|

市場調查報告書

商品編碼

1801921

麻混凝土市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Hempcrete Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024年,全球麻混凝土市場規模達5.702億美元,預計到2034年將以14.9%的複合年成長率成長,達到22.4億美元。隨著人們對環境影響的認知不斷增強,開發商和建築商擴大轉向低排放、永續的建築替代方案。麻混凝土具有可生物分解和碳封存的特性,與全球減少建築環境碳足跡的目標高度契合。其天然特性使其成為節能建築和環保住宅設計的理想材料,有助於滿足監管要求和消費者對更環保解決方案的期望。

政府推出的降低排放和提高能源效率的法規進一步激發了人們對麻混凝土等天然材料的興趣。一些國家正在實施更嚴格的溫室氣體排放法規,這促使人們轉向使用熱效率高且天然的隔熱材料。此外,LEED 和 BREEAM 等永續發展框架正在促使建築公司優先考慮環保材料,從而確保住宅、商業和工業領域對麻混凝土的長期穩定需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.702億美元 |

| 預測值 | 22.4億美元 |

| 複合年成長率 | 14.9% |

石灰基黏合劑市場在2024年創造了3.837億美元的收入,預計2025年至2034年的複合年成長率將達到14.5%。這些黏合劑與麻稈完美契合,具有高透氣性和強大的碳吸收能力。石灰黏合劑秉承了麻稈混凝土的環保形象,常用於經認證的綠色住宅。儘管石灰黏合劑固化時間較長且結構強度較低,但持續的研發已催生出更多以性能為導向的替代方案,同時保持了永續性。

2024年,住宅建築業創造了3.381億美元的收入,佔59.2%的市場。預計到2034年,該產業的複合年成長率將達到14.4%,受益於人們對節能自建住宅、低排放建築和氣候意識建築趨勢日益成長的興趣。麻石的隔熱、低毒和二氧化碳吸收特性使其成為永續住宅的理想材料,尤其是在北美和歐洲部分地區等注重環保的市場。

2024年,美國麻混凝土市場規模達1.691億美元,預計2034年將以14.1%的複合年成長率成長。不斷完善的麻混凝土種植法規、綠色建築產品需求以及永續建築實踐的日益普及,共同推動了美國國內市場的成長。麻混凝土在環境進步的州,尤其在房屋翻新和新建方面備受青睞。加拿大對工業麻混凝土產業的支持也促進了模組化和住宅應用領域強勁的跨境合作和供應鏈。

塑造全球麻混凝土市場的關鍵參與者包括 Hempitecture Inc.、Cavac Biomateriaux、Hemp and Block、American Hemp LLC 和 HempStone。為了擴大市場佔有率,麻混凝土行業的公司正在投資研發,以提升黏合劑性能、加快固化時間並提高結構強度。與永續建築公司和建築師的策略合作有助於提高專案的知名度。許多公司正在擴大生產能力並建立在地化供應鏈,以降低物流成本並提高產品的可及性。此外,圍繞綠色建築標準的教育活動和認證也被用來將麻混凝土定位為傳統材料的可行主流替代品。這些努力共同提升了品牌在全球市場的信譽、合規性和消費者信任度。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測,活頁夾類型,2021-2034

- 主要趨勢

- 石灰基黏合劑

- 水硬石灰

- 地上石灰

- 改質石灰配方

- 水泥基黏合劑

- 波特蘭水泥

- 混合水泥體系

- 低碳水泥替代品

- 替代黏合劑

- 鹼激活黏合劑

- 空心微珠黏合劑

- 土聚物黏合劑

- 基於菌絲體的黏合劑

- 混合配方

- 石灰水泥混合物

- 聚合物改質體系

- 纖維增強配方

第6章:市場估計與預測:依施工方法,2021-2034 年

- 主要趨勢

- 現澆系統

- 手工鑄造方法

- 氣動放置

- 模板系統

- 預製系統

- 砌塊製造

- 面板生產

- 模組化組件

- 噴塗應用

- 濕噴系統

- 乾混應用

- 機器人噴塗系統

- 先進製造業

- 3D列印技術

- 自動化生產系統

- 數位化製造方法

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 牆壁和結構填充物

- 住宅應用

- 商業應用

- 工業應用

- 絕緣系統

- 隔熱市場

- 隔音應用

- 改造絕緣解決方案

- 屋頂和地板

- 屋頂應用

- 地板系統

- 專業應用

- 預製塊和麵板

- 預製砌塊市場

- 面板系統

- 模組化建築應用

- 現澆應用

- 現場鑄造

- 噴塗應用

- 定製配方

- 新興應用

- 3D列印應用

- 複合材料

- 專業建築用途

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 住宅建築

- 獨棟住宅

- 多戶住宅

- 經濟適用房項目

- 改造和翻新

- 商業建築

- 辦公大樓

- 零售空間

- 教育設施

- 醫療保健設施

- 工業建築

- 生產設施

- 倉庫和配送中心

- 農業建築

- 特殊工業應用

- 基礎設施項目

- 公共建築

- 社區中心

- 交通基礎設施

- 公用建築

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- American Hemp LLC

- Cavac Biomateriaux

- Hemp and Block

- Hemp Building Institute

- Hemp Technology Ltd.

- Hempitecture Inc.

- HempStone

- IsoHemp

- Lower Sioux Indian Community

- Rare Earth Global

- rePlant Hemp Advisors

- Sativa Building Systems

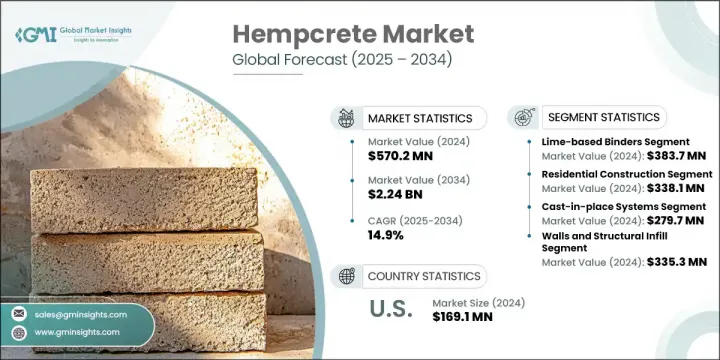

The Global Hempcrete Market was valued at USD 570.2 million in 2024 and is estimated to grow at a CAGR of 14.9% to reach USD 2.24 billion by 2034. As awareness of environmental impact grows, developers and builders are increasingly turning toward low-emission, sustainable construction alternatives. Hempcrete, being biodegradable and capable of sequestering carbon, aligns closely with global goals to reduce the carbon footprint in the built environment. Its natural properties make it an ideal material in energy-efficient buildings and eco-conscious residential design, helping meet both regulatory demands and consumer expectations for greener solutions.

Government mandates pushing for lower emissions and enhanced energy efficiency are further driving interest in natural materials like hempcrete. Several countries are enforcing stricter codes to reduce greenhouse gas emissions, which has prompted a shift toward using thermally efficient and natural insulation options. In addition, sustainability frameworks such as LEED and BREEAM are influencing construction companies to prioritize eco-friendly materials, ensuring steady demand for hempcrete across residential, commercial, and even industrial sectors in the long term.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $570.2 Million |

| Forecast Value | $2.24 Billion |

| CAGR | 14.9% |

Lime-based binders segment generated USD 383.7 million in 2024 and is expected to grow at a CAGR of 14.5% from 2025 to 2034. These binders are well-aligned with hemp hurd, offering high breathability and strong carbon absorption. Lime binders uphold the environmentally friendly image of hempcrete and are commonly used in certified green housing. Though they take longer to cure and offer lower structural strength, continuous R&D has given rise to more performance-driven alternatives while keeping sustainability intact.

The residential construction segment generated USD 338.1 million in 2024 and capturing 59.2% share. With a CAGR of 14.4% anticipated through 2034, the sector benefits from rising interest in energy-efficient self-build homes, low-emission structures, and climate-conscious architectural trends. Hempcrete's thermal insulation, low toxicity, and CO2 absorbing qualities make it a favorable material for sustainable housing, particularly in environmentally progressive markets such as North America and parts of Europe.

U.S. Hempcrete Market was valued at USD 169.1 million in 2024 and is forecasted to grow at a CAGR of 14.1% through 2034. Domestic growth is supported by evolving regulations around hemp cultivation, demand for green building products, and increasing adoption of sustainable construction practices. Hempcrete has gained traction particularly in retrofitting and new housing across environmentally progressive states. Canada's support for the industrial hemp industry also contributes to robust cross-border collaborations and supply chains for modular and residential applications.

Key players shaping the Global Hempcrete Market include Hempitecture Inc., Cavac Biomateriaux, Hemp and Block, American Hemp LLC, and HempStone. To expand their market share, companies operating in the hempcrete industry are investing in research and development to enhance binder performance, speed up curing time, and improve structural strength. Strategic collaborations with sustainable construction firms and architects are helping to increase project visibility. Many are scaling their production capabilities and establishing localized supply chains to reduce logistics costs and improve product accessibility. Educational campaigns and certifications around green building standards are also used to position hempcrete as a viable mainstream alternative to traditional materials. These efforts collectively enhance brand credibility, regulatory compliance, and consumer trust across global markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Binder Type

- 2.2.3 Construction Method

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2021-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Binder Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Lime-based binders

- 5.2.1 Hydraulic lime

- 5.2.2 Aerial lime

- 5.2.3 Modified lime formulations

- 5.3 Cement-based binders

- 5.3.1 Portland cement

- 5.3.2 Blended cement systems

- 5.3.3 Low-carbon cement alternatives

- 5.4 Alternative binders

- 5.4.1 Alkali-activated binders

- 5.4.2 Cenosphere binders

- 5.4.3 Geopolymer binders

- 5.4.4 Mycelium-based binders

- 5.5 Hybrid formulations

- 5.5.1 Lime-cement blends

- 5.5.2 Polymer-modified systems

- 5.5.3 Fiber-reinforced formulations

Chapter 6 Market Estimates & Forecast, By Construction Method, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cast-in-place systems

- 6.2.1 Hand-casting methods

- 6.2.2 Pneumatic placement

- 6.2.3 Formwork systems

- 6.3 Precast systems

- 6.3.1 Block manufacturing

- 6.3.2 Panel production

- 6.3.3 Modular components

- 6.4 Spray applications

- 6.4.1 Wet spray systems

- 6.4.2 Dry mix applications

- 6.4.3 Robotic spray systems

- 6.5 Advanced manufacturing

- 6.5.1 3d printing technology

- 6.5.2 Automated production systems

- 6.6 Digital fabrication methods

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Walls and structural infill

- 7.2.1 Residential applications

- 7.2.2 Commercial applications

- 7.2.3 Industrial applications

- 7.3 Insulation systems

- 7.3.1 Thermal insulation market

- 7.3.2 Acoustic insulation applications

- 7.3.3 Retrofit insulation solutions

- 7.4 Roofing and flooring

- 7.4.1 Roofing applications

- 7.4.2 Flooring systems

- 7.4.3 Specialty applications

- 7.5 Precast blocks and panels

- 7.5.1 Precast block market

- 7.5.2 Panel systems

- 7.5.3 Modular construction applications

- 7.6 Cast-in-place applications

- 7.6.1 On-site casting

- 7.6.2 Spray applications

- 7.6.3 Custom formulations

- 7.7 Emerging applications

- 7.7.1 3d printing applications

- 7.7.2 Composite materials

- 7.7.3 Specialty construction uses

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.2.1 Single-family homes

- 8.2.2 Multi-family housing

- 8.2.3 Affordable housing projects

- 8.2.4 Retrofit and renovation

- 8.3 Commercial construction

- 8.3.1 Office buildings

- 8.3.2 Retail spaces

- 8.3.3 Educational facilities

- 8.3.4 Healthcare facilities

- 8.4 Industrial construction

- 8.4.1 Manufacturing facilities

- 8.4.2 Warehouses and distribution centers

- 8.4.3 Agricultural buildings

- 8.4.4 Specialty industrial applications

- 8.5 Infrastructure projects

- 8.5.1 Public buildings

- 8.5.2 Community centers

- 8.5.3 Transportation infrastructure

- 8.5.4 Utility buildings

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 American Hemp LLC

- 10.2 Cavac Biomateriaux

- 10.3 Hemp and Block

- 10.4 Hemp Building Institute

- 10.5 Hemp Technology Ltd.

- 10.6 Hempitecture Inc.

- 10.7 HempStone

- 10.8 IsoHemp

- 10.9 Lower Sioux Indian Community

- 10.10 Rare Earth Global

- 10.11 rePlant Hemp Advisors

- 10.12 Sativa Building Systems

2026年全球麻石混凝土市場報告

2026年全球麻石混凝土市場報告 麻石混凝土市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

麻石混凝土市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 2026-2030年全球大麻包裝箱市場

2026-2030年全球大麻包裝箱市場 麻混凝土市場按產品類型、形式、最終用戶、應用、建築類型、最終用戶和分銷管道分類 - 2025-2030 年全球預測

麻混凝土市場按產品類型、形式、最終用戶、應用、建築類型、最終用戶和分銷管道分類 - 2025-2030 年全球預測 全球麻混凝土市場

全球麻混凝土市場 2032 年麻混凝土市場預測:按產品類型、施工方法、分銷管道、應用、最終用戶和地區進行的全球分析

2032 年麻混凝土市場預測:按產品類型、施工方法、分銷管道、應用、最終用戶和地區進行的全球分析 麻混凝土市場報告:2031 年趨勢、預測與競爭分析

麻混凝土市場報告:2031 年趨勢、預測與競爭分析 麻混凝土市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、配銷通路、應用、地區和競爭細分,2020-2030 年

麻混凝土市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、配銷通路、應用、地區和競爭細分,2020-2030 年 麻混凝土的全球市場 - 永續的建設,預測(2025年~2033年)麻凝土的全球市場:趨勢,知識和見識,成長預測(2025年~2033年)

麻混凝土的全球市場 - 永續的建設,預測(2025年~2033年)麻凝土的全球市場:趨勢,知識和見識,成長預測(2025年~2033年)