|

市場調查報告書

商品編碼

1822539

安全數位卡市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Secure Digital Card Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

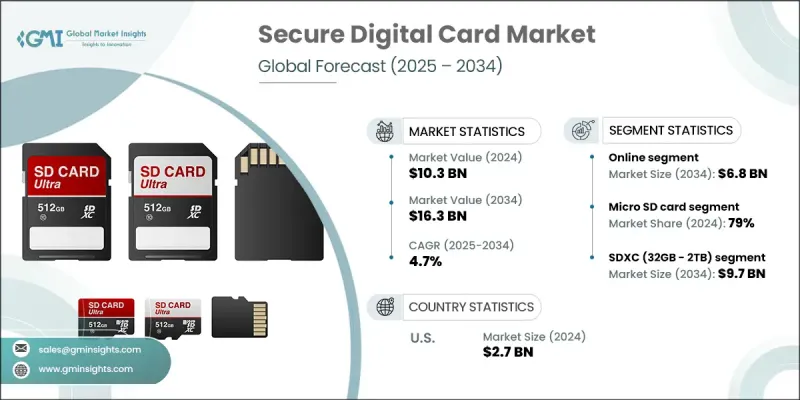

2024 年全球安全數位卡市場價值為 103 億美元,預計將以 4.7% 的複合年成長率成長,到 2034 年達到 163 億美元。

消費性電子產品對緊湊型大容量儲存的需求日益成長,以及物聯網和嵌入式系統的快速應用,推動了需求的激增。隨著邊緣運算的發展和人工智慧在設備層面的整合,SD 卡已成為實現本地資料儲存和緩衝的關鍵。這在自動駕駛、智慧基礎設施和監控等領域尤其重要。隨著邊緣人工智慧的興起,尤其是在北美和亞太地區,SD 卡的整合預計將進一步深化。能夠耐受極端環境的加固型 SD 卡在汽車、工業自動化和國防等領域正日益受到青睞。這些應用需要耐用、抗震的儲存設備,即使在嚴苛的操作條件下也能支援數位化工作流程。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 103億美元 |

| 預測值 | 163億美元 |

| 複合年成長率 | 4.7% |

2024年,micro SD卡市場佔有79%的市佔率。其主導地位主要歸功於無人機、智慧型手機和運動相機等小型設備的廣泛採用。隨著行動裝置功能越來越強大,以及創作高解析度內容的創作者數量不斷成長,UHS-I和UHS-II等microSD卡因其高耐用性和快速傳輸速度而越來越受到青睞。預計製造商將圍繞設備耐用性、資料傳輸速度以及與高階設備的兼容性加強產品行銷。

預計到2034年,線上分銷領域將創造68億美元的市場規模。消費者更青睞數位平台,因為它們便捷、產品多樣且易於比較。亞洲和北美的數位市場正透過精準行銷、搜尋引擎最佳化策略、限時搶購和個人化購物體驗加速線上SD卡的銷售。為了保持競爭力,品牌需要採用專注於直接面對消費者的精準廣告策略,並提升其在電商平台上的曝光度。

2024年,北美安全數位卡市場佔據31.1%的市場佔有率,預計到2034年將以4.7%的複合年成長率成長。該地區的成長得益於消費性電子產品使用量的不斷成長、視訊監控系統的日益普及以及影像領域內容創作者和專業人士日益成長的需求。為了搶佔市場佔有率,SD卡製造商專注於開發專為物聯網生態系統量身定做的高度安全的工業級儲存解決方案,並與區域原始設備製造商(OEM)和系統整合商保持合作。

全球安全數位卡市場的領導企業包括美光科技、雷克沙媒體、威剛科技、Nextorage、鎧俠、松下和金士頓科技。為了鞏固其在競爭激烈的安全數位卡行業中的地位,各公司正致力於透過適用於商業和工業用例的堅固耐用、高速和高容量的卡片來豐富其產品線。與智慧型手機品牌、相機製造商和原始設備製造商 (OEM) 建立策略聯盟有助於將 SD 卡相容性嵌入到下一代設備中。企業也利用人工智慧驅動的消費者行為分析來微調其行銷和分銷策略。透過投資在地化製造、擴展直接面對消費者的管道以及推廣環保產品設計,這些公司旨在增強全球影響力和客戶保留率。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 消費性電子產品對大容量儲存的需求不斷增加

- 數位影像設備和高畫質內容的普及率不斷提高

- 物聯網設備和嵌入式系統的擴展

- 監控和安全應用的成長

- 遊戲機和攜帶式設備日益普及

- 產業陷阱與挑戰

- 預算快閃記憶體的資料傳輸速度有限

- 大容量驅動器的熱管理挑戰

- 市場機會

- 資料中心和雲端運算的擴展

- 採用電動和自動駕駛汽車

- 企業從 HDD 過渡到 SSD

- 5G 部署提升行動與網路效能

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按類型,2021 - 2034

- 主要趨勢

- SD 卡

- 迷你 SD 卡

- Micro SD 卡

第6章:市場估計與預測:按產能,2021 - 2034 年

- 主要趨勢

- SDSC(最高 2GB)

- SDHC(2GB - 32GB)

- SDXC(32GB - 2TB)

第7章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 線上

- 離線

第 8 章:市場估計與預測:按最終用途應用,2021 - 2034 年

- 主要趨勢

- 消費性電子產品

- 智慧型手機和平板電腦

- 筆記型電腦和桌上型電腦

- 數位相機

- 穿戴式裝置

- 其他

- 汽車

- 資訊娛樂系統

- 行車記錄器和 ADAS資料存儲

- 其他

- 工業的

- 工業物聯網系統

- 工廠自動化與機器人技術

- 其他

- 衛生保健

- 零售

- 軍事與國防

- 其他

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球關鍵參與者

- SanDisk

- Samsung Electronics

- Sony

- Micron Technology

- 區域關鍵參與者

- 北美洲

- Lexar Media

- Patriot Memory

- PNY Technologies

- 歐洲

- Verbatim

- Kingston Technology

- Nextorage

- 亞太地區

- Kioxia

- Toshiba

- Transcend Information

- Panasonic

- 北美洲

- 利基市場參與者/顛覆者

- Adata Technology

The Global Secure Digital Card Market was valued at USD 10.3 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 16.3 billion by 2034.

The surge in demand is driven by the rising need for compact, high-capacity storage across consumer electronics and the rapidly growing use of IoT and embedded systems. With the evolution of edge computing and the integration of AI at the device level, SD cards have become critical for enabling local data storage and buffering. This is particularly important in sectors like autonomous mobility, smart infrastructure, and surveillance. As edge AI gains traction, especially across North America and the Asia-Pacific region, SD card integration is expected to deepen. Ruggedized SD cards that endure extreme environments are gaining significant traction in sectors like automotive, industrial automation, and defense. These applications demand durable, shock-resistant storage that supports digital workflows even under challenging operational conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.3 Billion |

| Forecast Value | $16.3 Billion |

| CAGR | 4.7% |

In 2024, the micro SD card segment held a 79% share. Its dominance is largely due to high adoption in compact devices such as drones, smartphones, and action cameras. As mobile devices become more powerful and the number of creators producing high-resolution content grows, microSD variants like UHS-I and UHS-II are increasingly preferred for their high durability and fast transfer speeds. Manufacturers are expected to strengthen product marketing around device endurance, data speed, and compatibility with advanced devices.

The online distribution segment is projected to generate USD 6.8 billion by 2034. Consumers prefer digital platforms for their convenience, product variety, and ease of comparison. Digital marketplaces in Asia and North America are accelerating online SD card sales through targeted marketing, SEO strategies, flash deals, and personalized shopping experiences. To stay competitive, brands need to adopt precision advertising techniques focused on direct-to-consumer outreach and enhance their visibility across e-commerce platforms.

North America Secure Digital Card Market held 31.1% share in 2024 and is forecasted to grow at a CAGR of 4.7% through 2034. Growth in this region is supported by expanding consumer electronics usage, rising adoption of video surveillance systems, and increased demand from content creators and professionals in the imaging space. To capture market share, SD card makers focus on developing highly secure, industrial-grade storage solutions tailored for IoT ecosystems and align with regional OEMs and system integrators.

Leading players in the Global Secure Digital Card Market include Micron Technology, Lexar Media, Adata Technology, Nextorage, Kioxia, Panasonic, and Kingston Technology. To solidify their position in the competitive secure digital card industry, companies are focusing on diversifying their product lines with rugged, high-speed, and high-capacity cards suitable for both commercial and industrial use cases. Strategic alliances with smartphone brands, camera manufacturers, and OEMs help in embedding SD card compatibility into next-gen devices. Firms are also leveraging AI-driven consumer behavior analytics to fine-tune their marketing and distribution strategies. By investing in localized manufacturing, expanding direct-to-consumer channels, and promoting eco-friendly product designs, these companies aim to enhance both global reach and customer retention.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Capacity trends

- 2.2.3 Distribution channel trends

- 2.2.4 End use application trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for high-capacity storage in consumer electronics

- 3.2.1.2 Growing adoption of digital imaging devices and HD content

- 3.2.1.3 Expansion of IoT devices and embedded systems

- 3.2.1.4 Growth in surveillance and security applications

- 3.2.1.5 Rising popularity of gaming consoles and portable devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited data transfer speeds in budget flash storage

- 3.2.2.2 Thermal management challenges in high-capacity drives

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of data centers and cloud computing

- 3.2.3.2 Adoption of electric and autonomous vehicles

- 3.2.3.3 Transition from HDD to SSD in enterprises

- 3.2.3.4 5G rollouts enhancing mobile and network performance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion & Thousand Units)

- 5.1 Key trends

- 5.2 SD card

- 5.3 Mini SD card

- 5.4 Micro SD card

Chapter 6 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Billion & Thousand Units)

- 6.1 Key trends

- 6.2 SDSC (Up to 2GB)

- 6.3 SDHC (2GB - 32GB)

- 6.4 SDXC (32GB - 2TB)

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion & Thousand Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Billion & Thousand Units)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.2.1 Smartphone & tablets

- 8.2.2 Laptops & computers

- 8.2.3 Digital cameras

- 8.2.4 Wearable devices

- 8.2.5 Others

- 8.3 Automotive

- 8.3.1 Infotainment system

- 8.3.2 Dashcams and ADAS data storage

- 8.3.3 Others

- 8.4 Industrial

- 8.4.1 Industrial IoT systems

- 8.4.2 Factory automation and robotics

- 8.4.3 Others

- 8.5 Healthcare

- 8.6 Retail

- 8.7 Military & Defense

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 SanDisk

- 10.1.2 Samsung Electronics

- 10.1.3 Sony

- 10.1.4 Micron Technology

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Lexar Media

- 10.2.1.2 Patriot Memory

- 10.2.1.3 PNY Technologies

- 10.2.2 Europe

- 10.2.2.1 Verbatim

- 10.2.2.2 Kingston Technology

- 10.2.2.3 Nextorage

- 10.2.3 APAC

- 10.2.3.1 Kioxia

- 10.2.3.2 Toshiba

- 10.2.3.3 Transcend Information

- 10.2.3.4 Panasonic

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Adata Technology

SD卡市場分析及至2035年預測:類型、技術、應用、最終用戶、產品容量

SD卡市場分析及至2035年預測:類型、技術、應用、最終用戶、產品容量 快閃記憶體卡市場規模、佔有率、趨勢和預測:按產品類型、分銷管道、應用和地區分類,2026-2034年

快閃記憶體卡市場規模、佔有率、趨勢和預測:按產品類型、分銷管道、應用和地區分類,2026-2034年 CF記憶卡複製機市場報告:趨勢、預測與競爭分析(至2035年)

CF記憶卡複製機市場報告:趨勢、預測與競爭分析(至2035年) 安全數位記憶卡市場:按容量、類型、應用、速度等級和分銷管道分類 - 全球預測 2026-2032記憶卡市場:按外形規格、容量範圍、技術類型、速度等級、應用和分銷管道分類-2026-2032年全球預測

安全數位記憶卡市場:按容量、類型、應用、速度等級和分銷管道分類 - 全球預測 2026-2032記憶卡市場:按外形規格、容量範圍、技術類型、速度等級、應用和分銷管道分類-2026-2032年全球預測 安全數位(SD)卡市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026–2034)

安全數位(SD)卡市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026–2034) 2025年全球安全數位卡市場報告

2025年全球安全數位卡市場報告 安全數位卡市場規模、佔有率、按規模、儲存容量、應用和地區分類的成長分析 - 產業預測,2025 年至 2032 年

安全數位卡市場規模、佔有率、按規模、儲存容量、應用和地區分類的成長分析 - 產業預測,2025 年至 2032 年 全球安全數位卡市場全球 SD 記憶卡市場:市場規模(按卡類型、應用程式、儲存容量和地區)、未來預測

全球安全數位卡市場全球 SD 記憶卡市場:市場規模(按卡類型、應用程式、儲存容量和地區)、未來預測