|

市場調查報告書

商品編碼

1822554

軍用防護眼鏡市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Military Protective Eyewear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

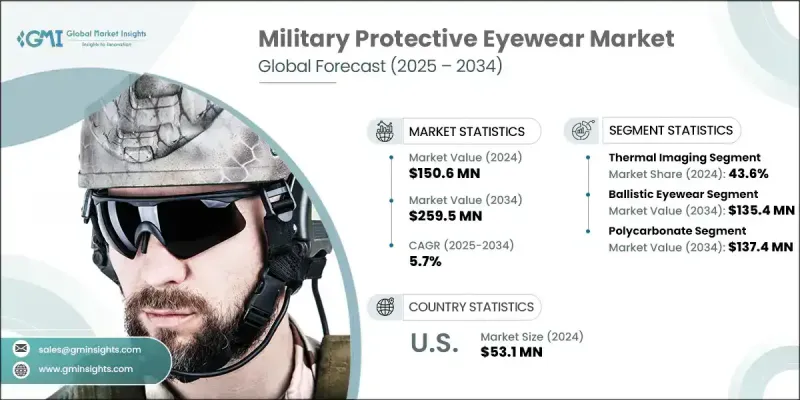

2024 年全球軍用防護眼鏡市場價值為 1.506 億美元,預計到 2034 年將以 5.7% 的複合年成長率成長至 2.595 億美元。

各國軍事預算的不斷成長,以及擴增實境等智慧技術日益融入作戰系統,是推動市場需求的關鍵因素。軍事組織越來越重視士兵安全和戰備狀態,從而更加重視先進眼鏡。採購模式正朝著長期合作夥伴關係發展,優先考慮防護眼鏡系統的生命週期成本效益、持續性能和持續研發。武裝部隊正在與私人科技開發商合作,透過聯合專案推動創新,尤其是在下一代戰術光學元件領域。人們對積層製造和快速成型技術的興趣也日益濃厚,這些技術能夠在移動野外環境中按需生產眼鏡零件。這些進步正在重塑物流戰略,預計到未來十年將成為未來作戰的核心,尤其是在特種部隊中。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.506億美元 |

| 預測值 | 2.595億美元 |

| 複合年成長率 | 5.7% |

2024年,熱成像系統佔了43.6%的市場。在夜間任務、偵察和目標追蹤等需要在弱光或遮蔽條件下保持可見性的行動中,熱光學的應用日益增加。為了減小組件的尺寸和重量,開發人員正在研發可與頭盔和支援AR的頭飾整合的緊湊型熱成像模組。製造商被鼓勵創新輕量化的熱成像裝置,以保持低功耗並與平視顯示器無縫合作。這些增強型系統正成為精英作戰部隊的必備工具,他們需要高效的、技術驅動的現場視野,同時又不影響長時間任務中的舒適度或電池性能。

2034年,防彈眼鏡市場規模將達到1.354億美元。由於在現役戰區中,人們日益頻繁地接觸高速威脅、爆炸碎片和敵方彈,該市場的需求正在成長。更輕的鏡框設計、模組化的佩戴方式以及升級的抗衝擊鏡片,都提升了產品的吸引力。符合最新的軍事和安全認證標準,有助於推動產品在全球國防部隊的部署。 MIL-PRF和ANSI Z87.1+等標準的廣泛實施正在各國防機構加速推進。為了保持競爭優勢,該領域的公司越來越注重開發可更換鏡片平台,並努力實現高等級的抗衝擊合規性,以贏得多年的政府供應合約。

2024年,北美軍用防護眼鏡市場佔據42.4%的市場佔有率,預計到2034年將以6.7%的複合年成長率成長。強大的國防支出文化、強大的創新生態系統以及防護裝備領域的早期技術應用,使該地區保持了領先地位。國防現代化計畫和不斷變化的戰場需求正在推動先進防護光學元件的採購,包括抗雷射、防彈級和整合式擴增實境(AR)的眼鏡。該地區對作戰人員生存能力的關注,加上廣泛的研發支持,正在為下一代眼鏡奠定基礎,該眼鏡能夠在各種環境條件下增強態勢感知、即時瞄準和威脅緩解能力。

塑造全球軍用防護眼鏡市場格局的關鍵參與者包括霍尼韋爾、奧克利、Wiley X、3M 和 Revision Military。軍用防護眼鏡市場的領先公司正專注於多方面策略,以鞏固其市場地位。他們優先考慮研發投入,設計輕量化、模組化的系統,增強其彈道和光學性能,以滿足不斷發展的軍事行動的特定需求。一些公司正在遵守政府採購協議和認證,以確保獲得高價值的長期國防合約。與技術合作夥伴的策略合作也使得擴增實境、熱成像和抬頭顯示系統能夠整合到眼鏡中。各公司正在透過建立供應鏈中心和區域製造部門來擴大其在高支出地區的業務,以確保持續交付。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 全球國防開支不斷上升

- 軍事現代化和裝備升級

- 擴增實境與智慧眼鏡系統的整合

- 採用輕量化和人體工學設計

- 執法和準軍事部隊的採購量不斷增加

- 產業陷阱與挑戰

- 高級防護眼鏡成本高

- 發展中國家的預算限制

- 市場機會

- 融入士兵現代化計劃

- 執法和國土安全的需求不斷成長

- 材料科學與鏡頭技術的進步

- 更加重視雷射和輻射眼部保護

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 防彈眼鏡

- 雷射防護眼鏡

- 化學和生物防護眼鏡

- 夜視相容眼鏡

- 標準防護眼鏡

- 其他

第6章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 石英

- 聚碳酸酯

- 玻璃纖維

- 藍寶石

- 其他

第7章:市場估計與預測:按技術分類,2021 - 2034 年

- 主要趨勢

- 熱成像

- 影像增強器

第 8 章:市場估計與預測:按最終用途應用,2021 - 2034 年

- 主要趨勢

- 砲手瞄準具

- 海軍追蹤器

- 駕駛視線

- 步兵武器瞄準具

- 其他

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球關鍵參與者

- 3M

- Honeywell International

- Oakley

- Revision Military

- Wiley X

- 區域關鍵參與者

- 北美洲

- ESS Eyewear

- Gentex

- Smith Optics

- 歐洲

- BAE Systems

- Bolle Safety

- Thales

- 亞太地區

- Bharat Electronics

- Day Sun Industrial

- Univet Optical Technologies

- 北美洲

- 利基市場參與者/顛覆者

- Elbit Systems

- Kentek

- Meopta

- NoIR Laser

- Philips Safety Products

- Uvex Safety Group

The Global Military Protective Eyewear Market was valued at USD 150.6 million in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 259.5 million by 2034.

Rising military budgets across nations and increasing integration of smart technologies such as augmented reality into combat systems are key factors driving market demand. Military organizations are placing higher importance on soldier safety and operational readiness, leading to increased focus on advanced eyewear. Procurement patterns are evolving toward long-term partnerships that prioritize lifecycle cost-efficiency, sustained performance, and continuous R&D in protective eyewear systems. Armed forces are collaborating with private tech developers to advance innovations via joint programs, especially for next-gen tactical optics. There's also a rising interest in additive manufacturing and rapid prototyping techniques, enabling on-demand creation of eyewear parts in mobile field environments. These advancements are reshaping logistics strategies and are expected to become central to future operations, particularly among special forces, by the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $150.6 Million |

| Forecast Value | $259.5 Million |

| CAGR | 5.7% |

The thermal imaging systems held a 43.6% share in 2024. The adoption of thermal optics is rising in operations requiring visibility in low-light or obscured conditions, such as night missions, reconnaissance, and target tracking. With a push to reduce the size and weight of components, developers are working on compact thermal modules that integrate with helmets and AR-enabled headgear. Manufacturers are encouraged to innovate lightweight thermal units that maintain low power consumption and work seamlessly with heads-up displays. These enhanced systems are becoming essential tools for elite combat units who require efficient, tech-enabled field vision without compromising comfort or battery performance during extended missions.

The ballistic protective eyewear segment will reach USD 135.4 million by 2034. This segment is witnessing higher uptake due to escalating exposure to high-velocity threats, blast debris, and hostile projectiles in active combat zones. Lighter frame designs, modular fit options, and upgraded lenses with high-impact resistance are all contributing to product appeal. Compliance with updated military and safety certification standards is helping drive product deployment across global defense forces. Widespread implementation of standards like MIL-PRF and ANSI Z87.1+ is accelerating across defense agencies. To retain a competitive edge, companies in this segment are increasingly focused on developing interchangeable lens platforms and working toward high-grade impact compliance to win multi-year government supply contracts.

North America Military Protective Eyewear Market held 42.4% share in 2024 and is expected to grow at a CAGR of 6.7% through 2034. A strong culture of defense spending, robust innovation ecosystems, and early tech adoption in protective gear have allowed the region to maintain leadership. Defense modernization initiatives and evolving battlefield requirements are pushing procurement of advanced protective optics, including laser-resistant, ballistic-grade, and AR-integrated eyewear. The region's focus on warfighter survivability, combined with extensive R&D support, is laying the groundwork for next-gen eyewear capable of enhancing situational awareness, real-time targeting, and threat mitigation under varied environmental conditions.

Key players shaping the Global Military Protective Eyewear Market landscape include Honeywell, Oakley, Wiley X, 3M, and Revision Military. Leading companies in the military protective eyewear market are focusing on multi-faceted strategies to solidify their presence. Prioritizing R&D investment, they are designing lightweight, modular systems with enhanced ballistic and optical capabilities to meet the specific needs of evolving military operations. Several firms are aligning with government procurement protocols and certifications to secure high-value, long-term defense contracts. Strategic collaborations with tech partners are also enabling the integration of AR, thermal, and HUD systems into eyewear. Companies are expanding their footprint in high-spending regions by establishing supply chain hubs and regional manufacturing units to ensure consistent delivery

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Material trends

- 2.2.3 Technology trends

- 2.2.4 End use application trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global defense expenditures

- 3.2.1.2 Military modernization and equipment upgrades

- 3.2.1.3 Integration of augmented reality and smart eyewear systems

- 3.2.1.4 Adoption of lightweight and ergonomic designs

- 3.2.1.5 Rising procurement from law enforcement and paramilitary forces

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of advanced protective eyewear

- 3.2.2.2 Budget constraints in developing nations

- 3.2.3 Market opportunities

- 3.2.3.1 Integration into soldier modernization programs

- 3.2.3.2 Growing demand from law enforcement and homeland security

- 3.2.3.3 Advancements in material science and lens technology

- 3.2.3.4 Increased focus on laser and radiation eye protection

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Ballistic eyewear

- 5.3 Laser protection eyewear

- 5.4 Chemical and biological protection eyewear

- 5.5 Night vision-compatible eyewear

- 5.6 Standard protective eyewear

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Quartz

- 6.3 Polycarbonate

- 6.4 Glass Fiber

- 6.5 Sapphire

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Thermal imaging

- 7.3 Image intensifier

Chapter 8 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Gunner sights

- 8.3 Naval trackers

- 8.4 Driving sights

- 8.5 Infantry weapon sight

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 3M

- 10.1.2 Honeywell International

- 10.1.3 Oakley

- 10.1.4 Revision Military

- 10.1.5 Wiley X

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 ESS Eyewear

- 10.2.1.2 Gentex

- 10.2.1.3 Smith Optics

- 10.2.2 Europe

- 10.2.2.1 BAE Systems

- 10.2.2.2 Bolle Safety

- 10.2.2.3 Thales

- 10.2.3 APAC

- 10.2.3.1 Bharat Electronics

- 10.2.3.2 Day Sun Industrial

- 10.2.3.3 Univet Optical Technologies

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Elbit Systems

- 10.3.2 Kentek

- 10.3.3 Meopta

- 10.3.4 NoIR Laser

- 10.3.5 Philips Safety Products

- 10.3.6 Uvex Safety Group