|

市場調查報告書

商品編碼

1822551

嬰兒孵化器市場機會、成長動力、產業趨勢分析及2025-2034年預測Infant Incubator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

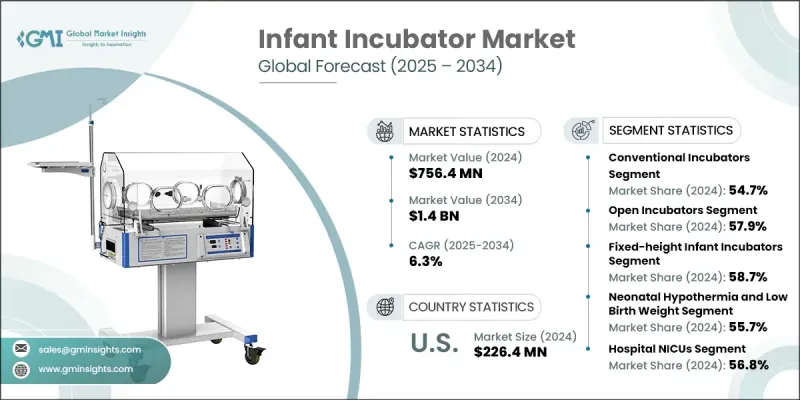

2024 年全球嬰兒孵化器市場價值為 7.564 億美元,預計將以 6.3% 的複合年成長率成長,到 2034 年達到 14 億美元。

早產率上升、降低新生兒死亡率的措施不斷加強以及新生兒護理技術的穩定進步,共同推動市場的成長。此外,已開發國家和發展中國家新生兒加護病房的擴建和現代化建設,也顯著提升了對高性能嬰兒培養箱的需求。這些培養箱為脆弱的新生兒提供了一個精心調控的環境,幫助他們發育和康復,在保護其免受外界干擾的同時,確保溫度、濕度和氧氣水平達到最佳控制。隨著各國政府和衛生組織持續投資新生兒健康基礎設施,包含遠端監控和物聯網連接等功能的先進模式正在加速普及。醫療保健系統的持續升級,尤其是在新興地區,加上人們對嬰兒健康需求的認知不斷提高,以及更先進護理設備的普及,預計將在未來幾年推動市場向前發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.564億美元 |

| 預測值 | 14億美元 |

| 複合年成長率 | 6.3% |

2024年,傳統恆溫箱市場佔54.7%的佔有率。這些系統因其可靠性、有效性以及與新技術相比相對較低的成本,仍在新生兒加護病房(NICU)廣泛使用。無論資源豐富或匱乏,醫院都仍然嚴重依賴傳統恆溫箱,以確保為早產兒提供一個穩定且支持性的環境。它們能夠維持新生兒生存所必需的穩定環境條件,使其成為婦產科醫院重症監護的重要組成部分。因此,預計它們將在整個預測期內佔據市場主導地位,尤其是在預算有限、無法採用更先進恆溫箱的醫療機構。

2024年,開放式恆溫箱市場佔有57.9%的佔有率。開放式恆溫箱以其便捷易用、價格實惠且相容於多種監測設備而聞名,在許多臨床環境中仍然是首選。這些設備通常被稱為輻射加溫器,利用頂部熱量來維持嬰兒體溫,同時方便嬰兒進行緊急干預或常規護理。雖然開放式恆溫箱缺乏封閉式系統那樣的全面環境控制,但其開放式設計使護理人員能夠快速回應醫療需求。這使得它們特別適用於需要便捷通道的高風險病例。開放式恆溫箱在醫院中的受歡迎程度也得益於其較低的維護要求以及在產後即時護理中經過驗證的臨床效果。

2024年,美國嬰兒培養箱市場規模達到2.264億美元,其成長動力源自於新生兒照護投資的增加、保險支持以及早產病例的上升。這項成長得益於先進的醫療基礎設施、持續成長的研發活動,以及將創新嬰兒護理技術融入新生兒加護病房(NICU)環境的廣泛推動。該地區還受益於健全的監管框架和強大的報銷網路,這些因素正在推動公立和私立醫院加快採用更智慧、更安全的培養箱系統。

活躍於嬰兒培養箱市場的主要公司包括 GE HealthCare、Dragerwerk、Koninklijke Philips、Stryker、Natus Medical 和 Inspiration Healthcare Group。嬰兒培養箱市場的公司專注於創新、合規和合作夥伴關係,以加強其全球影響力。許多公司正在投資研究,設計配備智慧感測器、即時監控和基於物聯網的連接功能的培養箱,以滿足現代新生兒重症監護室 (NICU) 不斷變化的需求。與醫院和醫療保健系統的策略合作有助於製造商根據特定的臨床需求量身定做產品,而與當地分銷商的合作則使其更容易進入新興地區。各公司也正在努力滿足國際安全和性能認證,以提高信任度和採用率。產品組合擴展到包括運輸培養箱、混合系統和全數位化平台,使參與者能夠應對多種護理環境。成本效益、病患安全和臨床結果仍然是保持市場領先地位的關鍵關注領域。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 全球早產數量不斷增加

- 政府加強新生兒護理力度

- 新生兒護理的技術進步

- 產業陷阱與挑戰

- 先進孵化器成本高

- 服務和維護挑戰

- 市場機會

- 混合孵化器的採用日益增多

- 關注新興經濟體的新生兒健康

- 成長動力

- 成長潛力分析

- 監管格局

- 技術進步

- 當前的技術趨勢

- 新興技術

- 供應鏈分析

- 報銷場景

- 2024年定價分析

- 北美洲

- 歐洲

- 亞太地區

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 常規孵化器

- 混合孵化器

- 運輸孵化器

第6章:市場估計與預測:按類型,2021 - 2034

- 主要趨勢

- 開放式(輻射加熱器)

- 關閉

第7章:市場估計與預測:按模式,2021 - 2034

- 主要趨勢

- 固定高度嬰兒培養箱

- 高度可調的嬰兒培養箱

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 新生兒體溫過低和低出生體重

- 黃疸

- 其他應用

第9章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- 醫院新生兒加護病房

- 產婦護理中心

- 緊急醫療服務

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- Dragerwerk

- GE HealthCare

- Inspiration Healthcare Group

- Koninklijke Philips

- Natus Medical

- Stryker

- 區域參與者

- Atom Medical

- Avante Health Solutions

- Bistos

- Fanem

- International Biomedical

- MEDICOR Elektronika

- 新興企業

- JW Pharmaceutical

- Narang Medical

- NOVOS

The Global Infant Incubator Market was valued at USD 756.4 million in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 1.4 billion by 2034.

Market growth is being propelled by a rise in premature births, increasing efforts to lower neonatal mortality rates, and steady progress in neonatal care technologies. Additionally, the expansion and modernization of neonatal intensive care units across developed and developing countries is significantly boosting demand for high-performance infant incubators. These incubators provide a carefully regulated environment to support the development and recovery of vulnerable newborns, offering protection from external disturbances while ensuring optimal control of temperature, humidity, and oxygen levels. As governments and health organizations continue to invest in neonatal health infrastructure, the adoption of advanced models that include features like remote monitoring and IoT connectivity is accelerating. Ongoing upgrades to healthcare systems, particularly in emerging regions, combined with rising awareness of infant health needs and the availability of more advanced care devices, are expected to push the market forward over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $756.4 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 6.3% |

In 2024, the conventional incubators segment accounted for a 54.7% share. These systems remain widely used across NICUs for their reliability, effectiveness, and relatively lower cost when compared with newer technologies. Hospitals in both high- and low-resource settings continue to depend heavily on conventional models to ensure a stable, supportive environment for premature infants. Their ability to maintain consistent environmental conditions essential for neonatal survival has made them an integral part of critical care in maternity hospitals. As a result, they are expected to hold a dominant share of the market throughout the forecast period, particularly in facilities where budget constraints limit the adoption of more advanced models.

The open incubators segment held a 57.9% share in 2024. Known for their ease of access, affordability, and compatibility with multiple monitoring devices, open incubators remain a top choice in many clinical environments. These devices, often referred to as radiant warmers, use overhead heat to maintain infant body temperature while keeping the baby accessible for emergency intervention or routine care. Though they lack the full environmental control of closed systems, their open design allows caregivers to respond quickly to medical needs. This makes them particularly suitable for high-acuity cases where access is critical. Their popularity across hospitals is also supported by their lower maintenance requirements and proven clinical performance in immediate postnatal care.

United States Infant Incubator Market reached USD 226.4 million in 2024, with growth driven by increasing neonatal care investments, insurance support, and rising cases of preterm births. This progress is supported by a combination of advanced healthcare infrastructure, growing R&D activities, and a widespread push toward integrating innovative infant care technologies into NICU environments. The region also benefits from a robust regulatory framework and strong reimbursement networks, which are encouraging the faster adoption of smarter, safer incubator systems across both public and private hospitals.

Key companies active in the Infant Incubator Market include GE HealthCare, Dragerwerk, Koninklijke Philips, Stryker, Natus Medical, and Inspiration Healthcare Group. Companies in the infant incubator market are focusing on innovation, compliance, and partnerships to strengthen their global reach. Many are investing in research to design incubators equipped with smart sensors, real-time monitoring, and IoT-based connectivity to meet the evolving demands of modern NICUs. Strategic collaborations with hospitals and healthcare systems help manufacturers tailor their products for specific clinical needs, while partnerships with local distributors allow easier entry into emerging regions. Firms are also working to meet international safety and performance certifications to improve trust and adoption. Expansion of product portfolios to include transport incubators, hybrid systems, and fully digitized platforms enables players to address multiple care environments. Cost-efficiency, patient safety, and clinical outcomes remain key focus areas to maintain market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Modality trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of preterm births globally

- 3.2.1.2 Rising government initiatives for neonatal care

- 3.2.1.3 Technological advancements in neonatal care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced incubators

- 3.2.2.2 Service and maintenance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of hybrid incubators

- 3.2.3.2 Focus on neonatal health in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional incubator

- 5.3 Hybrid incubator

- 5.4 Transport incubator

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Open (radiant warmers)

- 6.3 Closed

Chapter 7 Market Estimates and Forecast, By Modality, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Fixed-height infant incubators

- 7.3 Height-adjustable infant incubators

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Neonatal hypothermia and low birth weight

- 8.3 Jaundice

- 8.4 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital NICU

- 9.3 Maternity care centers

- 9.4 Emergency medical services

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Dragerwerk

- 11.1.2 GE HealthCare

- 11.1.3 Inspiration Healthcare Group

- 11.1.4 Koninklijke Philips

- 11.1.5 Natus Medical

- 11.1.6 Stryker

- 11.2 Regional players

- 11.2.1 Atom Medical

- 11.2.2 Avante Health Solutions

- 11.2.3 Bistos

- 11.2.4 Fanem

- 11.2.5 International Biomedical

- 11.2.6 MEDICOR Elektronika

- 11.3 Emerging players

- 11.3.1 JW Pharmaceutical

- 11.3.2 Narang Medical

- 11.3.3 NOVOS