|

市場調查報告書

商品編碼

1822542

汽車區塊鏈技術市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Blockchain Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球汽車區塊鏈技術市場價值為 3 億美元,預計到 2034 年將以 29% 的複合年成長率成長至 37.7 億美元。

隨著汽車互聯互通和軟體驅動程度的不斷提升,汽車製造商在資料完整性、網路安全和即時通訊方面面臨日益成長的擔憂。區塊鏈提供了一個去中心化的防篡改系統,可以安全地追蹤和驗證車輛生命週期內的資料,涵蓋從製造、零件採購到軟體更新和所有權轉移的各個環節。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3億美元 |

| 預測值 | 37.7億美元 |

| 複合年成長率 | 29% |

公共區塊鏈日益普及

預計到2034年,公共區塊鏈領域將憑藉其無與倫比的透明度和去中心化架構獲得強勁發展。公共區塊鏈允許汽車製造商、監管機構、供應商和最終用戶等多個利益相關者即時存取和驗證資料,而無需依賴中央機構。這種模式對於車輛歷史記錄、所有權記錄和共享出行應用尤其有用。

解決方案的採用率不斷上升

2024年,汽車區塊鏈技術市場的解決方案部分佔據了相當大的佔有率。汽車製造商和車隊營運商擴大投資端到端區塊鏈平台,這些平台提供從智慧合約執行到供應鏈管理和資料認證的全套服務。這些解決方案可以降低營運成本,提高透明度,並幫助企業打造面向未來的數位基礎設施。

乘用車將獲得發展動力

由於數位技術在現代汽車中的快速融合,乘用車市場在2024年佔據了相當大的佔有率。隨著消費者對更智慧、更安全、更互聯的駕駛體驗的需求,汽車製造商正在利用區塊鏈來確保無線 (OTA) 更新的安全、車輛身分管理以及資料貨幣化模式。從叫車到訂閱模式,區塊鏈確保與汽車相關的每項交易和資料點都是安全且可追溯的。

區域洞察

北美將成為利潤豐厚的地區

2024年,北美汽車區塊鏈技術市場創造了可觀的收入,這得益於其強大的數位基礎設施、高額的研發支出以及強大的產業合作夥伴關係。美國主機廠和科技巨頭正引領這一趨勢,在數位車輛所有權、電動車電池追蹤和自動駕駛汽車資料驗證等領域開展試點計畫。該地區還受益於對區塊鏈創新的監管開放,這使得汽車公司能夠以更少的門檻擴展新的解決方案。

汽車區塊鏈技術市場的主要參與者包括 MOBI、亞馬遜、SAP SE、Tech Mahindra Limited、IBM Corporation、BigchainDB GmbH、微軟公司、甲骨文公司、R3、埃森哲公司。

汽車區塊鏈技術市場的領導者正在尋求策略合作、試點項目和產品創新,以鞏固其市場地位。各公司正在向汽車原始設備製造商提供區塊鏈即服務 (BaaS) 平台,以實現更快、更安全的部署。 R3 和 BigchainDB 等公司正專注於開發針對供應鏈、資料安全和智慧合約應用的可客製化區塊鏈協議。同時,由汽車製造商和科技公司組成的聯盟 MOBI 正在建立行業標準,以促進互通性。

目錄

第1章:方法論

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- GMI 專有 AI 系統

- 人工智慧驅動的研究增強

- 來源一致性協議

- 人工智慧準確度指標

- 預測模型

- 初步研究和驗證

- 市場估計的主要趨勢

- 量化市場影響分析

- 生長參數對預測的數學影響

- 情境分析框架

- 一些主要來源(但不限於)

- 資料探勘來源

- 次要

- 付費來源

- 公共資源

- 來源(按地區)

- 次要

- 研究路徑和信心評分

- 研究路徑組成部分:

- 評分組件

- 研究透明度附錄

- 來源歸因框架

- 品質保證指標

- 我們對信任的承諾

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 對供應鏈透明度和可追溯性的需求不斷增加

- 連網和自動駕駛汽車的普及率不斷上升

- 對防詐欺和安全交易的需求日益成長

- 移動即服務 (MaaS) 和共享汽車平台的擴展

- 產業陷阱與挑戰

- 區塊鏈系統實施與整合成本高

- 汽車網路缺乏標準化和互通性

- 市場機會

- 區塊鏈與物聯網和人工智慧的整合,實現預測性維護

- 車輛所有權轉移和數位身分解決方案的應用

- 透過智慧出行計畫拓展新興市場

- 中小企業和二/三級供應商整合

- 成長動力

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利分析

- 定價趨勢與經濟分析

- 用例

- 最佳情況

- 投資前景和資金分析

- 全球汽車科技投資趨勢

- 區塊鏈技術在汽車領域的投資

- 區域投資模式和政府支持

- 企業投資與併購活動

- 成本效益分析

- 實施成本結構和投資要求

- 營運效益和效率提升

- 財務效益和成本降低

- 策略利益和競爭優勢

- 車輛身分和生命週期管理

- 自動駕駛汽車和資料管理

- 感測器資料完整性和驗證

- 機器學習模型管理

- 責任和事故調查

- 數據貨幣化和共享

- 行動服務和支付整合

- 共乘和汽車共享平台

- 電動車充電與能源管理

- 智慧城市整合和基礎設施

- 保險與風險管理

- 網路安全與資料保護框架

- 汽車網路安全與區塊鏈整合

- 區塊鏈安全和威脅評估

- 資料隱私和合規性管理

- 事件回應和業務連續性

- 永續性和環境影響分析

- 碳足跡追蹤和報告

- 循環經濟和材料可追溯性

- 環境合規與報告

- 綠色科技與創新

- 未來技術路線圖與創新時間表

- 區塊鏈技術演進(2024-2034)

- 汽車技術整合時間表

- 產業轉型與融合場景

- 市場演變與中斷評估

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依類型,2021 - 2034

- 主要趨勢

- 公共區塊鏈

- 私有區塊鏈

- 混合區塊鏈

第6章:市場估計與預測:依組件,2021 - 2034

- 主要趨勢

- 解決方案

- 服務

第7章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 多功能乘用車

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

- 二輪車

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 供應鏈管理

- 車輛身分和生命週期管理

- 自動駕駛汽車資料管理

- 旅行服務和支付

- 其他

第9章:市場估計與預測:依組織規模,2021 - 2034 年

- 主要趨勢

- 中小企業

- 大型企業

第 10 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 原始設備製造商

- 車輛所有者

- 出行即服務提供者

- 其他

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

第12章:公司簡介

- 全球參與者

- Amazon

- BMW Group

- ConsenSys

- Ford Motor

- General Motors

- Hyperledger Foundation

- Hyundai Motor

- IBM

- Mercedes-Benz

- Microsoft

- Oracle

- R3

- Renault-Nissan-Mitsubishi Alliance

- SAP

- Toyota Motor

- Volkswagen

- 區域參與者

- MOBI

- VeChain

- OriginTrail

- Chronicled

- Ambrosus

- Provenance

- Everledger

- 新興玩家

- CarVertical

- AutoBlock

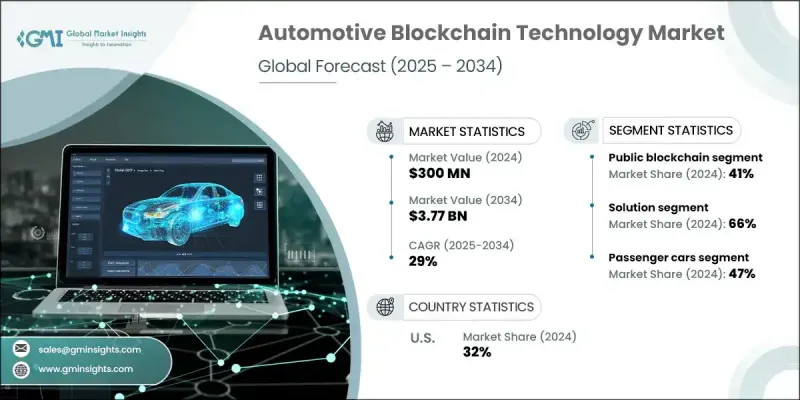

The Global Automotive Blockchain Technology Market was valued at USD 300 million in 2024 and is estimated to grow at a CAGR of 29% to reach USD 3.77 billion by 2034.

As vehicles become increasingly connected and software-driven, automakers are facing growing concerns around data integrity, cybersecurity, and real-time communication. Blockchain offers a decentralized, tamper-proof system to securely track and verify data across a vehicle's lifecycle from manufacturing and parts sourcing to software updates and ownership transfers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $300 Million |

| Forecast Value | $3.77 Billion |

| CAGR | 29% |

Increasing Prevalence of Public Blockchain

The public blockchain segment is expected to gain strong traction through 2034 driven by its unmatched transparency and decentralized structure. Public blockchains allow multiple stakeholders including automakers, regulators, suppliers, and end use to access and verify data in real-time, without relying on a central authority. This model is particularly useful for vehicle history tracking, ownership records, and shared mobility applications.

Rising Adoption of Solutions

The solutions segment from the automotive blockchain technology market held sizeable share in 2024. Automakers and fleet operators are increasingly investing in end-to-end blockchain platforms that offer a complete suite of services from smart contract execution to supply chain management and data authentication. These solutions reduce operational overhead, enhance transparency, and help companies to future-proof their digital infrastructure.

Passenger Cars to Gain Traction

The passenger cars segment held substantial share in 2024, owing to the rapid integration of digital technologies in modern vehicles. As consumers demand smarter, safer, and more connected driving experiences, automakers are leveraging blockchain to secure over-the-air (OTA) updates, manage vehicle identity, and enable data monetization models. From ride-hailing to subscription models, blockchain ensures that every transaction and data point tied to a car is secure and traceable.

Regional Insights

North America to Emerge as a Lucrative Region

North America automotive blockchain technology market generated significant revenues in 2024, driven by a robust digital infrastructure, high R&D spending, and strong industry partnerships. U.S. based OEMs and technology giants are leading the charge with pilot projects in digital vehicle titles, EV battery tracking, and autonomous vehicle data verification. The region also benefits from regulatory openness to blockchain innovation, allowing automotive companies to scale new solutions with fewer barriers.

Major players involved in the automotive blockchain technology market include MOBI, Amazon, SAP SE, Tech Mahindra Limited, IBM Corporation, BigchainDB GmbH, Microsoft Corporation, Oracle Corporation, R3, Accenture plc.

Leading players in the automotive blockchain technology market are pursuing strategic collaborations, pilot programs, and product innovation to strengthen their market position. Companies are offering blockchain-as-a-service (BaaS) platforms to automotive OEMs, enabling faster and more secure deployment. Firms such as R3 and BigchainDB are focusing on developing customizable blockchain protocols tailored for supply chain, data security, and smart contract applications. Meanwhile, MOBI, a consortium of automakers and tech firms, is building industry-wide standards to promote interoperability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 GMI proprietary AI system

- 1.1.5.1 AI-Powered research enhancement

- 1.1.5.2 Source consistency protocol

- 1.1.5.3 AI accuracy metrics

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Research Trail & Confidence Scoring

- 1.6.1 Research Trail Components:

- 1.6.2 Scoring Components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Organization Size

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for supply chain transparency and traceability

- 3.2.1.2 Rising adoption of connected and autonomous vehicles

- 3.2.1.3 Growing need for fraud prevention and secure transactions

- 3.2.1.4 Expansion of mobility-as-a-service (MaaS) and shared vehicle platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs for blockchain systems

- 3.2.2.2 Lack of standardization and interoperability across automotive networks

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of blockchain with IoT and AI for predictive maintenance

- 3.2.3.2 Adoption in vehicle ownership transfer and digital identity solutions

- 3.2.3.3 Expansion into emerging markets with smart mobility initiatives

- 3.2.3.4 SME and tier 2/3 supplier integration

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Pricing trends and economic analysis

- 3.9 Use cases

- 3.10 Best-case scenario

- 3.11 Investment landscape and funding analysis

- 3.11.1 Global automotive technology investment trends

- 3.11.2 Blockchain technology investment in automotive

- 3.11.3 Regional investment patterns and government support

- 3.11.4 Corporate investment and M&A activity

- 3.12 Cost-benefit analysis

- 3.12.1 Implementation cost structure and investment requirements

- 3.12.2 Operational benefits and efficiency gains

- 3.12.3 Financial benefits and cost reduction

- 3.12.4 Strategic benefits and competitive advantage

- 3.13 Vehicle identity and lifecycle management

- 3.14 Autonomous vehicle and data management

- 3.14.1 Sensor data integrity and validation

- 3.14.2 Machine learning model management

- 3.14.3 Liability and accident investigation

- 3.14.4 Data monetization and sharing

- 3.15 Mobility services and payment integration

- 3.15.1 Ride-sharing and car-sharing platforms

- 3.15.2 Electric vehicle charging and energy management

- 3.15.3 Smart city integration and infrastructure

- 3.15.4 Insurance and risk management

- 3.16 Cybersecurity and data protection framework

- 3.16.1 Automotive cybersecurity and blockchain integration

- 3.16.2 Blockchain security and threat assessment

- 3.16.3 Data privacy and compliance management

- 3.16.4 Incident response and business continuity

- 3.17 Sustainability and environmental impact analysis

- 3.17.1 Carbon footprint tracking and reporting

- 3.17.2 Circular economy and material traceability

- 3.17.3 Environmental compliance and reporting

- 3.17.4 Green technology and innovation

- 3.18 Future technology roadmap and innovation timeline

- 3.18.1 Blockchain technology evolution (2024-2034)

- 3.18.2 Automotive technology integration timeline

- 3.18.3 Industry transformation and convergence scenarios

- 3.18.4 Market evolution and disruption assessment

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.1.1 Public blockchain

- 5.1.2 Private blockchain

- 5.1.3 Hybrid blockchain

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Solution

- 6.3 Services

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUV

- 7.2.4 MPVs

- 7.3 Commercial Vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

- 7.4 Two-Wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Supply chain management

- 8.3 Vehicle identity and lifecycle management

- 8.4 Autonomous vehicle data management

- 8.5 Mobility services and payments

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 SME

- 9.3 Large enterprises

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 OEMs

- 10.3 Vehicle owners

- 10.4 Mobility as a service provider

- 10.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Nigeria

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Amazon

- 12.1.2 BMW Group

- 12.1.3 ConsenSys

- 12.1.4 Ford Motor

- 12.1.5 General Motors

- 12.1.6 Hyperledger Foundation

- 12.1.7 Hyundai Motor

- 12.1.8 IBM

- 12.1.9 Mercedes-Benz

- 12.1.10 Microsoft

- 12.1.11 Oracle

- 12.1.12 R3

- 12.1.13 Renault-Nissan-Mitsubishi Alliance

- 12.1.14 SAP

- 12.1.15 Toyota Motor

- 12.1.16 Volkswagen

- 12.2 Regional Players

- 12.2.1 MOBI

- 12.2.2 VeChain

- 12.2.3 OriginTrail

- 12.2.4 Chronicled

- 12.2.5 Ambrosus

- 12.2.6 Provenance

- 12.2.7 Everledger

- 12.3 Emerging Players

- 12.3.1 CarVertical

- 12.3.2 AutoBlock