COMSOL

- dSPACE

- Gamma Technologies

- 區域參與者

- OpenCFD

- TWAICE Technologies GmbH

- Batemo

- Maplesoft

- ThermoAnalytics

- Shenzhen Finite Element Technology

- Suzhou Yilaikede Technology

- Mid-Atlantic Power Specialists

- UK Battery Industrialization Centre

- 新興玩家

- Battery Design LLC

- BATEMO GmbH

- Keysight Technologies

- Gamma Technologies

- AVL List GmbH

- Cadmus Group

- Electrochemical Engine Simulation

The Global Battery Simulation Software Market was valued at USD 1.03 billion in 2024 and is estimated to grow at a CAGR of 11.4% to reach USD 3 billion by 2034.

This growth reflects a broader push toward smarter, cost-effective, and energy-efficient battery systems in response to surging demand for electric vehicles and grid-scale energy storage. Simulation software offers a powerful toolset to model battery behavior, streamline design, and optimize performance while minimizing costly physical prototyping. Automakers and energy solution providers are increasingly leveraging simulation to enhance battery safety, extend range, and align with evolving energy storage regulations. With renewable energy sources being added to national grids, there's a need for dependable storage that supports load balancing, reduces peak pressure, and stabilizes supply. Battery simulation platforms are emerging as essential to meeting these goals, especially as grid operators and utility providers scale up smart energy infrastructure. The transition to digital engineering has been accelerated by disruptions like the COVID-19 pandemic, where limited access to labs and travel restrictions drove enterprises toward remote design and virtual testing. Companies now rely on hybrid cloud environments, digital twin systems, and validated virtual models to advance battery technology development and shorten innovation cycles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.03 Billion |

| Forecast Value | $3 Billion |

| CAGR | 11.4% |

The lithium-ion battery segment held 53% share in 2024 and is projected to maintain a CAGR of 11% through 2034. Lithium-ion batteries remain the most prominent choice for electric vehicles, grid energy systems, and mobile electronics due to their high energy density, long cycle life, and efficient performance characteristics. Simulation software enables developers to improve lithium-ion battery design through predictive modeling of thermal behavior, electrochemical reactions, and charge-discharge cycles. These tools also play a vital role in improving battery longevity and system reliability. As electric mobility and clean energy sectors continue to scale, simulation provides a necessary foundation for innovation, ensuring these batteries meet increasingly rigorous performance and safety benchmarks.

The electrochemical simulation segment captured 39% share in 2024 and is anticipated to grow at a CAGR of 11% from 2025 to 2034. This segment stands out due to its capacity to simulate battery chemistry and internal processes at the molecular level. It allows manufacturers to evaluate ion dynamics, charging behavior, and reaction mechanisms before physical trials, making development faster and more cost-effective. Electrochemical modeling is essential for refining battery architecture, optimizing electrode materials, and tailoring electrolyte composition. This simulation type supports deeper insights into performance under variable operating conditions, which is crucial for applications where safety and durability are mission-critical, including electric vehicles and aerospace systems.

United States Battery Simulation Software Industry held an 85% share in 2024, generating USD 324.9 million. The country's battery simulation sector benefits from its mature tech ecosystem, access to advanced computing infrastructure, and a strong presence of cloud service providers offering scalable environments for simulation workloads. The demand for multi-physics, high-fidelity simulation models is growing, particularly among EV manufacturers, aerospace companies, and clean energy startups. The US also leads in R&D investment and digital engineering transformation, enabling companies to reduce physical prototyping costs and shorten time-to-market through cloud-enabled modeling platforms.

Notable players in the Global Battery Simulation Software Industry include Dassault, ESI, Siemens, COMSOL, AVL List, MathWorks, Autodesk, Ansys, and Altair Engineering. To solidify their market position, companies in the battery simulation software sector are prioritizing innovation, collaboration, and cloud integration. Firms are advancing simulation accuracy by investing in AI-enhanced modeling tools that adapt to real-world battery usage conditions. Many players are forming partnerships with OEMs, battery developers, and academic institutions to develop proprietary algorithms and co-develop industry-specific applications. There's a strong focus on offering hybrid deployment options-cloud-based and on-premises-catering to varying IP sensitivity levels. Leading providers are also improving user interfaces, reducing simulation runtimes, and supporting multi-physics environments to attract more enterprise users.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery Type

- 2.2.3 Simulation

- 2.2.4 Application

- 2.2.5 Enterprises

- 2.2.6 Deployment mode

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of electric vehicles (EVs)

- 3.2.1.2 Increasing investment in renewable energy storage

- 3.2.1.3 Technological advancements in battery chemistry

- 3.2.1.4 Integration of AI and cloud computing in simulation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and software complexity

- 3.2.2.2 Data availability and model accuracy challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Collaboration with battery manufacturers and OEMs

- 3.2.3.3 Integration with digital twin and IoT technologies

- 3.2.3.4 Customization for next-generation batteries

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Pricing trends and economic analysis

- 3.9 Use cases

- 3.9.1 Cell-level design and optimization

- 3.9.2 Module and pack-level integration

- 3.9.3 System-level performance and integration

- 3.9.4 Lifecycle and degradation analysis

- 3.10 Best-case scenario

- 3.11 Investment landscape and funding analysis

- 3.11.1 Global battery industry investment trends

- 3.11.2 Simulation software investment and R&D spending

- 3.11.3 Regional investment patterns and government support

- 3.11.4 Technology transfer and commercialization

- 3.12 Cost-benefit analysis

- 3.12.1 Software implementation cost structure

- 3.12.2 Operational benefits and value creation

- 3.12.3 Strategic benefits and competitive advantage

- 3.12.4 ROI analysis and payback assessment

- 3.13 Sustainability and environmental impact analysis

- 3.13.1 Lifecycle assessment and environmental modeling

- 3.13.2 Sustainable design and optimization

- 3.13.3 Environmental compliance and reporting

- 3.13.4 Green technology and innovation

- 3.14 Future technology roadmap and innovation timeline

- 3.14.1 Simulation technology evolution (2024-2034)

- 3.14.2 Battery technology integration and adaptation

- 3.14.3 Technology convergence and platform evolution

- 3.14.4 Market evolution and disruption scenarios

- 3.15 Quality assurance and validation framework

- 3.15.1 Model validation and verification

- 3.15.2 Software quality assurance

- 3.15.3 Regulatory compliance and documentation

- 3.15.4 Continuous improvement and innovation

- 3.16 Technology integration and workflow optimization

- 3.16.1 CAD and design tool integration

- 3.16.2 PLM and data management integration

- 3.16.3 Manufacturing and testing integration

- 3.16.4 Digital twin and IOT integration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Battery type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Lithium-Ion

- 5.3 Lead-Acid

- 5.4 Solid-State

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Simulation, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Electrochemical simulation

- 6.3 Thermal simulation

- 6.4 Structural & mechanical simulation

- 6.5 Electrical & circuit simulation

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-Premise

- 7.3 Cloud

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Automotive & transportation

- 8.3 Consumer electronics

- 8.4 Energy storage systems

- 8.5 Industrial equipment

Chapter 9 Market Estimates & Forecast, By Enterprises, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 SME

- 9.3 Large Enterprises

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Battery manufacturers

- 10.4 Research & development organizations

- 10.5 Universities & academic institutions

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Ansys

- 12.1.2 Siemens

- 12.1.3 Altair Engineering

- 12.1.4 MathWorks

- 12.1.5 Dassault Systemes

- 12.1.6 AVL List GmbH

- 12.1.7 ESI Group

- 12.1.8 Ricardo

- 12.1.9 Intertek Group

- 12.1.10 Hexagon

- 12.1.11 Synopsys

- 12.1.12 COMSOL

- 12.1.13 dSPACE

- 12.1.14 Gamma Technologies

- 12.2 Regional Players

- 12.2.1 OpenCFD

- 12.2.2 TWAICE Technologies GmbH

- 12.2.3 Batemo

- 12.2.4 Maplesoft

- 12.2.5 ThermoAnalytics

- 12.2.6 Shenzhen Finite Element Technology

- 12.2.7 Suzhou Yilaikede Technology

- 12.2.8 Mid-Atlantic Power Specialists

- 12.2.9 UK Battery Industrialization Centre

- 12.3 Emerging Players

- 12.3.1 Battery Design LLC

- 12.3.2 BATEMO GmbH

- 12.3.3 Keysight Technologies

- 12.3.4 Gamma Technologies

- 12.3.5 AVL List GmbH

- 12.3.6 Cadmus Group

- 12.3.7 Electrochemical Engine Simulation

全球電池模擬軟體市場規模調查與預測:按電池類型、模擬、應用、部署模式、企業、最終用途和地區分類的預測(2026-2035 年)

全球電池模擬軟體市場規模調查與預測:按電池類型、模擬、應用、部署模式、企業、最終用途和地區分類的預測(2026-2035 年) 電池 CAE 軟體市場(按軟體類型、電池類型、部署模式、應用和最終用戶產業分類)—2026-2032 年全球預測電池建模與模擬軟體市場(按軟體類型、電池類型、部署模式、應用和最終用戶產業分類),全球預測(2026-2032年)

電池 CAE 軟體市場(按軟體類型、電池類型、部署模式、應用和最終用戶產業分類)—2026-2032 年全球預測電池建模與模擬軟體市場(按軟體類型、電池類型、部署模式、應用和最終用戶產業分類),全球預測(2026-2032年) 電池模擬軟體市場,規模,佔有率,趨勢,產業報告:電池類別,模擬類別,各最終用途產業,各地區,2025年~2034年的市場預測

電池模擬軟體市場,規模,佔有率,趨勢,產業報告:電池類別,模擬類別,各最終用途產業,各地區,2025年~2034年的市場預測 電池模擬軟體市場:全球按類比類型、電池類型、最終用途產業和地區分類 - 預測至 2030 年

電池模擬軟體市場:全球按類比類型、電池類型、最終用途產業和地區分類 - 預測至 2030 年