|

市場調查報告書

商品編碼

1801935

脊椎融合設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Spinal Fusion Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

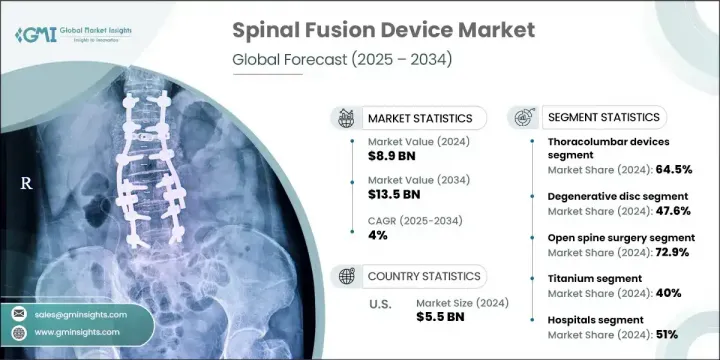

2024年,全球脊椎融合器材市場規模達89億美元,預計2034年將以4%的複合年成長率成長,達到135億美元。市場成長動能的驅動力源自於脊椎疾病發生率的上升、目標患者群體的擴大,以及持續的研發投入,旨在開發更先進、更微創的融合手術。儘管前景樂觀,但一些新興國家報銷選擇有限,仍是市場全面擴張的挑戰。然而,脊椎外科手術的進步和全球老化人口的增加持續推高了需求。技術進步,尤其是術中影像、機器人技術和導航技術,正在幫助減少手術併發症並改善療效。

2024年,胸腰椎器械市場佔據64.5%的市場佔有率,這歸因於腰椎退化性疾病和脊椎損傷的發生率較高,這些疾病需要對胸椎和腰椎進行手術固定。該領域的成長主要源自於老年人高衝擊力創傷和脊椎退化發生率的上升。此外,諸如脊椎骨折和脊椎滑脫等疾病正在透過精密設計的器械進行治療,以改善穩定性和恢復能力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 89億美元 |

| 預測值 | 135億美元 |

| 複合年成長率 | 4% |

2024年,退化性椎間盤疾病領域佔據47.6%的市場。這一主導地位歸因於與年齡相關的椎間盤退化病例的激增,以及微創脊椎融合術的廣泛應用。隨著越來越多的老年人出現椎間盤相關問題,對高效率、低風險治療的需求持續成長。早期發現、患者認知度的提高以及對微創手術日益成長的信任,也對提升該領域的表現發揮著至關重要的作用。

2024年,美國脊椎融合器材市場規模達55億美元。這一成長源於老年患者數量的增加、脊椎疾病負擔的加重,以及創新手術器械和技術的日益普及。該地區擁有強大的醫療保健體系、先進的外科基礎設施,以及對現代脊椎植入物和導航系統的廣泛採用。 2021年,該市場規模達42億美元,2022年達47億美元,在臨床需求和技術進步的推動下,市場規模逐年穩定成長。

全球脊椎融合器材市場的頂級公司包括史賽克 (Stryker)、Globus Medical、美敦力 (Medtronic)、NuVasive 和 DePuy Synthes。為了鞏固市場地位,領先的脊椎融合器材製造商正在大力投資機器人輔助手術、人工智慧導航系統和微創產品開發。這些公司正在透過研發和有針對性的收購來擴展其產品組合,以提供端到端的脊椎解決方案。與醫院和外科中心的策略合作夥伴關係也使先進器械的採用速度更快。一些公司正在本地化生產並加強分銷網路,以更好地服務高成長市場。持續的外科醫生培訓計劃和數位平台整合正在進一步提高手術的精確度和跨地區的採用率。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 脊椎疾病盛行率不斷上升

- 技術進步

- 創傷和損傷病例數上升

- 老年人口不斷增加,對微創手術的需求也不斷增加

- 產業陷阱與挑戰

- 嚴格的監管情景

- 脊椎手術費用高昂

- 市場機會

- 門診手術中心(ASC)的成長

- 機器人和導航輔助手術的採用率不斷提高

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 導航與機器人系統的整合

- PEEK 和鈦合金籠的廣泛使用

- 新興技術

- 3D列印和脊椎植入物的進步

- 整合感測器的智慧植入物

- 當前的技術趨勢

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

- 價值鏈分析

- 報銷場景

- 消費者行為分析

- 比較分析:前路與後路手術入路

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 胸腰椎裝置

- 椎弓根螺釘

- 椎間融合裝置(IBFD)

- 桿

- 盤子

- 其他胸腰椎裝置

- 頸椎固定裝置

- 椎間融合裝置(IBFD)

- 盤子

- 桿

- 鉤子

- 其他子宮頸裝置

第6章:市場估計與預測:依疾病類型,2021 - 2034 年

- 主要趨勢

- 椎間盤退化

- 脊椎畸形

- 創傷與骨折

- 脊椎腫瘤

- 其他疾病類型

第7章:市場估計與預測:按手術,2021 - 2034 年

- 主要趨勢

- 開放性脊椎手術

- 微創脊椎手術

第8章:市場估計與預測:按材料類型,2021 - 2034 年

- 主要趨勢

- 鈦

- 聚醚醚酮(PEEK)

- 鈷鉻合金

- 不銹鋼

- 其他材料

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 骨科診所

- 其他最終用途

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- ATEC

- B. Braun

- Captiva Spine

- ChoiceSpine

- DePuy Synthes

- Globus Medical

- K2M

- Life Spine

- Medtronic

- NuVasive

- Orthofix

- Premia Spine

- Stryker

- Xtant Medical

- Zimmer Biomet

The Global Spinal Fusion Device Market was valued at USD 8.9 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 13.5 billion by 2034. The market's upward momentum is fueled by the rising number of spinal disorders, a growing pool of target patients, and ongoing investments in R&D to develop more advanced and minimally invasive fusion procedures. Despite the positive outlook, limited reimbursement options in several emerging countries remain a challenge for full market scalability. Nevertheless, advancements in spinal surgery and the rise in aging populations worldwide continue to elevate demand. Technological evolution, particularly in intraoperative imaging, robotics, and navigation, is helping reduce surgical complications and improve outcomes.

The thoracolumbar devices segment held 64.5% share in 2024, owing to the high frequency of lumbar degenerative disorders and spinal injuries that necessitate surgical stabilization in both the thoracic and lumbar spine. Growth in this segment is largely driven by increasing rates of high-impact trauma and spine degeneration among older adults. Additionally, conditions like spinal fractures and spondylolisthesis are being addressed with precision-engineered devices to improve stability and recovery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $13.5 Billion |

| CAGR | 4% |

In 2024, the degenerative disc disorder segment held a 47.6% share. This dominance is attributed to a surge in cases of age-related disc degeneration and the broader adoption of less invasive spinal fusion methods. As more elderly individuals experience disc-related issues, the need for efficient, lower-risk treatment continues to climb. Earlier detection, patient awareness, and growing trust in minimally invasive procedures also play vital roles in boosting the segment's performance.

US Spinal Fusion Device Market generated USD 5.5 billion in 2024. This growth stems from an increasing number of geriatric patients and a high burden of spinal disorders, along with broader acceptance of innovative surgical tools and techniques. The region benefits from a robust healthcare system, advanced surgical infrastructure, and favorable adoption of modern spinal implants and navigation systems. The market was valued at USD 4.2 billion in 2021 and USD 4.7 billion in 2022, showing steady annual increases fueled by clinical demand and technological improvements.

Top companies in the Global Spinal Fusion Device Market include Stryker, Globus Medical, Medtronic, NuVasive, and DePuy Synthes. To strengthen their market presence, leading spinal fusion device manufacturers are investing heavily in robotic-assisted surgery, AI-powered navigation systems, and minimally invasive product development. These firms are expanding their product portfolios through R&D and targeted acquisitions to offer end-to-end spinal solutions. Strategic partnerships with hospitals and surgical centers are also enabling quicker adoption of advanced devices. Several companies are localizing production and strengthening distribution networks to better serve high-growth markets. Continuous surgeon training programs and digital platform integration are further enhancing procedural precision and adoption rates across geographies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Disease type trends

- 2.2.3 Surgery trends

- 2.2.4 Material type trends

- 2.2.5 End use trends

- 2.2.6 Region trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of spinal diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rise in number of trauma and injury cases

- 3.2.1.4 Rising geriatric population coupled with high demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of spinal procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of ambulatory surgical centers (ASCs)

- 3.2.3.2 Increasing adoption of robotic and navigation-assisted surgery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Integration of navigation and robotic systems

- 3.5.1.2 Widespread use of PEEK and titanium cages

- 3.5.2 Emerging technologies

- 3.5.2.1 3D Printing, and advances in spinal implants

- 3.5.2.2 Smart implants with sensor integration

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.7 Spinal Fusion Device Market, By Region, 2021 - 2034 (Units)

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Value chain analysis

- 3.12 Reimbursement scenario

- 3.13 Consumer behaviour analysis

- 3.14 Comparative analysis: anterior Vs posterior surgical approach

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Thoracolumbar devices

- 5.2.1 Pedicle screws

- 5.2.2 Intervertebral body fusion device (IBFD)

- 5.2.3 Rods

- 5.2.4 Plates

- 5.2.5 Other thoracolumbar devices

- 5.3 Cervical fixation devices

- 5.3.1 Intervertebral body fusion device (IBFD)

- 5.3.2 Plates

- 5.3.3 Rods

- 5.3.4 Hooks

- 5.3.5 Other cervical devices

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Degenerative disc

- 6.3 Spinal deformity

- 6.4 Trauma and fractures

- 6.5 Spinal tumors

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Surgery, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open spine surgery

- 7.3 Minimally invasive spine surgery

Chapter 8 Market Estimates and Forecast, By Material Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Titanium

- 8.3 Polyether ether ketone (PEEK)

- 8.4 Cobalt chrome

- 8.5 Stainless steel

- 8.6 Other materials

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Orthopedic clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ATEC

- 11.2 B. Braun

- 11.3 Captiva Spine

- 11.4 ChoiceSpine

- 11.5 DePuy Synthes

- 11.6 Globus Medical

- 11.7 K2M

- 11.8 Life Spine

- 11.9 Medtronic

- 11.10 NuVasive

- 11.11 Orthofix

- 11.12 Premia Spine

- 11.13 Stryker

- 11.14 Xtant Medical

- 11.15 Zimmer Biomet

脊椎固定裝置市場:2026-2032年全球市場預測(按產品類型、類別、植入材料、手術方法、應用和最終用戶分類)

脊椎固定裝置市場:2026-2032年全球市場預測(按產品類型、類別、植入材料、手術方法、應用和最終用戶分類) 姿勢矯正矯正器具市場規模、佔有率和成長分析:按產品類型、材料成分、目標用戶、分銷管道和地區分類-2026-2033年產業預測後路頸椎融合植入產品市場(依手術入路、最終用戶、產品類型、材料、手術等級、適應症、植入類型和分銷管道分類),全球預測,2026-2032年

姿勢矯正矯正器具市場規模、佔有率和成長分析:按產品類型、材料成分、目標用戶、分銷管道和地區分類-2026-2033年產業預測後路頸椎融合植入產品市場(依手術入路、最終用戶、產品類型、材料、手術等級、適應症、植入類型和分銷管道分類),全球預測,2026-2032年 2026年全球脊椎固定器市場報告

2026年全球脊椎固定器市場報告 脊椎融合裝置市場:依裝置類型、手術類型、最終用戶和地區分類

脊椎融合裝置市場:依裝置類型、手術類型、最終用戶和地區分類 全球脊椎融合手術器材市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球脊椎融合手術器材市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 頸椎病診斷及治療市場-全球產業規模、佔有率、趨勢、機會及預測(按診斷、產品類型、通路、地區和競爭格局分類,2021-2031年)

頸椎病診斷及治療市場-全球產業規模、佔有率、趨勢、機會及預測(按診斷、產品類型、通路、地區和競爭格局分類,2021-2031年) 全球脊椎固定器市場:洞察、競爭格局及至2032年預測2025年全球頸椎病治療市場報告

全球脊椎固定器市場:洞察、競爭格局及至2032年預測2025年全球頸椎病治療市場報告 脊椎融合裝置市場,按產品類型、按手術類型、按疾病適應症、按材料、按最終用戶、按國家/地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測

脊椎融合裝置市場,按產品類型、按手術類型、按疾病適應症、按材料、按最終用戶、按國家/地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測